All about Taxation of Income From Capital Gains

Table of Contents

Overview on Taxation of Income From Capital Gains

Meaning of Capital Gain

- Any profits or gains arising from the transfer of a Capital Asset effected in the previous year. Such profit will be chargeable to tax u/h of Capital Gain.

- Capital gains apply to any type of asset, including investments.

- The gain may be short-term or long-term and must be claimed on income taxes.

- Income tax sections under which treatment of income from capital gains is covered are section 45 to 55A.

Chargeability of Capital Gains u/s 45(1)

- Any profits or gains arising from the transfer of a capital asset effected in the previous year shall, be chargeable to income-tax under the head “Capital gains”, and shall be deemed to be the income of the previous year in which the transfer took place

- For e.g : If Mr A transfers a capital asset on 27th March 2022, however the payment of the same is received on 5th April 2022, then in this case capital gains shall be taxable in the previous year 2021-22.

Meaning of Capital Asset u/s 2(14)

Capital Asset is defined to include:

- Any kind of property held by an assesse, whether or not connected with business or profession of the assesse.

- Securities held by a FII which has invested in such securities in accordance with the regulations made under the SEBI Act, 1992.

But following are excluded from the definition of “Capital Assets”:

- Stock -in- trade, consumable stores, raw materials held for the purpose of business or profession;

- Movable property held for personal use of taxpayer or for any member of his family dependent upon him. However, jewellery, costly stones, and ornaments made of silver, gold, platinum or any other precious metal, archaeological collections, drawings, paintings, sculptures or any work of art shall be considered as capital asset even if used for personal purposes;

- Specified Gold Bonds and Special Bearer Bonds;

- Agricultural Land in India, not being a land situated:

- Within jurisdiction of municipality, notified area committee, town area committee cantonment board and which has a population not less than 10,000;

- Deposit certificates issued under the Gold Monetization Scheme, 2015

- Within range of following distance measured aerially from the local limits of any municipality or cantonment board:

- Not being more than 2 KMs, if population of such area is more than 10,000 but not exceeding 1 lakh;

-

- It should Not being more than 6 KMs, if population of such area is more than 1 lakh but not exceeding 10 lakhs; or

-

- Not being more than 8 KMs , if population of such area is more than 10 lakhs

- Unit Linked Insurance Plan to which exemption u/s 10(10D) does not apply due to fourth and fifth proviso thereof.

Capital Asset

Short term capital assets u/s 2(42A)

“Short-term capital asset” means a capital asset held by an assessee for not more than

Thirty – six months, however in the following cases the period shall be twelve months instead of thirty-six months.

-

- A unit of the Unit Trust of India

- Shares listed in Recognized Stock Exchange

- A unit of an equity oriented mutual fund

- Any other security listed in a recognized stock exchange in India

- A Zero Coupon bond Capital Asse

Note:

-

- Any non listed shares shall be considered as long term after twenty four months and any non listed securities shall be considered as long term after thirty six months.

- Immovable property (being land or building or both) shall be considered as long term after twenty four months.

- Capital Asset that held for more than 36 months or 24 months or 12 months, as the case may be, immediately preceding the date of transfer is treated as long-term capital asset.

Computation of Capital Gains u/s 48

Short Term Capital Gains

Particulars |

Amount |

| Full value of consideration | xxx |

| Less: a) Cost of acquisition | xxx |

| b) Cost of improvement | xxx |

| c) Selling expenses | xxx |

| Short Term Capital Gain | xxx |

Long Term Capital Gains

| Particulars | Amount |

| Full value of consideration | xxx |

| Less: a) Indexed Cost of acquisition | xxx |

| b) Indexed Cost of improvement | xxx |

| c) Selling expenses | xxx |

| Long Term Capital Gain | xxx |

- The difference between the computation of short term and long term capital gain is that, under the computation of long term capital gain instead of cost of acquisition and cost of improvement indexed cost of acquisition and indexed cost of improvement shall be taken into consideration.

“Indexed cost of acquisition” and “Indexed cost of improvement” means the cost adjusted as per cost inflation index

Note on Assets purchased before 1st April 2001

- In case a capital asset has been purchased or constructed before 1st April 2001 then cost shall be considered to be the

Ø cost incurred, or

Ø fair market value of the asset as on 1st April 2001 whichever is higher and further index of 2001-02 shall be used instead of the index of the earlier year in which purchase or construction take place.

- Any cost of improvement prior to 1st April 2001 shall not be taken into consideration.

- In case of land and building such market value cannot exceed stamp duty value as on 1st April 2001.

Meaning of Transfer u/s 2(47)

Capital gains shall be computed in case of transfer of capital asset and term transfer shall include:

-

- Sale of the asset

- Compulsory acquisition of land or building

- Conversion of capital asset into stock-in trade

- The relinquishment of the asset

- Extinguishment of any rights/asset

- The maturity or redemption of a zero coupon bond

- If any person has given possession of immovable property and has taken full payment but ownership in documents has not yet been transferred. It will also be considered to be transfer and capital gains shall be computed

Capital Gains in case of transfer of shares

Where no Securities Transaction Tax (STT) is paid:

- In case of original shares, cost of acquisition shall be amount for which the asset was purchased but if it was purchased before 1st April 2001, cost of acquisition shall be the higher of amount for which the shares were purchased or the market value as on 1st April 2001.

- If the bonus shares, cost of acquisition shall be NIL, but if the said shares were issued before 1st April 2001, cost of acquisition shall be market value as on 1st April 2001.

- If right shares, cost of acquisition shall be the amount that has been paid for purchase of such shares. If right to purchase right shares has been renounced, amount received shall be considered to be short term capital gains. Cost of acquisition for the right renounce shall be the amount paid to the person renouncing the right and amount paid to the company.

Long term capital gains shall be taxable at the rate of 20% but short term capital gain shall be taxable at normal rate.

In case of short term equity shares or the units, capital gains shall be computed as per section 111A and such capital gains shall be taxable at the rate of 15%.

Where Securities Transaction Tax (STT) is paid

- In case of long term equity shares or long term equity oriented mutual funds or units of business trust, capital gains shall be computed as per section 112A provided securities transaction tax has been paid and such capital gains shall be taxed at the rate of 10% in excess of INR 1,00,000 and indexation shall not be applicable while computing such capital gains.

- STT paid is not considered to be selling expense, hence not allowed to be deducted while computing capital gains.

Grandfathering Rule

Cost of acquisition shall be computed in the manner given below:

As per section 55(2)(ac), in case of equity shares or units of equity oriented mutual funds or units of business trust which have been sold from 1st April 2018 onwards, cost of acquisition shall be higher of,

- Cost of acquisition

or

- Lower of

a) Fair market value of such shares on 31st January 2018

b) Actual Sale value

Note: In case more than one value is available as on 31st January 2018, the highest of all such value shall be taken AND in case of mutual fund which is not listed, Net Asset Value (NAV) shall be taken into consideration.

Capital Gains on distribution of assets by companies in Liquidation (Section 46)

If any company is in liquidation and the company has distributed its assets to the shareholders in connection with liquidation, it will be exempt from capital gains.

However, if the same asset has been sold by the shareholder subsequently, its cost of acquisition shall be the amount for which the shareholder has received the asset from the company and capital gains shall be computed accordingly.

Transaction not regarded as transfer (Section 47)

The following transactions will not be regarded as transfer and therefore, no capital gains will arise:

- Transfer of any capital asset through gift or will or inheritance, etc.

- Distribution of capital assets on the partition of a Hindu Undivided Family.

- Transfer of any capital asset by holding company to subsidiary company or by subsidiary company to holding company, provided the company receiving the capital asset is an Indian company and also 100% share capital of subsidiary company is held by holding company or its business.

- Central Government to be of national importance or to be of renown throughout any State:

- Transfer of any capital asset by the amalgamating company to the amalgamated company if the amalgamated company is an Indian company.

- Any transfer of a capital asset in a transaction of reverse mortgage.

- Transfer of a capital asset by the demerged company to the resulting company, if the resulting company is an Indian company.

- Receiving of shares from an amalgamated company in lieu of shares held in amalgamating company provided the amalgamated company is an Indian company.

- Transfer or issue of shares by a resulting company in case of demerger.

- In case of conversion of bonds or debentures, etc. into shares or conversion of preference shares into equity shares, no capital gains shall be computed.

- Redemption by an individual of Sovereign Gold Bonds issued by RBI under the Sovereign Gold Bond Scheme, 2015.

- Any transfer of any of the following capital asset to the Government or to the University or the National Museum, National Art Gallery, National Archives or any other public museum or institution notified by the

- Work of art

- Archaeological, scientific or art collection

- Book

- Manuscript

- Drawing

- Painting

- Photograph, or

- Any other transaction as may be prescribed

Reverse Mortgage Loan

- Reverse Mortgage Loan (RML) enables a Senior Citizen i.e. above the age of 60 years to avail of periodical payments from a lender against the mortgage of his/her house while remaining the owner and occupying the house

- Senior Citizen borrower is not required to service the loan during his/her lifetime and therefore does not make monthly repayments of principal and interest to the lender.

- The loan amount may be used by the Senior Citizen borrower for varied purposes including up-gradation/ renovation of residential property, medical exigencies, etc. However, use of RML for speculative, trading and business purposes is not permissible.

- Maximum period of the loan is 20 years.

- Valuation of the residential property would be done at such frequency and intervals as decided by the reverse mortgage lender, which in any case shall be at least once every five years.

- The quantum of loan may undergo revisions based on such re-valuation of property at the discretion of the lender.

Income tax Provision under Section 49(1) and 49(4)

Provision under Section 49(1)

- As per Section 49(1), if any person has received an asset through any transaction mentioned under section 47 and subsequently asset was sold by him, in such cases cost of acquisition and cost of improvement of previous owner shall be considered to be cost of acquisition/improvement of the assessee and also cost of improvement by assessee shall be taken into consideration.

Provision under Section 49(4)

- According to the section 49(4), in case any individual or HUF has received gift in kind and it was taxable u/s 56, in such cases, at the time of sale, cost of acquisition of such asset shall be the value which has been taken into consideration for the purpose of computing taxable amount of gift.

Special provision for full value of consideration in certain cases (Section 50C)

- Where the consideration received or accruing as a result of the transfer by an assessee of a capital asset, being land or building or both, is less than the value adopted or assessed or assessable by any authority of a State Government (hereafter in this section referred to as the “stamp valuation authority”) for the purpose of payment of stamp duty in respect of such transfer, the value so adopted or assessed or assessable shall be deemed to be the full value of the consideration received or accruing as a result of such transfer.

- Provided that where the date of the agreement fixing the amount of consideration and the date of registration for the transfer of the capital asset are not the same, the value adopted or assessed or assessable by the stamp valuation authority on the date of agreement may be taken for the purposes of computing full value of consideration for such transfer.

- Also, the above provision is applicable only in a case where the amount of consideration, or a part thereof, has been received by way of an account payee cheque or account payee bank draft or by use of electronic clearing system through a bank account, on or before the date of the agreement for transfer.

| S. No. | Conditions | Deemed sale consideration |

|

1. |

Stamp Duty Value (SDV)> Actual Consideration

If SDV>110% of Actual Consideration In case the Stamp Duty ValueSDV<=110% of Actual Consideration |

Stamp Duty Value Actual sale consideration |

| 2. | Actual consideration > SDV | Actual sale consideration

|

| 3. | A Value Ascertained by Valuation Officer>SDV | SDV |

| 4. | The Value Ascertained by Valuation Officer<SDV | Value Ascertained by Valuation Officer |

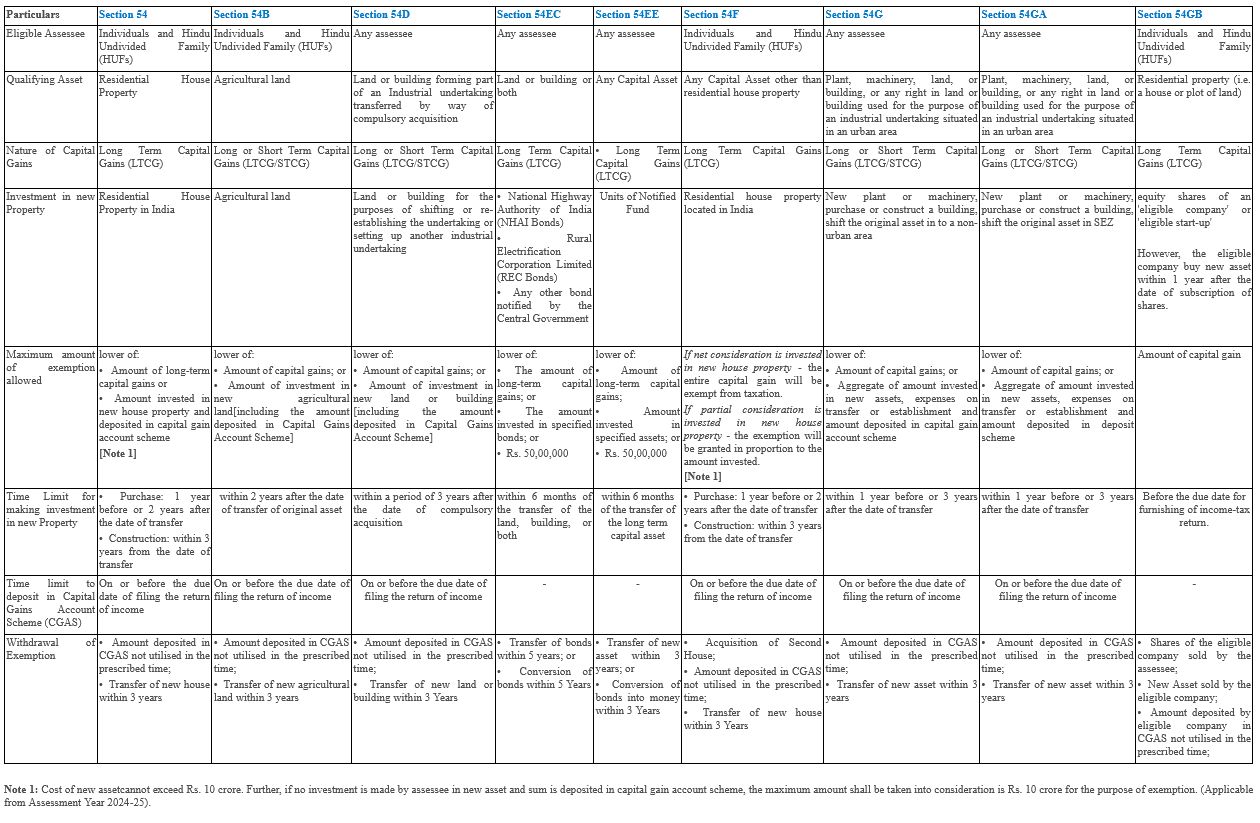

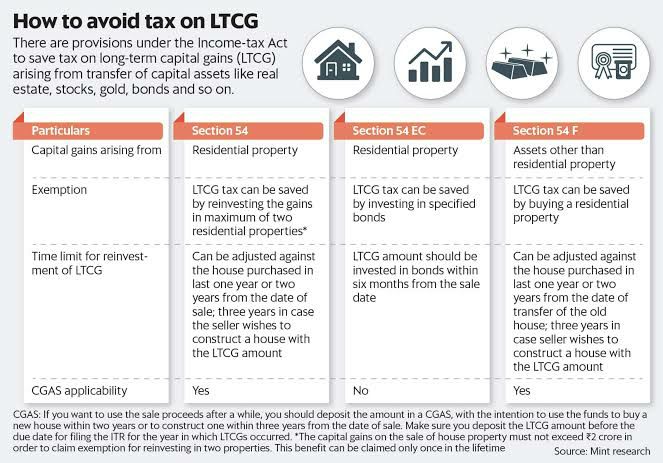

Exemption of Capital Gain [Section 54 to 54F]

| S.No | Particulars | Section 54 | Section 54B | Section 54D | Section 54EC | Section 54F |

| 1. | Eligible Assessee | Individual/ HUF | Individual/ HUF | Any assessee | Any assessee | Individual/ HUF |

| 2. | Asset transferred | Residential House | Urban agricultural Land | L&B forming part of as industrial undertaking | Land or Building Or Both (LTCA) | Any LTCA other than residential House |

| 3. | Qualifying Asset in which CG has to be invested | One/ Two Residential House in India, at the option of asssessee, where CG does not exceed ₹2 Crore | Land for being used for Agricultural purposes (Urban/ Rural) | Land and Building | Bonds of NHAI or RECL or any other bond notified by CG (Redeemable

after 5 years) |

One Residential House situated in india. |

| 4. | Time Limit For purchase | Purchase before 1 year or 2 year after the date of transfer or construct within 3 years | Purchase within a period of 2 years after the date of transfer. | Purchase within a period of 3 years after the date of transfer. | Purchase within a

period of 6 months after the date of transfer |

Purchase before 1 year or 2 year after the date of transfer or construct within 3 years |

| 5. | Amount of Exemption | Cost of New

Residential house or 2 houses, as the case may be or CG whichever is lower is exempt |

Cost of new agricultural land or CG, whichever is lower is exempt | Cost of new asset or CG whichever is lower is exempt | CG or amt. invested in specified bonds, whichever is lower | Cost of New residential house >= Net sales consideration of original asset, entire Capital gain is exempt. |

Income tax rate in case of capital Gain regulation in India

Ready Recknor for calculating capital gains tax for all class of Assets.

Written by the IFCCL -Team

IFCCL provides our clients adequate guidance and assistance as they deal with internal audits as well as government audits of various corporate problems (business incorporation, statutory audits, ROC compliance, and company winding-up) in India. Please get in contact with us if you have any questions or would need more information concerning with Capital gain.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.