All About Right Issue to NRI’s

Table of Contents

RIGHTS ISSUE TO NRIS

BRIEF INTRODUCTION

- Right issues refers to the further issuance of securities to existing shareholders and such an approach is used in rasiing additional capital for the corporate entity. A public Ltd. Entity is allowed to issue rights shares and the same is governed by the section 62(1) of the Companies Act, 2013.

- A rights issue is distinguished by the actual fact that it’s limited to the company’s current shareholders. It can be a public firm that’s listed or unlisted. Also, the offer can allow the shareholders to relinquish their rights in the name of some other shareholders.

- Existing shareholders of the Company will gain from the issue of right shares since they will be able to apply for the shares at a reduced price while keeping their voting rights. Issuance Company of rights shares can be used to raise a considerable amount of capital for a firm.

MANDATORY RIGHT ISSUE

- It is obligatory for each company registered under Companies Act, 2013 to follow the provisions of Companies Act, 2013 and any non-compliance may cause penalties and punishments.

- As per the section 62 of the Companies Act, 2013, the provisions for “Further Issue of Share Capital” has been provided. Thus, whenever a corporation, already having share capital, proposes to raise further capital by way of issue of shares, then the said entity is required to make an initial offer to –

- To existing equity shareholders, i.e., persons who are holding equity shares on the date of offer;

- To the employees of the entity, and the same be provided under a scheme of ESOP, subject to the passing of special resolution by corporate and some other conditions.

- To a number of persons, provided the same is authorised by passing of a special resolution, and the consideration is received either in cash or kind, and the value of such shares has been determined under the valuation report of a registered valuer.

Thus, the issuance of right shares stands as an obligation of the public company, where they look for raising funds thorugh issuance of further securities.

What is procedure for Rights Issue

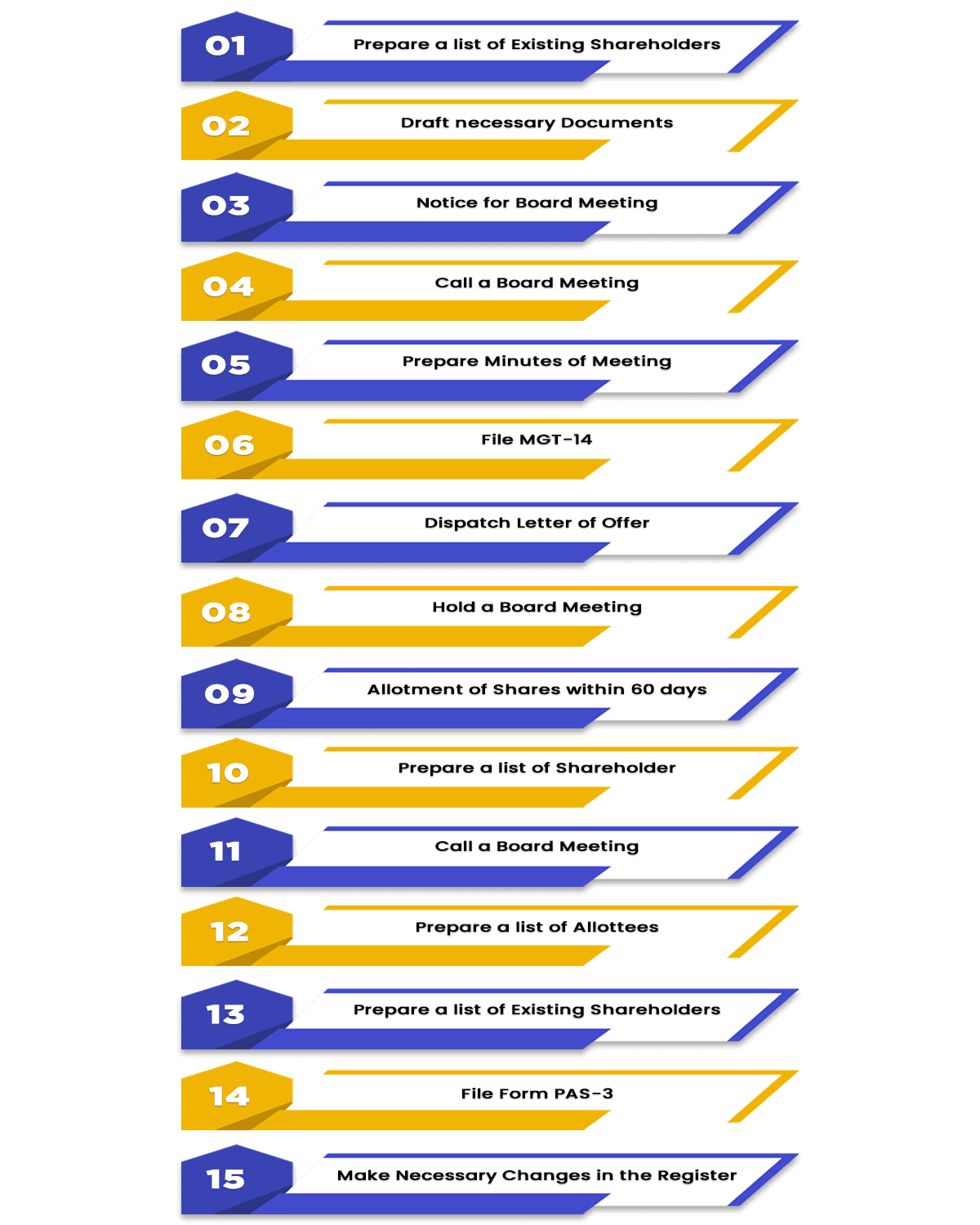

As per the Sub section (1) of Section 62 of the CO. Act 2013, the procedure for issue of shares is as under:

- Issue of notice of Board meeting: As per sub section (3) of Section 173(3) of the CO. Act 2013, the board meeting notice must be given at least Seven days before to the meeting and must include the agenda.

- Hold a meeting the First Board Meeting: The first Board meeting is conducted, and the resolution authorising the issuance of rights shares is approved. Because the rights issue does not require shareholder approval, the board can proceed with the issue.

- Issue Letter of Offer: Following the passage of the resolution, a letter of offer is sent to all shareholders via registered mail or speed mail. A Time period of Fifteen to Thirty days has been set for shareholders to accept the offer, meaning that the most time they can take to accept the offer is Thirty days and the least time is Fifteen.

If the offer is not accepted before the deadline, it is considered declined. The offer must be open for at least three days after the letter of offer has been issued.

- Submitting Form MGT – 14 : Within 30 days of the board resolution being made, the company must file the MGT-14. For a public limited company, the MGT 14 form is required. MGT 14 must be supported by a true certified copy of the Board Resolution.

- Receive application money: Company shareholders shall have to share the accepted application along with required application money.

- Convene Second Board Meeting: The Company shall convene 2nd board meeting, which must be announced seven days in advance. A quorum must be present, and the resolution authorising the allotment of shares must be approved. The allotment of shares must be completed within Sixty days of receiving the application money for the same once the resolution for allotment of shares has been passed.

- Submit Forms with ROC: Within 30 days of the allotment of the shares, the company must file Form PAS -3 with the Registrar of Companies. The form must include a certified accurate copy of the Board Resolution as well as a list of the allottees. In addition, for both the allotment and issuing of shares, the MGT – 14 must be filed.

- Needed to Issue of Share Certificates: The share certificates must be issued; If the shares are held in Demat form, the corporation must immediately notify the depository of the allotment of shares.

If the shares are held in tangible form, share certificates must be issued within two months of the date of the allotment. At least 2 directors must sign the share certificate. Form SH -1 i.e share certificates must be issued.

RIGHT ISSUE TO NON-RESIDENTS

- If shares of a corporation are held by a Non-Resident then whether the corporate is required to make the right issue of shares to such non-resident shareholders as well?

- Since, Company law requires right issue of shares to existing shareholders, therefore, right issue is obtainable to all or any resident and non-resident shareholders.

- However, the instructions for issuance of right shares to Non-resident has been provided Master Direction – Foreign Investment in India, being issued vide RBI/FED/2017-18/60 FED Master Direction No. 11/2017-18.

- As per the Para 6.11 of the Master Directions, the provisions regarding “Acquisition through rights issue or bonus issue” has been provided. Under this, an NRI owing stock in an Indian company, may invest in capital instruments (other than share warrants), being issued by the said corporate, in the form of rights or bonus issue, however, the same shall be available, subject to fulfilment of subsequent conditions:

- Offer must be in compliance with the provisions of Companies Act, 2013;

- Such issue won’t end in a breach of the sectoral cap applicable to the company.

- Shareholding of such person, after the issuance of rights issue or bonus, must be well within the limit prescribed in the FEMA regulations.

- Shares, being acquired as right issue, shall be subject to the conditions and restrictions, applicable to the original holding, in respect of reparability of the holding;

- Rights, being granted NRIs, by a listed Indian entity, shall be made at a price, being determined by such entity in general.

- The rights issued to an individual resident outside India by an unlisted Indian company shall not be at a price but the worth offered to persons resident in India.

- Such an investment made through a rights issue is subject to the terms and conditions in effect at the time of the difficulty.

- The consideration paid in respect of acquisition of such shares, shall be made using banking channels or the funds lying in an NRE/FCNR(B) account, being maintained in accordance with the Foreign Exchange Management (Deposit) Regulations, 2016.

- If the first investment was made on non-repatriation basis*, the consideration for right issue of shares may additionally be paid by debit to the NRO account maintained in accordance with the foreign exchange Management (Deposit) Regulations, 2016.

- Also to note that –

- If an individual residing outside of India exercises a right that was issued while he or she was a resident of India, shares acquired as a result of the right issue must be held on a non-repatriation basis.

- With effect from November 12, 2002, the Indian entity, on an application, allot additional shares to existing shareholders, who are NRI, under offer over and above their respect rights entitlement subject to certain limits and conditions.

VALUE OF SHARES UNDER RIGHT ISSUE

As discussed earlier, the businesses are free to decide on the value of right issue, however, the same is possible on fulfilment of following conditions:

- If unlisted Company, securities must be offered to non-residents at a price that’s not but the worth offered to residents during a rights issue.

- In case of publicly traded enterprises, the value shall be decided by the corporate.

RENOUNCEMENT OF RIGHT SHARES TO NON-RESIDENTS

-

- According to the companies Act of 2013, existing shareholders can accept, deny, or renounce their right to subscribe a rights offering in favour of a 3rd party if a rights offer is created. This renunciation will be made within the name of an Indian citizen or a foreigner.

- Thus, a person, being regarded as NRI, is eligible to renounce their shares offered under right issue. Renunciation is done either fully or part thereof in favour of someone named by them.

-

Pricing guidelines for renunciation of right issue

-

- Investments in India through equity instruments by someone resident outside India is governed by foreign exchange Management (Non-debt Instruments) Rules, 2019 (“NDI Rules”)

- As per the explanation provided under the Rule 7 and Rule 6.11.4, a person, being resident outside India, is elibiel to acquire shares under right issue, under the ambit of renunciation of rights. However, the price of such right issue shall be determined in accordance with the guidelines mentioned above. Therefore, price shall be:

- Where the issuing entity is an unlisted Indian company, the price of offer, shall be the price determined in respect of persons residing in India, and

- Where the entity is a listed company, the price of right issue, be determined by the corporate itself.

- Since, no restriction was provided for pricing therefore, non-resident shareholders were ready to make major investments in India at a fraction of the fair market price.

- To curb this example, an amendment was introduced in Rule 7 of NDI Rules vide notified the foreign exchange Management (Non-debt Instruments) (Second Amendment) Rules, 2020 issued on 27th April, 2020. Amendment deleted explanation to Rule 7 of NDI Rules and inserted a replacement Rule 7A which states that:

‘a person resident outside India who has acquired a right from an individual resident in India who has renounced it should acquire equity instruments (other than share warrants) against the said. - As per the Rule 21(2)(a)(ii) of the NDI Rules, where the equity shares have been issued by an entity to an NRI, then the same be issued at a price, which shall not be less than:

- In case of listed company, the worth discovered as per with the SEBI Guidelines or just in case of a Company inquiring a delisting process as per the SEBI (Delisting of Equity Shares) Regulations, 2009;

- For an unlisted Indian company, the valuation be done as per any of the internationally accepted pricing methodology and the same be made on arm’s length basis, being duly certified by a CA or a Merchant Banker, being registered with Securities and Exchange Board of India.

- While the Amendment has made a long-awaited modification to the worth parameters within the case of residents renouncing a rights offer, it doesn’t cover a situation during which an existing non-resident investor renounces a offer entitlement in favour of another non-resident investor.

- it’s critical that these clarifications be provided so as to confirm that no equity instruments be purchased for fewer than their fair market price.

REPORTING REQUIREMENT IN THE MATTER OF RIGHT ISSUE

- In the Reporting requirement, in the matter of Right Issue has been provided under the Rule 4 of the FEMA (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019.

- Unless otherwise provided, all reporting with relevancy issue of right shares shall be made through or by an Authorised Dealer Bank, because the case could also be.

- As per Rule 4 of FEM (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019, An Indian company issuing equity instruments to an individual resident outside India and where such issue has been made in accordance with the Foreign Direct Investment,

- the same shall report in Form FC-GPR. The Form FC-GPR is required to be filed within 30 days from the date of issuance of such equity shares.

FAQ’s on Rights Issue to NRI’s

Q.: Is it possible to issue rights/bonus shares to non-resident person ?

Yes, Indian corporations are free to issue rights/bonus shares to existing Non-Residents shareholders. The issuing Co. must required sure that the issuance of such rights/bonus shares does not exceed the Non-Residents India sectoral cap limit.

Q.: Can a remote investor invest in Rights shares issued by an Indian company at a discount?

There aren’t any restrictions under FEMA for investment in Rights shares issued at a reduction by an Indian company under the provisions of the companies Act, 2013. The offer on a rights basis to the person resident outside India shall be:

- just in case of shares of an organization listed on a recognized stock exchange in India, at a price, as determined by the company; and

- within the case of shares of a corporation unlisted on a recognized exchange in India, at a price, which isn’t but the value at which the offer on the correct basis is created to resident shareholders.

Q.: Whether the entity be required to take RBI approval, in respect of renunciation of rights shares?

No, the renunciation of rights shares can be made and carried out, in accordance with the instructions provided in Para 6.11 of Master Direction – Foreign Investment in India, dated January 4, 2018, along with the Regulation 6 of FEMA, Regulation.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.