FAQs ON DEDUCTIONS UNDER SECTION 80C, 80CCC, 80CCD & 80D

Table of Contents

FAQs ON DEDUCTIONS UNDER SECTION 80C, 80CCC, 80CCD & 80D

- Are taxpayers allowed to say 80C deductions while filing taxation return?

Claim for 80C deduction is allowed while filing income return before the top of that Assessment Year.

- Which year will the investments reflect within the tax return?

Assume a taxpayer made investments in accordance with Section 80C guidelines on 30th April 2019. Then, he or she is going to be able to claim tax exemption on such investments within the Assessment Year 2019-2020.

- Can someone claim an 80C deduction on the life assurance premium paid to personal insurance aggregator?

Yes, deduction under Section 80C is accessible for all times insurance premiums paid to any insurance aggregator recognized by IRDAI (Insurance Regulatory and Development Authority of India). it’s applicable for both public and personal sector companies.

-

Are donations eligible for tax exemptions under Section 80C?

Donations made to specific institutions and funds are eligible for tax exemption under this section.

- Can taxpayers invest in additional than one investment policy and claim Rs.1.5 lakh exemption for every investment?

No, an individual taxpayer is allowed claim a maximum tax exemption of up to Rs.1,50,000 on cumulative basis, after considering the investments made towards tax-saving instruments under Section 80C

- Can I claim the 80C deductions at the time of filing return just in case I’ve got not submitted proof to my employer?

Proofs for creating investments are submitted to the employer before the tip of an yr (FY) so the employer considers these investments while determining your taxable income and therefore the deduction that has to be made. However, whether or not you miss submitting these proofs to your employer, the claim for such investments made is done at the time of filing your return of income as long as these investments are made before the top of the relevant FY.

- I have made an 80C investment on 30 April 2018. that year am I able to claim this investment as a deduction?

You can claim deduction for investments made within the return of income for the year within which you’ve got made the investment. Therefore, if you’ve got made the investment on 30 April 2018, you’ll be eligible to say such investment as a deduction during FY 2018-19.

- I have availed a loan from my employer for pursuing education. am I able to claim the interest paid on such loan as a deduction under Section 80E?

A deduction of interest paid on education loan under Section 80E are often made on condition that the loan has been availed from a financial organization for pursuing education. Therefore, availing a loan from your employer won’t entitle you to assert the interest under Section 80E.

- Is there any restriction or maximum limit up to which I can claim a deduction under Section 80E?

Law has not prescribed any upper limit for creating a claim of deduction under Section 80E. Hence, the particular interest paid during a year will be claimed as a deduction.

-

Can an organization or a firm take the advantage of Section 80C?

The provisions of Section 80C apply only to individuals or a Hindu Undivided Family (HUF). Hence, an organization or a firm cannot take the good thing about Section 80C.

- I am paying insurance premium to a non-public underwriter. am I able to claim 80C deduction for the premium paid?

Deduction under Section 80C is on the market in respect of insurance premium paid to any insurer approved by the Insurance Regulatory and Development Authority of India, whether public or private. Hence, the amount you’re paying also will facilitate your claim an 80C deduction.

- In which year am I able to claim deduction of the taxation purchased purchase of a house property

You can plow ahead claiming the revenue enhancement for purchase of a house within the year during which the payment is formed towards tax under Section 80C.

- Can a corporation claim a deduction for donations made under Section 80G?

Any taxpayer, who is making donations towards specified institutions, funds etc., shall be eligible to assert a deduction under Section 80G.

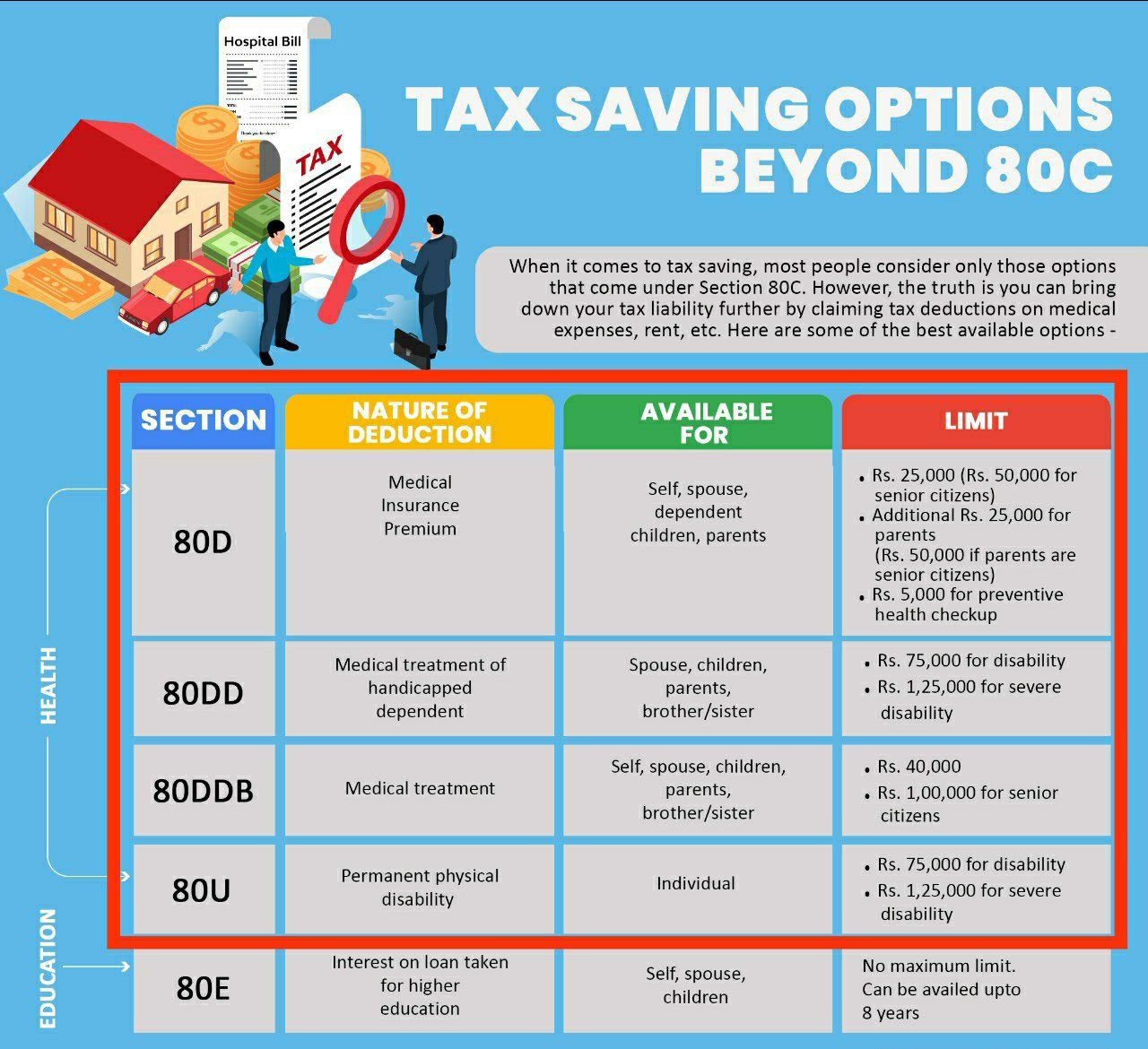

- I am paying medical payment for a medical policy taken in my name, my wife and youngsters. I’m also paying premium on a medical policy taken within the name of my parents who are above 60 years. am I able to claim a deduction for both premiums paid?

The premium you’ve got paid on the policy taken for yourself, spouse and kids are eligible for a deduction under Section 80D up to a maximum of Rs 25,000. additionally, to the present, you may even be eligible to assert deduction of premium paid on the policy taken for your adult parents up to a maximum of Rs 50,000. Hence, you’ll be able to claim both premiums paid as a deduction under Section 80D.

- Is my FD interest exempt under Section 80TTB?

If you’re an oldster above 60 years old, then your interest income from a hard and fast Deposit is exempt under Section 80TTB.

-

What does one mean by 80C deduction under chapter VI A?

Income tax department allows reducing of the taxable income of the taxpayer just in case the taxpayer makes certain investments or eligible expenditures allowed under Chapter VI A. 80C allows deduction for investment made in PPF , EPF, LIC premium , Equity linked saving scheme, principal amount payment towards home equity loan, tax and registration charges for purchase of property, Sukanya Smriddhi Yojana (SSY) , National saving certificate (NSC) , adult savings scheme (SCSS), ULIP, tax saving FD for five years, Infrastructure bonds etc.

- How to calculate deduction u/s 80c?

For section 80C- the number of eligible investment or expenditure as specified is fully allowed for deduction subject to the limit of Rs 1.5 lakh.

The limit of Rs 1.5 lakh deduction of Section 80C includes 80CCC (contribution towards pension plan) and 80CCD (1), 80CCD (1b) and 80CCD (2).

Section 80CCCD (1) may be a contribution towards the National pension scheme by the worker or self-employed and is restricted to 10% of salary (basics + DA) or 20% of gross total income for self-employed.

Section 80CCD (1b) provides additional deduction of Rs 50,000 for contributions towards NPS, Atal pension Yojana etc. Such a deduction can be availed above the amount of Rs 1.5 lakh. Thus, the total of deduction including 80C and 80CCD (1b) are often maximum Rs 2 lakh for one year.

Section 80CCD (2) is deduction allowed to salaried for contributions made by their employer for NPS, this is often also allowed at 10 you look after salary (basic +DA). However, it’s important to notice that there’s no upper limit in 80CCD (2)

Hence for investment in 80C only, the limit is Rs 1.5 Lakh. For investment together in 80C, 80CCD (1) and 80CCD (1b), one may invest up to Rs 2 lakh in total. Whereas, a salaried employee can avail more deduction without restriction of limit of Rs 2 lakh under section 80CCD (2) if the employer contributes towards NPS account subject to 10% of salary.

Further please note that per Budget 2020, any contribution towards EPF, NPS and superannuation are going to be added to the salary as “perquisites” and taxable under salaries within the hands of employees.

-

- Can you claim HRA under section 80?

Yes, if you are doing not receive HRA as a component of a salary component, rent paid is claimed as deduction under section 80GG. However, the utmost amount of deduction allowed is Rs 60,000 each year.

- what’s 80GG in income tax? What is rent paid under 80GG?

80GG allows you to say deduction for rent paid whether or not your salary doesn’t include HRA component or by self-employed individuals having income aside from salary. The condition is that you just mustn’t own any residential accommodation within the place of residence to assert deduction under 80GG.

-

The way to calculate 80GG? How to claim 80GG?

80GG deduction are allowed as lowest of below mentioned:

-

- Rs 5,000 per month

- 25% of the adjusted total Income (excluding long-term capital gains, short-term capital gains under section 111A and Income under Section 115A or 115D and deductions under 80C to 80U. Also, income is before making a deduction under section 80GG).

- Actual rent less 10% of Income

- Who can claim deduction in 80GG?

Deduction under 80GG is on the market for workers who don’t get HRA as a component of salary due to jobs within the informal sector or to self-employed persons. The person claiming this deduction mustn’t own a house within the place of residence.

- What is section 80CCD?

80CCD may be a subsection of 80C which allows deduction for contributions to national pension schemes as notified by the central government. The deduction is allowed for contributions made by an employee, employer or voluntary self-contribution. Overall limit of deduction allowed in section 80C is Rs 1.5 lakh plus a further deduction of Rs 50,000 u/s 80CCD (1b) for self-contribution to NPS or Atal pension yojana.

- What is section 80CCD (1b)?

Section 80CCD (1b) specifically deals with contributions made by an individual (employee or self-employed) to pension schemes as notified by the central government. Such a section provides for an additional deduction of Rs 50,000, above the amount of Rs 1.5 Lakh. Thus, a taxpayer can claim total deduction of Rs 2 lakh by making investments in 80C and contribution for national pension scheme u/s 80CCD (1b)

- What is section 80CCD (1)?

Section 80CCD (1) could be a deduction for workers similarly as self-employed for creating contributions to the National Pension scheme. An employee can claim deduction under 80CCD (1) at a maximum of 10% of basic salary plus dearness allowance. For self-employed, the limit for deduction is 20% of their income subject to Rs 1.5 lakh maximum limit of section 80C.

- What is section 80CCD (2)?

Section 80CCD deals with tax deductions available to employers with relation to contributions made to the pension scheme for its employees. i.e., if your employer contributes to its employee’s retirement savings account, deduction, maximum up to 20% of total income of the employer are often availed.

-

What is section 80TTB?

Section 80TTB provides deduction up to Rs 50,000 on interest income earned on fixed deposit or bank account specifically to Senior citizens.

- What is rebate u/s 87A?

A rebate under section 87A is one amongst the tax provisions that help low income earning taxpayers reduce their Income Tax liability. Taxpayers earning an income below a specific limit have the advantage of paying marginally lower taxes. A Taxpayer can claim the good thing about rebate under section 87A for FY 2019-20 and 2020-21 given that the subsequent conditions are satisfied:

-

- You are a resident individual

- Your total income after reducing the deductions under chapter VI-A (Section 80C, 80D and then on) doesn’t exceed Rs 5 lakh in an FY

The tax rebate is restricted to Rs 12,500. This means, if your total tax payable is a smaller amount than Rs 12,500, then you may not must pay any tax. Do note that the rebate is applied to the full tax before adding the health and education cess of 4%.

-

Who is eligible for rebate u/s 87a?

A Taxpayer can claim the good thing about rebate under section 87A for FY 2019-20 and 2020-21 given that the subsequent conditions are satisfied:

- You are a resident individual which implies HUF and firms cannot claim this rebate.

- Your total income after reducing the deductions under chapter VI-A (Section 80C, 80D and then on) doesn’t exceed Rs 5 lakh in an FY

Income under the head salaries for The FY 2024-25

FINISH YOUR E-FILING free WITH IFCCL

- IFCCL makes it very easy to E-File your ITR

- E-Filing takes only some minutes

- Our experts facilitate and provide services on live chat and email

- Easy and Accurate ITR Filing on IFCCL

- File in 7 Mins | Minimal Data Entry | 100% Paperless

- START YOUR legal instrument NOW

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.