Read All about Deduction U/s 80C, 80CCC, 80CCD & 80D

Table of Contents

Section 80C, 80CCC, 80CCD, and 80D deductions:

The tax department provided various deductions from taxable income in Chapter VI A deductions in order to encourage savings and investment among taxpayers. As 80C is the most well-known, other deductions are useful to reduce tax liability for taxpayers. Let us have a clear understanding of these deductions.

Section 80C – Investment deductions:

Section 80C of the Income Tax Act of India identifies a number of expenses and investments that are excluded from paying income tax. It enables an annual maximum deduction of Rs.1.5 lakh from the total taxable income of an investor.

Individual taxpayers and Hindu Undivided Families are the only ones who can use Section 80C. Corporate bodies, partnership companies and other companies are not eligible to use Section 80C tax exemptions.

Section 80C is one of the most well-known and popular sections among taxpayers since it allows them to lower their taxable income by making tax-saving investments or incurring qualified costs. Each year it allows a maximal allowance of Rs 1.5 lakh of total income for taxpayers.

Individuals and HUFs can both take advantage of this deduction. This deduction is not available to corporations, partnership firms, or LLPs. Subsections 80CCC, 80CCD (1), 80CCD (1b), and 80CCD (1c) are all contain in section 80C. (2).

It’s worth noting that the overall ceiling for claiming deductions, including subsections, is Rs 1.5 lakh, with an extra deduction of Rs 50,000 allowed under section 80CCD (1b).

Subsections of Section 80C:

Deductions under Section 80Care of the Income Tax Act of India are divided into sub-sections. These are as follows:

| Tax saving sections | Eligible investments for tax exemptions |

| Section 80C | Investments in Provident Funds such as EPF, PPF, etc., payment made towards life insurance premiums, Equity Linked Saving Schemes, payment made towards the principal sum of a home loan, SSY, NSC, SCSS, etc. |

| Section 80CCC | Payment made towards pension plans, as well as mutual funds. |

| Section 80CCD(1) | Payment made towards certain Government-backed schemes such as National Pension System, Atal Pension Yojana, etc. |

| Section 80CCD(1B) | Investments of up to Rs.50,000 in NPS is considered for exemption under this section. |

| Section 80CCD(2) | Employer’s contribution towards NPS (up to 10%, comprising basic salary and dearness allowance, if any) is exempted under this category. |

Investments that allow for a deduction under Section 80C of the Income Tax Act:

| Investment options | Interest | Minimum lock-in period | Assured return | Associated risk |

| ELSS | 12% to 15% (depending on market fluctuation) | 3 years | No | High |

| NPS | 8% to 10% | Till the investor reaches 60 years of age (retirement) | No | High |

| SCSS | 8.60% | 5 years | Yes | low |

| PPF | 7.90% | 15 years | Yes | Low |

| NSC | 7.9% | 5 years | Yes | Low |

| ULIP | 8% to 10% (depending on market fluctuation) | 5 years | No | Moderate |

| Fixed deposit | Up to 8.40% | 5 years | Yes | Low |

| Sukanya Samriddhi Yojana | 8.50% | 8 years | Yes | Low |

Life insurance premiums:

Premiums paid for life insurance policies qualify for tax benefits under the 80C limit. These exemptions apply to insurance owned by the policyholder, his or her spouse, dependent children, and so forth. Hindu Undivided Exemptions are available to family members as well.

Currently, an annual premium of up to 10% (of the total sum assured of the insurance policy) is tax free under this plan. This clause was changed on April 1, 2012; formerly, premiums of up to 20% (of the total guaranteed) were eligible for a tax deductible under Section 80C.

Public Provident Fund:

Section 80C allows for a tax credit for contributions to the Public Provident Fund (PPF). The highest deposit limit for Public Provident Funds is Rs.1,50,000, allowing an investor to claim the entire amount placed as an exemption under the Income Tax Act.

Under Section 80C of the Income Tax Act, any voluntary contribution made by the employee to the supplied fund is likewise tax deductible.

Rural Bonds from NABARD:

The National Bank for Agriculture and Rural Development (NABARD) is a financial institution that focuses on agriculture and rural development. Under the Income Tax Act of India, NABARD Rural Bonds are eligible for tax exemption. The highest amount that can be deducted is Rs.1.5 lakh under section 80C of the Income Tax Act.

Unit Linked Insurance Plans (ULIPs):

When compared to traditional insurance policies, unit-linked insurance plans provide better long-term returns. They’ve grown in popularity in recent years as a result of the tax benefits provided by Section 80C of the Income Tax Act of 1961. Tax exemptions of up to Rs. 1.5 lakh are available to investors under Section 80C of the Income Tax Act.

Certificate of National Savings:

One of the most popular tax-saving vehicles for risk-averse individuals is the NSC, or National Savings Certificate. NSC interest is compounded semi-annually, and the maximum maturity duration is between 5 and 10 years. Investors are not have to adhere to any limits on the total amount invested in NSC in a financial year; however, Section 80C will only exempt up to Rs.1.5 lakh every financial year.

Tax Saving FD:

Tax Saving FDs are fixed deposit products issued by banks and post offices that qualify for the Section 80C tax deduction. These FDs have a 5-year lock-in term and a maximum tax exemption of Rs.1.5 lakh (on the principal amount). The returns on such instruments, on the other hand, are taxed.

EPF – Employee Provident Fund (EPF)

Employee Provident Fund (EPF) returns, including interest, are exempt from taxation under Section 80C of the Income Tax Act of 1961. It is only available to employees who have been with the company for at least 5 years. Individuals who make voluntary contributions to their EPF accounts are entitled for Section 80C tax exemptions.

Bonds for infrastructure:

Tax breaks on infrastructure bonds are available under Section 80C of the Income Tax Act, if the investment is equal to or greater than Rs.20,000. These long-term secured bonds are still subject to the Rs.1.5 lakh restriction.

Equity-Linked Saving Scheme:

For up to the maximum level, equity linked savings schemes, or ELSS, fall under Section 80C’s exemption category (Rs.1.5 lakh). A three-year lock-in period is required for these investment schemes.

Senior Citizens Savings Scheme:

Any contributions made to the Senior Citizens Saving Scheme (or SCSS) are tax deductible up to the maximum allocated 80C limit, which is Rs. 1.5 lakh. Individuals over the age of 60 (people opting for voluntary retirement scheme are eligible to participate in SCSS after the age of 55) years are eligible to receive benefits from SCSS, which has a 5-year minimum lock-in period.

Principal repayment on a home loan has been made:

Only payments paid toward the principal portion of home loan EMIs are eligible for Section 80C deductions. However, in order to take advantage of this benefit, the borrower must comply with certain conditions. These are as follows:

- Exemptions are only available if the property’s construction is complete.

- If the property is transferred within 5 years of possession, it is no longer eligible for the tax exemptions given by Section 80C of the Income Tax Act of 1961.

- If a handover is done after 5 years of possession, any sum claimed as a tax deduction should be taxable in the transfer year. If you don’t comply with this clause, you’ll be kicked out of Section 80C’s guidelines.

Charges for stamp duty and registration:

The two most significant costs associated with acquiring property ownership are stamp duty and registration fees. The government of India permits stamp duty and registration fees paid for house purchase to be deducted from tax burden up to the 80C limit. Exemptions, on the other hand, can only be claimed in the year in which the duties are paid; otherwise, it will not be qualified for the Section 80C deduction.

Sukanya Samriddhi Yojana:

Sukanya Samriddhi Yojana is a savings scheme created to help girls meet their financial needs for education and marriage. This account can be opened by parents or legal guardians of a girl child under the age of ten, and parents of two or more (only in the case of twins) girls can also invest in this plan. Section 80C allows you to deduct the interest you earn from this investment scheme.

Section 80C contains a number of instruments about which every investor should have a good understanding. The benefits provided by this statute can assist save a significant amount of money on one’s tax bill.

Section 80CCC – Section 80CCD – Pension contribution.

| Section | Eligible investments for tax deductions |

| 80 C | 80C allows deduction for investment made in PPF , EPF, LIC premium , Equity linked saving scheme, principal amount payment towards home loan, stamp duty and registration charges for purchase of property, Sukanya smriddhi yojana (SSY) , National saving certificate (NSC) , Senior citizen savings scheme (SCSS), ULIP, tax saving FD for 5 years, Infrastructure bonds etc |

| 80CCC Deduction for life insurance annuity plan. | 80CCC allows deduction for payment towards annuity pension plans Pension received from the annuity or amount received upon surrender of the annuity, including interest or bonus accrued on the annuity, is taxable in the year of receipt. |

| 80CCD (1) Deduction for NPS | Employee’s contribution under section 80CCD (1) Maximum deduction allowed is least of the following

|

| 80CCD (1b) Deduction for NPS | Additional deduction of Rs 50,000 is allowed for amount deposited to NPS account

Contributions to Atal Pension Yojana is also eligible for deduction. |

| 80CCD (2) Deduction for NPS | Employers contribution is allowed for deduction upto 10% of basic salary plus dearness allowance under this section. Benefit in this section is allowed only to salaried individuals and not self employed. |

Here are some investment possibilities that qualify for an 80C deduction. They not only assist you in lowering your taxes, but also in increasing the value of your assets. Below is a quick comparison of the many alternatives.

| Investment options | Average Interest | Lock in period for | Risk factor |

| ELSS funds | 12% – 15% | 3 years | High |

| NPS Scheme | 8% – 10% | Till 60 years of age | High |

| ULIP | 8% – 10% | 5 years | Medium |

| Tax saving FD | 7% – 8% | 5 years | Low |

| PPF | 7.10% | 5 years | Low |

| Senior citizen savings scheme | 7.4% | 5years (can be extended for other 3 years) | Low |

| National | 6.8% | 5 years | Low |

| Sukanya Samriddhi Yojana | 8.4% | Till girl child reaches 21 years of age (partial withdrawal allowed when she reached 18 years) |

Low |

Get income tax savings from a tax specialist to help you file.

You may have deductions or assets that are eligible for the 80C deduction but haven’t provided documentation to your employer. TDS deductions may be increased as a result of this. You can still claim these deductions if you have the proofs with you during e-filing.

Interest on Savings Accounts (Section 80 TTA):

Interest on a savings bank account is deducted from gross total income.

If you are an individual or a HUF, you can deduct up to Rs 10,000 from your interest income from a bank, co-operative society, or post office savings account. Include interest from a savings account in your other sources of income. Interest income from fixed deposits, recurring deposits, or corporate bonds is not eligible for the Section 80TTA deduction.

Section 80GG – House Rent Paid

House Rent Deduction Payable Where HRA does not get

- The deduction of Section80GG for rent paid if HRA is not received is available. The taxpayer, spouse or minor child should not own housing at the place of work.

- The taxpayer must have no residential self-occupied property elsewhere.

- The taxpayer shall live and pay rent.

- Anyone can take advantage of the deduction.

- The lesser of the following is the deduction available.

Deduction available is the least of the following:

- The loan is paid less than 10% of the total adjusted income.

- Rs 5,000/- per month.

- 25% of total adjusted income*.

*After adjusting the Gross Total Income for certain deductions, exempt income, long-term capital profits, and non-resident and foreign company income, an adjustable Gross Total Income is achieved.

Because the restrictions are auto-calculated, using an online e-filing software can be quite simple. There are therefore no complicated calculations you need to worry about.

A deduction of 5 000 Rs per month from Rs 2,000 per month was levied from FY2016-2017 available.

Section 80E – Education interest credit:

Interest deduction on higher education loan:

Individuals are entitled to a tax deduction for interest paid on loans used to pursue higher education. This loan could have been taken for the taxpayer, his or her spouse or children, or for a student over whom the taxpayer has legal custody.

The 80E deduction is allowed for up to 8 years (starting with the year in which the interest begins to be returned) or until the total interest is repaid, whichever comes first. The maximum sum that can be claimed is unlimited.

Section 80EE — Interest on Home Loan

Deductions for First-Time Home Buyers in Fiscal Years 2017-18 and 2016-17 If the loan was taken in FY 2016-17, this deduction is available in FY 2017-18.

The interest component of a residential house property loan obtained from any financial institution is eligible for income tax benefits under Section 80EE. This part allows you to claim a deduction of up to Rs. 50,000 per financial year. You can claim this deduction until the debt is completely paid off.

To be eligible for a deduction, you must meet certain criteria.

- The residence should be worth no more than Rs 50 lakhs.

- The housing loan must be less than Rs 35 lakhs.

- A Financial Institution or a Housing Finance Company must approve the loan.

- The loan must be approved between April 1, 2016 and March 31, 2017.

- You must not own any other dwelling property as of the loan’s approval date.

Only home-owners (individuals) with only one house property on the date of loan sanction are eligible for the deduction under section 80EE. The property must be worth less than Rs 50 lakh, and the mortgage must be for less than Rs 35 lakh. The loan acquired from a financial institution must have been sanctioned between 1 April 2016 and 31 March 2017. On top of the deduction of Rs 2 lakh (on the interest component of your house loan EMI) allowed under section 24, you can deduct an extra Rs 50,000 on your home loan interest.

Financial years 2013-14 and 2014-15 The deduction provided under this section throughout these financial years was for a first-time home worth less than Rs 40 lakh. You can only get this if your loan amount at this time is less than Rs 25 lakh. The loan must be approved between April 1st and March 31st, 2014. The total deduction allowed under this clause is limited to Rs 1 lakh for the fiscal years 2013-14 and 2014-15.

Sections 80EE and 24 of the Income tax Act

Be quick to claim benefits if you meet the requirements of both Section 24 and Section 80EE of the Income Tax Act.

- First, use up your Rs. 2 lakh deductible limit under Section 24.

- Then seek the additional benefits under section 80EE.

- As a result, this deduction is in addition to the Rs 2 lakh limit set under section 24.

Sections 80EE and 80EEA of the Income tax Act

In the 2019 Union Budget, a new section 80EEA was added to prolong the tax benefits of interest deduction up to Rs 1,50,000 for housing loans obtained for affordable housing between April 1, 2019 and March 31, 2020. The individual taxpayer must be a first-time home buyer and not be eligible for the deduction under Section 80EE.

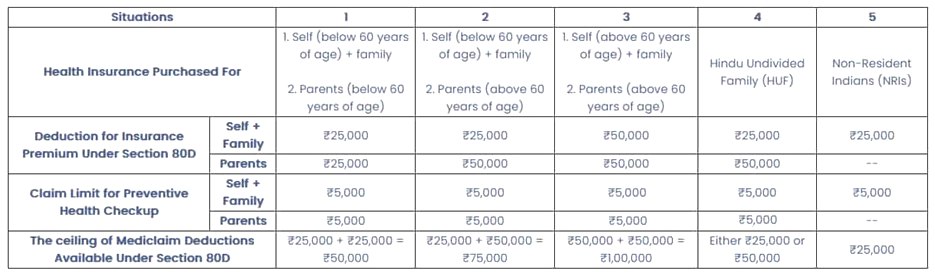

Medical Insurance (Section 80D). – Medical insurance premium deduction paid

You (as a person or a HUF) can deduct Rs.25,000 for insurance for yourself, your spouse, and your dependant children under section 80D. If your parents are under 60 years old, you can get an additional deduction for their insurance up to Rs 25,000. If the parents are over the age of 60, the deduction amount is Rs 50,000, up from Rs 30,000 in Budget 2018. If both the taxpayer and the parent(s) are 60 or older, the maximum deduction available under this section is Rs.1 lakh.

Disabled Dependent (Section 80DD): Deduction for Handicapped Dependent Relative Rehabilitation

A resident individual or a HUF can take advantage of the Section 80DD deduction, which is available on.

- Medical expenses (including nursing care), training, and rehabilitation of a disabled dependent relative.

- Payment or deposit to the specific disability-related maintenance scheme.

- When disability stands at or above 40 percent but is less than 80 percent – Rs 75,000 fixed deduction.

- If serious invalidity exists (disability amounts to 80% or more) – fixed Rs 1,25,000 deduction.

A certificate of disability from a prescribed medical authority is required in order to claim this deduction. The deduction limit of Rs 50,000 has been increased from the FY 2015-16 to Rs 75,000 and Rs 1,00,000 to Rs 1,25,000.

Section 80DDB – Medical Expenditure: Self or dependent medical expenses deduction

Individuals and HUFs under the age of 60.

A resident individual or a HUF can claim a deduction of up to Rs.40,000. It is available for any expenses incurred in connection with the treatment of specified medical diseases or ailments for himself or any of his dependents. For a HUF, such a deduction is available for medical expenses incurred for any of the HUF members suffering from these prescribed ailments.

For senior citizens and super seniors.

If the person on whose behalf the expenses are incurred is a senior citizen, the individual or HUF taxpayer can claim a deduction of up to Rs 1 lakh. The claim for a senior citizen and super senior citizen until FY 2017-18 was respectively Rs 60,000 and Rs 80,000. Unlike before, all elderly citizens (including super senior citizens) are now eligible for a deduction of up to Rs 1 lakh.

For the purpose of reimbursement claims.

Any reimbursement of the insurer or employer’s medical expenses shall be reduced from the taxpayer’s allowance of a deduction in this section.

Remember that in order to claim such a deduction, you must obtain a prescription for such medical treatment from the concerned doctor. Read more about Section 80DDB in our in-depth article.

Section 80U – Physical Disability: Deduction for people with physical disabilities

A resident suffering physical disability (including blindness) or a mental retardation is subject to a deduction of Rs.75,000. For serious disabilities, a deduction of Rs 1,25,000 may be claimed.

The deduction limits of Rs 50,000 were raised to Rs 75,000 from FY 2015-16 – Rs 1,00,000 were raised to Rs 1,25,000 from section 80U.

Section 80G – Donations: Deduction on Social Causes donations:

The diverse gifts specified in u/s 80G are deductible by up to 100% or 50% with or without limit. Until financial year 2017-18, a senior citizen and a super senior citizen could claim a deduction of Rs 60,000 and Rs 80,000, respectively. Unlike before, all elderly citizens (including super senior citizens) are now eligible for a deduction of up to Rs 1 lakh.

Section 80U – Physical Disability: Deduction for people with physical disabilities

A resident suffering physical disability (including blindness) or a mental retardation is subject to a deduction of Rs.75,000. For serious disabilities, a deduction of Rs 1,25,000 may be claimed.

The deduction limits of Rs 50,000 were raised to Rs 75,000 from FY 2015-16 – Rs 1,00,000 were raised to Rs 1,25,000 from section 80U.

Section 80G – Donations: Deduction on Social Causes donations

The diverse gifts specified in u/s 80G are deductible by up to 100% or 50% with or without limit.

From the financial year 2017-18, any cash donations exceeding Rs 2,000 will not be allowed as a deduction. To qualify for the 80G deduction, donations over Rs 2000 must be made in a form other than cash.

Donations with a full tax deduction and no qualifying limit.

- The Central Government established the National Defense Fund.

- Prime Minister’s National Relief Fund.

- National Foundation for Communal Harmony.

- A university/educational institution of national renown that has been approved.

- In any district, a Zila Saksharta Samiti is formed under the chairmanship of the Collector.

- A fund established by a state government to provide medical assistance to the poor is known as the National Illness Assistance Fund.

- National Board of Blood Transfusion or any State Board of Blood Transfusion.

- National Autism, Cerebral Paralysis, Mental Delays and Multiple Disabilities Trust.

- National Sports Fund.

- National cultural fund.

- Development and Application Technology Fund.

- National Fund for Children.

- The Relief Fund for Chief Ministers or the Relief Fund for Lieutenant Governors for every State or territory of the Union.

- The Armed Forces Central Welfare Fund, the Indian Naval Benevolent Fund or the Cyclone Relief Fund of the Air Force, Andhra Pradesh, 1996. 1996.

- During October 1, 1993 and October 6, 1993, Maharashtra Chief Minister’s Relief Fund.

- Maharashtra’s Chief Minister’s Earthquake Relief Fund

- Any fund established by the Gujarat State Government solely for the purpose of providing relief to earthquake victims in Gujarat.

- Section 80G(5C) applies to any trust, organisation, or fund that provides help to Gujarat earthquake victims (contribution made during January 26, 2001 and September 30, 2001).

- Armenia Earthquake Relief Fund established by Prime Minister

- Fund for Africa (Indian Public Contributions).

- Swachh Bharat Abhiyan ( Was implemented from financial year 2014-15).

- Clean Ganga Fund is a non-profit organisation dedicated to keeping the (applicable from financial year 2014-15)

- National Institute on Drug Abuse’ (applicable from financial year 2015-16).

Donations that are eligible for a 50% deduction without any restrictions.

- The Jawaharlal Nehru Memorial Fund was established in memory of Jawaharlal Nehru.

- Prime Minister’s Drought Relief Fund.

- The Indira Gandhi Memorial Trust.

- The Rajiv Gandhi Foundation.

Donations to the following organisations are tax deductible at 100% up to 10% of adjusted gross total income.

- To be used for the purpose of encouraging family planning by the government or any approved local authority, institution, or group.

- Donation by a company to the Indian Olympic Association or any other notified association or institution created in India for the development of sports and games infrastructure or for the sponsorship of sports and games in India.

Donations to the following organisations are qualified for a 50% deduction up to 10% of adjusted gross total income.

- Any other fund or institution that meets the requirements of Section 80G. (5).

- Any charitable purpose other than promoting family planning to be used by the government or any local authority.

- Any Indian authority established for the aim of dealing with and meeting the demand for housing, or for the planning, development, or enhancement of cities, towns, or villages, or both.

- Any corporation referred to in Section 10(26BB) for the purpose of advancing minority community interests.

- Repairs or renovations to any notified temple, mosque, gurudwara, church, or other location.

Section 80GGB: Company Contribution : Deduction for corporate contributions to political parties

Section 80GGB allows an Indian company to deduct the amount it contributes to any political party or electoral trust. Contributions made in any form other than cash are eligible for a tax deduction.

Section 80GGC: Contribution to Political Parties : Deduction for contributions made to political parties by anyone.

Individual taxpayers can deduct any amount they provide to a political party or electoral trust under section 80GGC. Companies, municipal governments, and artificial juridical persons who are entirely or partially supported by the government are not eligible. Only when you pay other than cash can this deduction be used.

Patent Royalty (Section 80RRB): Deduction for any income received as a result of a patent royalty

80RRB any royalty income received on or after April 1, 2003, under the Patents Act 1970, is eligible for a deduction of up to Rs.3 lakh or the income received, whichever is less. The taxpayer must be a single patentee who is also an Indian resident. A certificate in the required form, duly signed by the prescribed authority, must be provided by the taxpayer.

Section 80TTB – Interest Income

Interest on deposits for senior citizens is deductible.

In Budget 2018, a new section 80TTB was introduced, allowing deductions for interest income from deposits held by senior citizens. The deduction is limited to Rs.50,000.

There will be no further deductions under section 80TTA. Along with Section 80 TTB, Section 194A of the Act will be amended to raise the TDS threshold limit on interest income payable to senior citizens. The previous limit was Rs 10,000, which was increased to Rs 50,000 in the most recent Budget.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.