How to choose an accounting method ?

Table of Contents

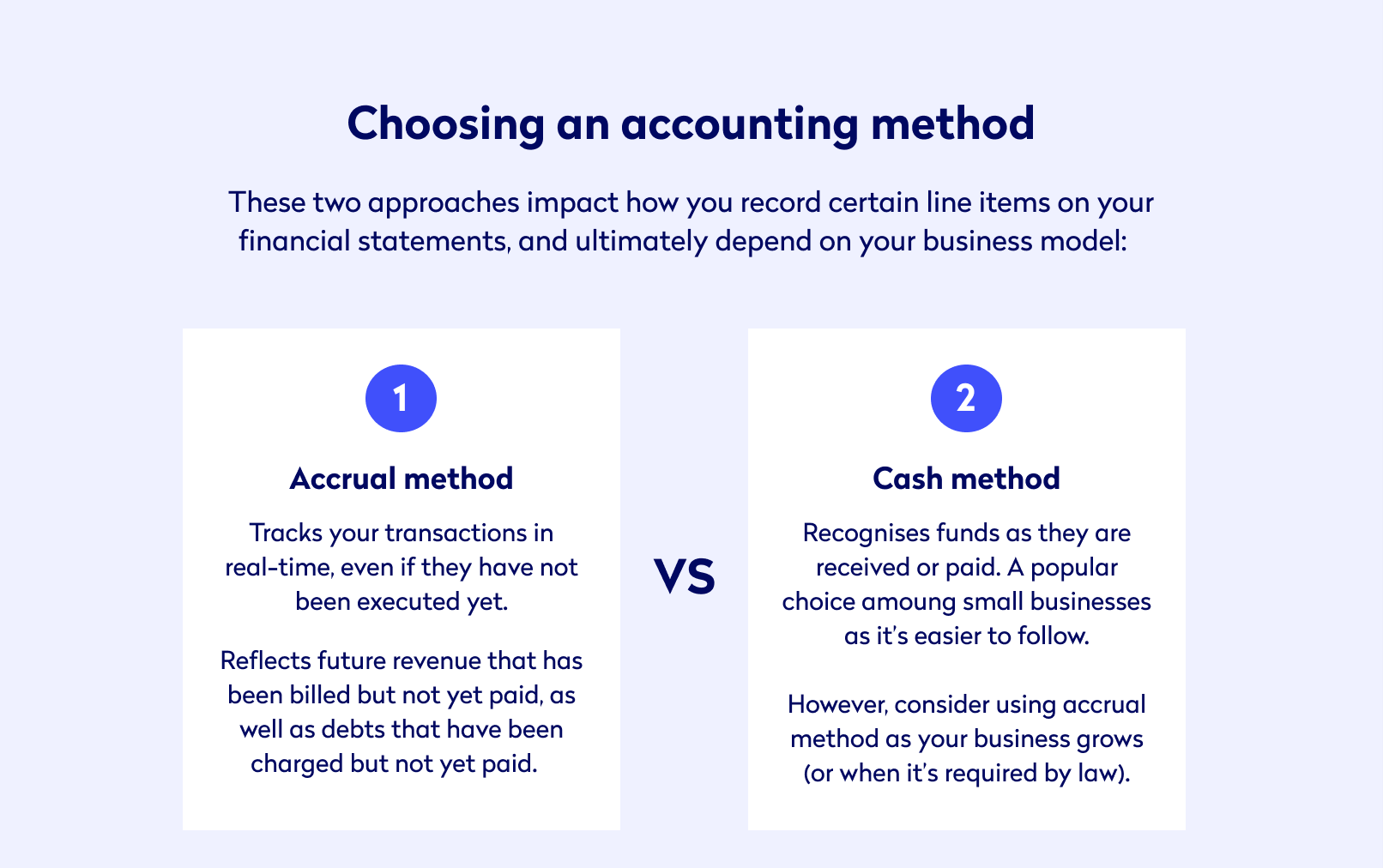

How to choose an accounting method ?

- Using the cash basis of accounting method may appear to lower your tax liability. However, it is probable that it will merely postpone your tax payment However, you will not be able to save any money on taxes

- Once you’ve opted on an accounting method, you must follow it on a regular basis. If your goal is to save or avoid taxes, you are not allowed to change your accounting system frequently.

- Unless your receipts are irregular, imprecise, or unpredictable, it appears more sensible to use the Accrual Basis. The Income Tax Act states that books of accounts must be maintained for the purposes of income taxation. Section 44AA and Rule 6F have made these mandatory.

Accrual Basis of Accounting (also called Mercantile Basis)

| Accrual Basis of Accounting | Cash Basis of Accounting |

| When a right to receive arises, income is accounted for or recorded. | When income, is received it is recorded. |

| When a payment obligation occurs, expenses are accounted for or booked. | Expenses are recorded when they are paid. |

| When income is booked, tax is due; nevertheless, tax may be due even if income has not been received. | Tax liability occurs in the year in which income is received, obliging you to pay tax only when income is obtained. |

| This method can be used for all types of income, however it is required for salary, house property, and capital gains. | Only profits and losses from a business or profession, as well as income from other sources, are allowed to be calculated using this method. |

| Example 1: You issue your client an invoice for a transaction on February 2nd, but you don’t be paid until April 4th. Based on the date the invoice was sent to the client, the revenue will be recorded in your account. | Example 1: When the payment is received, revenue will be accounted for on April 4th (which will be the tax year after the year in which the invoice was raised or work was performed) |

| Example 2: Your cellphone bill from February 15th to March 15th has arrived. For accounting purposes, this bill will be recorded as an expense in March.

This applies regardless of whether you pay by the 31st of March or not (you may actually pay in the next tax year). When your books of accounts are closed on March 31st for tax purposes, the mobile bill for the remaining 15 days of March will be incurred using a reasonable basis, based on an estimate. |

Example 2: Your cell bill from the 15th of February to the 15th of March has arrived, and if you pay it before the 31st of March, it will be recorded as an expense in the month of March (therefore, gets booked in the same tax year).

If you pay it in April, it will be recorded as an expense in the following tax year (though the expense or mobile usage pertains to the previous tax year). |

It’s important to remember that the accounting method you chose must be followed for all clients, all revenues, and all expenditure.

Total taxable income and tax payable

- Making full use of Section 80 deductions can help you save money on taxes. Section 80C of the Income Tax Act encourages taxpayers to save for the future by providing tax relief on specified expenditure (by giving deductions on investments in financial products).

- Net Taxable Income = Gross Taxable Income – Deductions

- By claiming a deduction for the amount actually invested/spent under this clause, you can lower your taxable income by up to Rs.1.5 lakh. If you are under the age of 60 and have a net taxable income of more than Rs.2.5 lakh, you must pay income tax.

Here is how tax will be calculated on your income:

Tax payable for a freelancer

How to calculate advance tax?

- Calculate your overall income by adding up all of your receipts.

- Subtract only the expenses that are directly relevant to your job.

- Include earnings from other sources, such as a rental property or a savings account.

- Determine your tax slab and compute your tax liability.

Remember to deduct TDS

- If your tax payment exceeds Rs.10,000, you must pay advance tax by the deadlines listed below.

Due date for Advance Tax

| On or before 15th June | Not less than 15% of advance tax |

| On or before 15th September | Not less than 45% of advance tax as reduced by the tax paid in the last installment. |

| On or before 15th December | Not less than 75% of advance tax as reduced by the tax paid till the last installments. |

| On or before 15th March | The whole amount (100%) of advance tax as reduced by the tax paid till the last installments. |

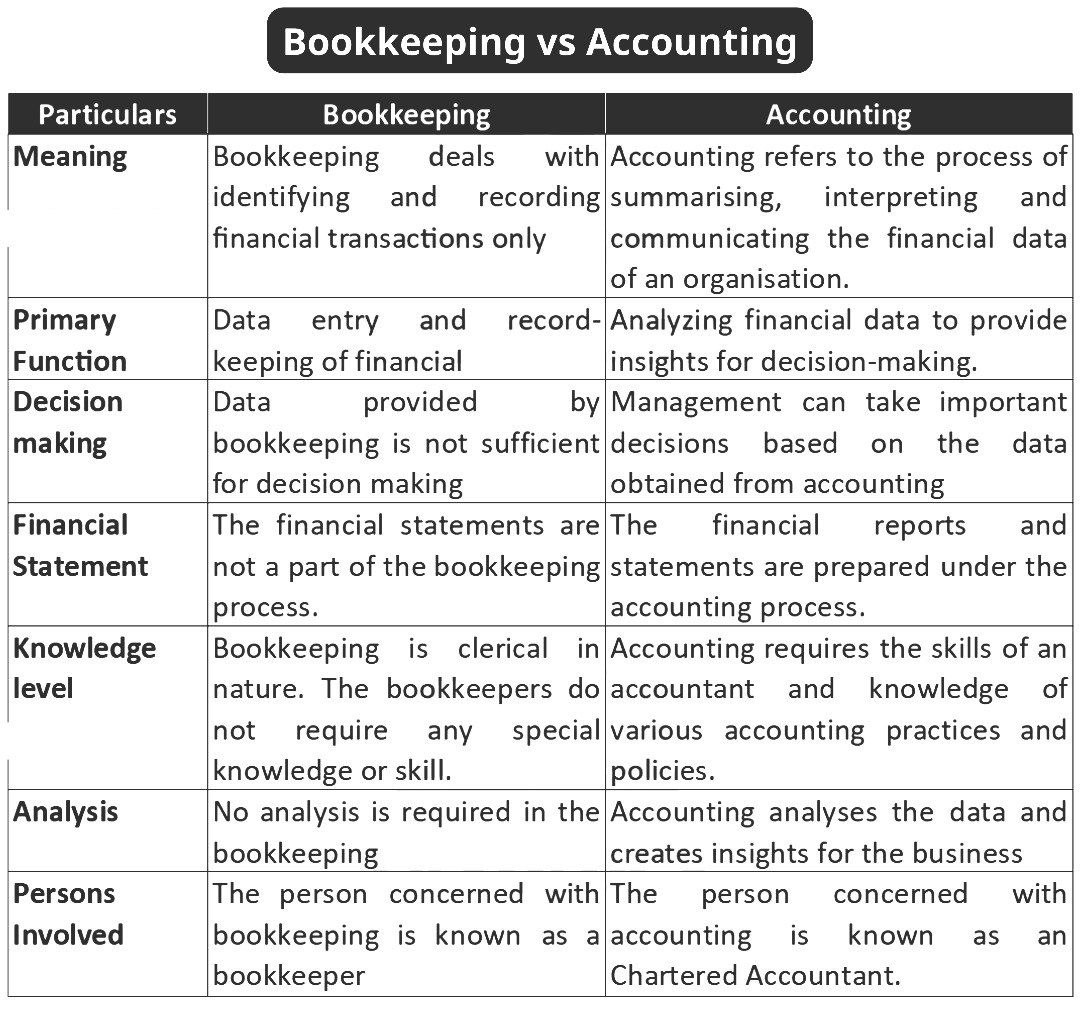

Difference between accounting and bookkeeping

India Financial consultancy corporation Pvt Ltd specialize in:

• Accounting

• Bookkeeping

• Payroll

• Management Accounts

• Accounts Receivable / Accounts Payable

• Financial Modeling /Financial Reporting / Financial Statement

• Taxation

• Strategic CFO Support

• Compliance & Reporting

By partnering with India Financial consultancy corporation Pvt Ltd. Services, you can expect:

-

Expertise and Experience:

Our dedicated team brings extensive knowledge and experience in accounting and bookkeeping services. We stay updated with industry best practices to provide you with top-quality solutions.

-

Tailored Solutions:

We understand that every organization is unique, and we customize our services to meet your specific requirements. We work closely with you to ensure our solutions align with your business objectives.

-

Data Security and Confidentiality:

We prioritize the security and confidentiality of your financial data. Our robust data protection measures and strict adherence to privacy regulations guarantee the safety of your sensitive information.

-

Cost Savings and Efficiency:

Outsourcing your accounting and bookkeeping needs to us allows you to reduce overhead costs associated with hiring and training in-house staff. Our streamlined processes and technology-driven solutions enhance efficiency and productivity. We would be delighted to discuss the possibilities of establishing with your company to fulfill accounting and bookkeeping requirements. Let’s set up a time to chat or call for further steps if this is something you are looking for!!

Popular blogs :

- F&Q on NRI Income Tax Compliance (Help Centre)

- Key Provision for NRI Taxation

- Tax implication for NRI on selling property

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.