GST Registration is getting suspended due to non-compliance

Table of Contents

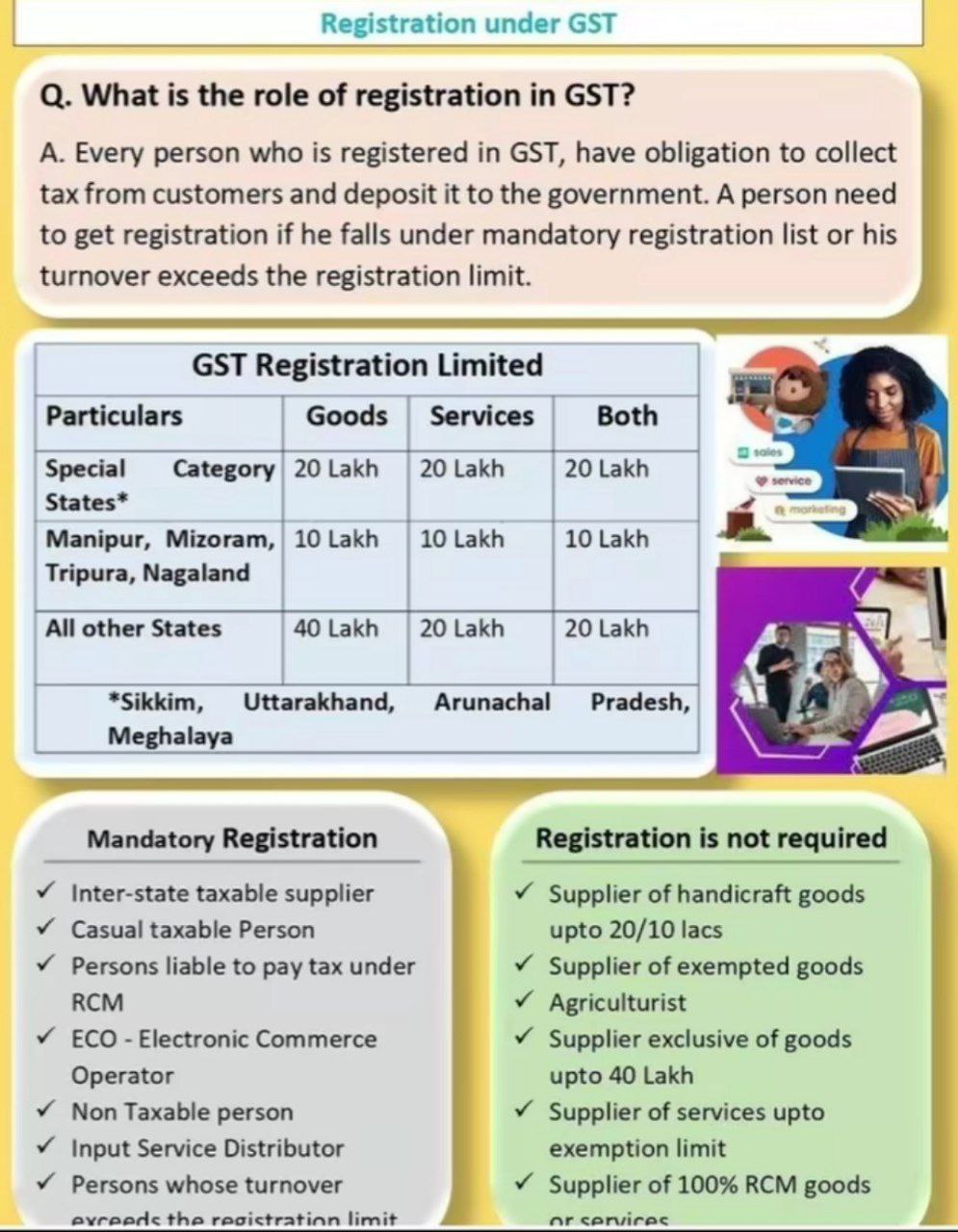

GST Registration under GST LAW

GST Registration is getting suspended due to non-compliance – GST Important Provision

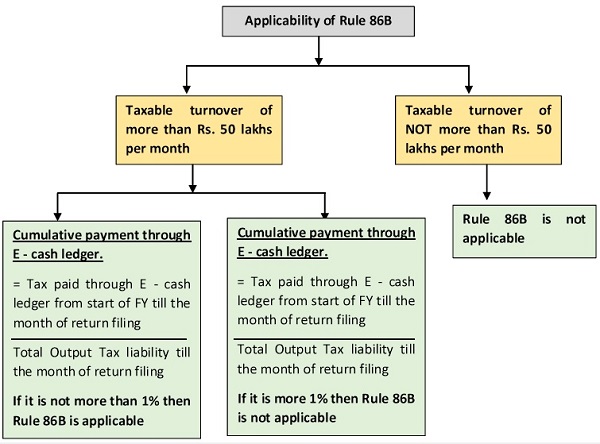

- As per the notification, GST registered individuals would be unable to pay more than 99% of their production tax obligations from the funds in their electronic credit ledger as of Jan 1st, 2021. In other words, as per the rule 86b example above, GST taxpayers cannot claim input tax credit for more than 99% of the output tax liability.

- What is an electronic credit ledger: The amount of funds that is available for the payment of tax debt is shown in the electronic cash ledger. While Electronic Liability Ledger displays the taxpayer’s GST Tax liability. The balance that remains of the registered taxpayer’s applicable input tax credit is shown on the electronic credit ledger.

- Rule 86B imposes restrictions regarding how an input tax credit (ITC) from the electronic credit ledger can be used to reduce the output tax liability. This regulation overrides all previous CGST regulations. This GST Restriction does not apply in different cases: you may refer First Proviso to the GST Rule 86B

GST Restrictions on use of amount available in electronic credit ledger (GST Rule 86B)

- Notwithstanding anything contained in these rules,

- GST registered person shall not use the amount available in electronic credit ledger to discharge his liability

- Towards output tax

- In excess of 99% of such GST tax liability,

- In cases where the value of taxable supply

- Other than exempt supply & zero-rated supply,

- In a month

- more than INR. 50,00,000/-

Exceptions of Rule 86B

Rule 86B of the GST has few Exceptions which is mention here under :

- Following people have paid more than INR 1,00,000 as income tax in each of the last 2 Fy, for which time limit to file the ITR u/s 139(1) has expired:

- Goods and Services Tax registered person or

- Any of Partners, Members of Managing Committee of Associations or Board of Trustees, whole-time Directors of GST registered person. or

- Karta or Proprietor, or Managing Director of the Goods and Services Tax registered person

- Goods and Services Tax registered person has received a Goods and Services Tax refund of more than Rs. 1 Lakhs in preceding fy on a/c of unutilised ITC or export under letter of undertaking or due to the inverted tax structure.

- Goods and Services Tax registered person has discharged his/her liability towards output tax through the electronic cash ledger for an amount which is more than 1% of the total output tax liability.

- Goods and Services Tax registered person is a:

- Local authority; or

- Government Department; or

- Statutory body. or

- Public Sector Undertaking

Note: The officer authorized by the commissioner or Commissioner can remove the Goods and Services Tax restrictions mentioned above after undertaking need verifications & safeguards

Summary Overview of When GST Registration: Know Your Triggers

Thresholds for GST Registration

- Goods: INR 40 lakh

- Services: INR 20 lakh

- (Lower thresholds apply for special category states)

Compulsory GST Registration (As per Section 24 of CGST Act)

GST registration is mandatory regardless of turnover if:

- You make inter-state supply of goods

- You’re under Reverse Charge Mechanism (RCM)

- You’re a casual taxable person (temporary business in a state)

- GST Registration for Online Sellers

- For goods, selling via e-commerce (e.g., Amazon, Flipkart) → Registration required from Day 1

- For services (e.g., tutors, beauticians):

Exempt from GST if:

-

- Turnover < INR 20 lakh

- No inter-state supply

- Not using e-commerce platforms

How to Register under GST

- Visit www.gst.gov.in

- Fill GST REG-01:

- Part A: PAN, email, mobile → generates ARN

- Part B: Business details + documents

Timeframe for GST Registration

- Standard: Within 7 working days

- With checks: Up to 30 days

GST Return Filing & GST Payment

- GSTR-1 (Sales Data): Due by 11th of every month

- GSTR-3B (Tax Payment): Due by 20th of every month

- (Small businesses ≤ INR 5 Cr turnover may opt for quarterly filing)

Composition Scheme (Optional)

Flat tax rate for small taxpayers:

- Goods: Max turnover INR 1.5 crore → Tax @ 1%

- Services: Max turnover INR 50 lakh → Tax @ 6%

- (₹75 lakh limit for NE & HP states)

- Note: Not available if you:

- Make inter-state supplies

- Sell via e-commerce platforms

Penalties on violation of rule 86B

- GST Registration taxpayer shall be liable to pay a penalty of minimum penalty ₹ 10,000/- and maximum penalty equal to the tax evaded, whichever is higher. It is one time penalty for one offence.

GST Penalties

- Interest: 18% p.a. on delayed tax

- Late Fee: INR 200/day (Max ₹10,000)

GST Registration Document Requirements Summary :

As per GSTN Instruction No. 03/2025-GST following guidance is issuec on GST Registration Document Requirements:

- Owned Premises; Any ONE of the following: Property Tax Receipt, Municipal Khata, Electricity bill/Water Bill, Any similar document under State laws

- Rented Premises – Registered Rent Agreement- Registered Rent Agreement, Any ONE proof of lessor (e.g., Property Tax Receipt / Electricity Bill)

- In case Rented Premises – Unregistered Rent Agreement – Unregistered Rent Agreement, Any ONE ownership proof of lessor, Lessor’s ID Proof

- Utility Bill in Applicant’s Name (Electricity/Water) : Utility Bill in applicant’s name, Rent Agreement, No lessor documents required

- Premises Owned by Spouse/Relative: Consent Letter (plain paper), Owner’s ID Proof, Any ONE ownership proof

- Shared Premises – Registered Rent Agreement- Registered Rent Agreement, Any ONE ownership proof of lessor

- In case Shared Premises – Unregistered Rent Agreement – Unregistered Rent Agreement, Any ONE ownership proof of lessor, Lessor’s ID Proof

- Shared Premises – No Agreement, Consent Letter from ownerOwner’s ID ProofAny ONE ownership proof

- Rented/Leased without Agreement : Affidavit on non-judicial stamp paper (before Magistrate/Notary) and Utility Bill in applicant’s name

- SEZ Units : SEZ Certificate or Letter issued by Government of India

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.