Income tax treatment of a company’s dividend:

Table of Contents

Income tax treatment of a company’s dividend:

If a shareholder receives a dividend from a domestic company, he is not required to pay any tax on that dividend until Assessment Year 2020-21 because it is exempt from tax under Section 10(34) of the Act. In such cases, however, the domestic company is required to pay a Dividend Distribution Tax (DDT) under section 115-O.

As a result, if the dividend is distributed on or after 01-04-2020, the provisions of Section 115-O will not apply. As a result, if the dividend is distributed on or after January 4, 2020, domestic corporations will not be required to pay DDT, and shareholders would be required to pay tax on the dividend income. Because dividends are now available at a price of the shareholder, several elements of the Act have been resurrected, including the ability to deduct expenses from dividend income, the deductibility of tax from dividend income, and the treatment of inter-corporate dividends, among others.

This section will teach you about the taxability of dividends distributed by domestic corporations on or after January 4, 2020.

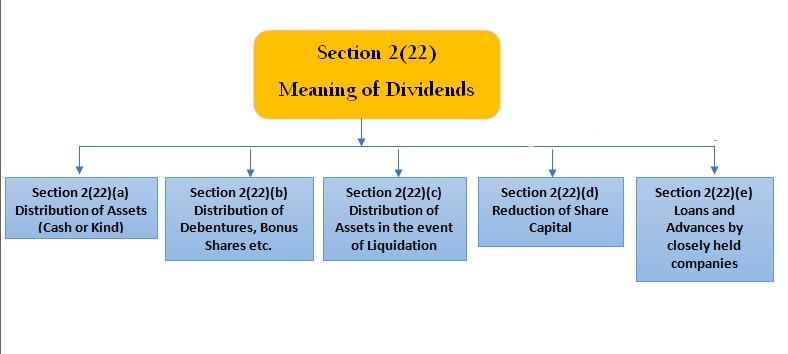

Under the Income Tax Act, the term “dividend” has a specific meaning.

A dividend is typically defined as a company’s distribution of profits to its shareholders. However, in accordance with Section 2(22) of the Income-tax Act, the dividend must include the following.

- Distribution of accumulated profits to shareholders, which requires the release of the company’s assets.

- Distribution of debentures or deposit certificates to shareholders from the company’s accumulated profits, as well as the issuance of bonus shares to preference shareholders from the company’s accumulated profits.

- A distribution made to the company’s shareholders upon its liquidation from its accumulated profits.

- Distribution to shareholders of accumulated profits from the company’s capital reduction.

- A loan or advance made to a shareholder by a closely held company from its accumulated profits.

Taxability on or after 01-04-2020 of the dividend received:

The taxability of dividends in the hands of the company as well as shareholders would be as follows beginning with Assessment Year 2021-22.

Domestic companies’ obligation:

- On or after 01-04-2020, domestic companies are not required to pay DDT on dividends distributed to shareholders. Domestic corporations, on the other hand, must deduct tax under Section 194.

- According to Section 194, which applies to dividends distributed, declared, or paid on or after 01-04-2020, an Indian company must deduct tax at a rate of 10% from dividends distributed to resident shareholders if the total amount of dividend distributed or paid to a shareholder during the fiscal year exceeds Rs. 5,000. However, no tax would be deducted from any dividend paid or due to the Life Insurance Corporation of India (LIC), the General Insurance Corporation of India (GIC), or any other insurer in respect of any shares in which it owns or has a full beneficial interest.However, in accordance with the relevant DTAA Taxability, the tax in the hands of the shareholders shall be deducted where the dividend is payable to the non-resident or to a foreign company.

Taxability in hands of shareholders:

- Application from assessment Year 2021-20 Section 10(34) provides for an exemption for shareholders from dividend income. The dividend received in the course of the 2020-21 financial year is therefore now taxable by the shareholders. As the whole amount of the dividend is taxable in the hands of the partner, therefore, Section 11 5BBDA providing for taxability of the dividend above Rs 10 lakh does not have any significance.

- The taxability of dividends and the rate at which they are taxed will be determined by a number of factors, including the shareholders’ residential status and the relevant head of income. In the case of a non-resident shareholder, the provisions of Double Taxation Avoidance Agreements (DTAAs) and Multilateral Instruments (MLIs) will also apply.

In the hands of a resident shareholder, the dividend is taxable.

- A person can trade or invest in securities. The income he receives from his trading activity is taxable as business income. Thus, the dividend revenues shall be taxable under the head business or occupation, where shares are held for trading purposes. While the income in kind of the dividend is held as an investment, the income generated by the heads of other sources shall be taxable.

- The revenue is calculated by the accounting method regularly followed by the assessor, which is taxable under head PGBP. A taxpayer may follow either a mercantile accounting system or an accounts’ cash basis for the purposes of the calculation of business revenue. But the accounting approach used by the assessee does not affect the basis for the dividend income charge as Article 8 of the Law stipulates that in the year it is declared, distributed or paid by a company a final dividend, including a deemed dividend, is taxable. In the previous year, however, the provisional dividend is taxable in which the amount of that dividend is made available to the shareholder unconditionally by the Company. In other words, the provisional dividend is taxable on the basis of receipt.

Income dividend deductions:

- If a business earnings dividend is taxable, the assessee can claim the deduction for the dividend’s earnings, such as collection fees, interest on loans, and others.

- However, if the dividend is taxable under the other sources category, the assessee can deduct only the interest expense incurred to earn the dividend income up to 20% of the total dividend income. Any other expenses including commission or remuneration payable to a banker or any other person to make such a dividend shall not be deducted.

Dividend income tax rate:

- Divide income shall be charged at a normal rate as a tax in the case of an assessee with the exception of the Dividend Income, which applied to the GDRs issued by such a company under an Employees Stock Option Scheme, being an employeen of the Indian enterprise or its affiliate engaged in the information technology, entertainment, pharmaceutical or bio-technology industry. In that case the dividend shall, without deduction under the Income Tax Act, be taxed at a concessional tax rate of 10%. However, in foreign currency, the GDR should be bought by the employee.

Taxation of non-resident shareholders, including FPIs:

- A non-resident generally invests in India either directly as a private equity investor or indirectly as a Foreign Portfolio Investor (FPIs). A non-resident individual may also be a promoter of an Indian company. A non-resident person normally holds shares of an Indian firm as an investment and, as a result, any dividend income is taxed under the head other sources, unless the income is related to the non-Permanent resident’s Establishment in India. Securities held by foreign portfolio investors (FPIs) are always recognized as capital assets, not stock-in-trade.

- So also in the case of FPIs, the income from the dividend under the other sources is always taxable.

Dividend Income tax rate:

- Dividend income is taxable at 20 per cent in the hands of a non-resident (including FPIs and NRIs) without providence for a deduction under any provision of the Income Tax Act. •Dvidend income is taxable at a rate of 20 per cent. But the dividend income of an Offshore Banking Unit investment division is taxable at the rate of 10%.

- Moreover, if a dividend is received in connection with the GDRs of a foreign currency bought by an Indian or Public Sector Company (PSU), the rate of tax shall be 10% without any deduction.

| Section | Assessee | Particulars | Tax Rate |

| Section 115AC |

Non-resident | Dividend on GDRs of an Indian Company or Public Sector Company (PSU) purchased in foreign currency | 10% |

| Section 115AD |

FPI | Dividend income from securities (other than units referred to in section 115AB) | 20% |

| Investment division of an offshore banking unit | Dividend income from securities (other than units referred to in section 115AB) | 10% | |

| Section 115E | Non-resident Indian |

Dividend income from shares of an Indian company purchased in foreign currency. | 20% |

| Section 115A |

Non-resident or foreign co. | Dividend income in any other case | 20% |

Withholding tax:

- In the case of a dividend paid to a non-resident shareholder, the tax must be deducted under section 195 of the Income Tax Act. However, where the dividend is issued or paid in respect of GDRs of an Indian Company or a Public Sector Undertaking (PSU) purchased in foreign currency or to Foreign Portfolio Investors (FPIs), the tax must be deducted in accordance with sections 196C and 196D, respectively.

- The withholding tax rate on dividends, according to section 195, shall be as specified in the relevant year’s Finance Act or under the DTAA, whichever is appropriate in the instance of an assessee. The withholding tax rates under sections 196C and 196D, on the other hand, are 10% and 20%, respectively.

- The dividend withholding tax rate distributed or paid by a non-resident shareholder may be explained using the table below.

| Section

(chargeability of income) |

Section

(withholding of tax) |

Nature of Income

|

Rate of TDS

(Payee is any other non- |

Rate of TDS

(Payee is a foreign |

| Section 115AC |

Section 196C

|

Dividend on GDRs of an Indian Company or Public Sector Company (PSU) purchased in foreign currency | 10%

|

10%

|

| Section 115AD | Section 196D | Dividend income of FPIs from securities Investment division of an offshore banking unit | 20% 10% | 20% 10% |

| Section 115E | Section 195 | Dividend income of non-resident Indian from shares of an Indian company purchased in foreign currency. | 20%* | – |

| Section 115A | Section 195 | Dividend income of a non-resident in any other case

|

30%* | 40%* |

* Where a tax withholding rate in accordance with the DTAA is lower than the Finance Act rate, tax is deducted in accordance with the DTAA rate.

Under DTAA taxability:

- The dividend earnings are generally taxable in the source country as well as in the assessee’s country of residence, thereby providing the assessee’s tax credit in the country of origin. In Indian, therefore, the revenues of the dividend are taxable as provided by the Act or by the DTAA, whichever is more profitable.

- Dividends are taxable in the source nation in the hands of the beneficial owner of shares at a rate ranging from 5% to 15% of the gross amount of the dividends, according to the majority of the DTAAs India has signed with other countries.

- Dividend tax rates are further reduced under the DTAA with countries like Canada, Denmark, and Singapore when the dividend is paid to a firm that owns a particular percentage (usually 25%) of the company generating the dividend. However, there is no minimum time restriction under these DTAAs for which the receiving firm must keep such an ownership. As a result, MNCs were frequently detected abusing the laws by raising their stock in the company just before the dividend was declared and dumping it after receiving the payout. In India, dividend income is tax-free in the hands of shareholders; hence this circumstance does not exist. However, following the proposed revision, India will face the risk of foreign companies avoiding taxes by artificially expanding their holdings in dividend-paying domestic companies.

- India is a signatory towards the Multilateral Convention (MLI), which requires it to put in place the OECD-recommended measures to prevent base erosion and profit shifting. MLI is a binding international legal instrument that is being developed in order to quickly implement the OECD-recommended measures to prevent Base Erosion and Profit Shifting in existing bilateral tax treaties. For dividend income the minimum period of time in which a shareholder receiving dividend income must retain their shareholding in the company paying the dividend is set by Article 8 (Dividend Transfer Transaction) of MLI, which allows the benefit of the reduced dividend tax rate.

Inter-corporate dividend:

- Because the taxability of dividends is being proposed to be shifted from companies to shareholders, the Government has added a new section 80M to the Act to eliminate the cascading effect when a domestic company receives a dividend from another domestic company. However, nothing prohibits a local corporation from receiving a dividend from a foreign company and distributing it to its shareholders. In such cases, the taxability is as follows.

Domestic co. receives dividend from another domestic co.:

- Section 80M eliminates the cascading impact by requiring that an inter-corporate dividend be deducted from the total income of the firm receiving the dividend if it is delivered to shareholders 1 month just before return’s due date.

Domestic co. receives dividend from a foreign co.

- Dividends received from a foreign corporation by a domestic corporation in which that company has 26% or more of its equity shares are taxable at a rate of 15% plus supplements and cessation of health and education in accordance with Section 1 15BBD. Such tax shall be computed on a gross basis, with no allowance for expenditure deductions.

- Dividend from a foreign company in which that domestic company holds less than 26%, by a domestic company, is taxable at a normal tax rate. For the purposes of earning this dividend income, the domestic company can claim a deduction for any expenses it incurred.

No MAT on a foreign company’s dividend revenue.

- MAT provisions apply to a foreign company only if it is a resident of a country with which India has DTAA and conducts business through a PE in India. Under Section 44B, Section 44BB, Section 44BB, Section 44BBA or section44BBB, however, it should not be taxable. Once the foreign company is found to be responsible for paying MAT, it will make certain adjustments in its profits.

- However, if it is credited (or debited) into the profit and loss account, the following revenue (and costs claimed in relation thereto), if it is taxable at a rate less than MAT rate is added back to (or cut off) the net profit.

- Capital gain from securities;

- Interest;

- Royalty;

- FTS

Thus, a foreign company is not liable to pay MAT on the aforesaid incomes.

- Regarding the taxability of dividends in the hands of a foreign company, section 1 15JB of the Finance Bill, 2021 has been amended to provide that dividend income and expenses claimed in respect thereof be added back or reduced from net profit if such income is taxed at a rate lower than the MAT rate due to the DTAA.

- It should be noted that dividend income in the hands of a foreign company is taxable in accordance with the provisions of the Act or relevant DTAA, whichever is more advantageous.

Dividend income advance tax liability:

If the deficiency in the advance tax payment or failure to pay it on time is due to dividend income, no interest will be levied under section 234C if the assessee had also paid that amount of tax in successive advance tax instalments. However, in respect of the deemed dividend as set out in Section 2(22) this benefit cannot be provided (e).

Conclusion on Tax Treatment of Dividend Income:

- Since the Dividend Distribution Tax was repealed by the Finance Act of 2020, dividends paid by corporations on or after April 1, 2020 are now taxable incomes to the investor.

- Section 115BBDA of the Income Tax Act, which allows for the taxation of dividends in excess of Rs. 10 lakh, is no longer relevant because the full dividend amount is now taxable in the hands of the shareholders.

- Under Sections 194 and 195 of the Income Tax Act of 1961, an Indian company is required to deduct the applicable tax at source.

- The distribution of a Dividend on Equity Shares to a resident shareholder in excess of INR 5000 in a financial year is covered by Section 194.

- TDS at a rate of 10% will be deducted by the payer in the event of resident shareholders, and TDS at a rate of 20% will be deducted if the payee does not give the PAN.

- In the event of non-resident shareholders, the payer is required to deduct TDS at a rate of 20%.

Following the repeal of DDT, businesses may prefer to incorporate a corporation rather than a firm or LLP, but only if they can handle the additional compliance requirements that a corporation must meet.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.