intimations and Returns filling Compliance for NBFC’s

Table of Contents

Compliance by NBFC under RBI Regulation Different intimations & Returns

- One of the main factor in improving economic growth is arobust financial systems. NBFC has proven to be an important asset of Indian economy. In transportation and infrastructure sector as well NBFC has been a major contributor, it has also generated multiple employment opportunities & gained a remarkable in India.

- NBFC is able to procure an exceptional position in financial area. NBFC provide loans to weaker sections , and support those people where the bank doesn’t reach. NBFC has to comply with certain compliances that will the functioning of the NBFC smooth. This blog includes all the information regarding the returns and intimation that NBFC has to submit to RBI.

Reserve Bank of India Master Directions for NBFC

- RBI has issued the master direction non -banking financial company returns (Reserve Bank) direction, 2016 in September 2016, and for NBFCs with asset size of more than 500 crore and for NBFC which accepts a public deposit there is a different Master Direction. This is why, the direction does not apply to such NBFCs.

- As per the Reserve Bank of India Master Direction – NBFC – Non Systemically important Non-deposit taking company ( reserve bank) direction ,2016, it is essential for NBFC to submit several returns to RBI regarding the the deposit acceptance, ALM, Prudential norms compliance along with other other things.

RBI Master Direction Applicability & Exemptions on NBFC

- NBFC that has an asset size of less than Rs. 500 Cr & does not accept public deposit, is subject to fulfil the RBI compliances.

- Direction under chapter IV (prudential Regulation), paragraph 68 (KYC Directions) and chapter V ( FCP guidelines ) do not apply to those NBFCs who nether have any retrieved public funds nor have customer interface.

- The NBFC has access public funds but have no customer interface are exempted from the applicability of para 68 (KYC directions) and chapter V (FPC procedure) of the directions.

- NBFC that has customer interface but does not have access to public funds are exempted from the applicability of chapter VI (prudential Regulation) of the direction.

- RBI Master direction applies to NBFC – Factor, Micro finance Institution , infrastructure finance company having an asset size of less than INR 5000 Crore, and registered under the provision of RBI Act 1934.

- The provision of Master direction para 23 shall not apply to an NBFC being a govt Company. It has been given under the clause (45), section 2 of companies Act ,2013 and not holding or accepting public deposit.

With Reference To Public Funds: It refers to the funds financed Via bank finance , the Public , inter- corporate deposits, or via outside sources for Eg: debentures, commercial papers etc. It is to be noted that these funds do not include the funds raised through instruments that compulsorily change to Equity shares in period of 5 years from date of issue.

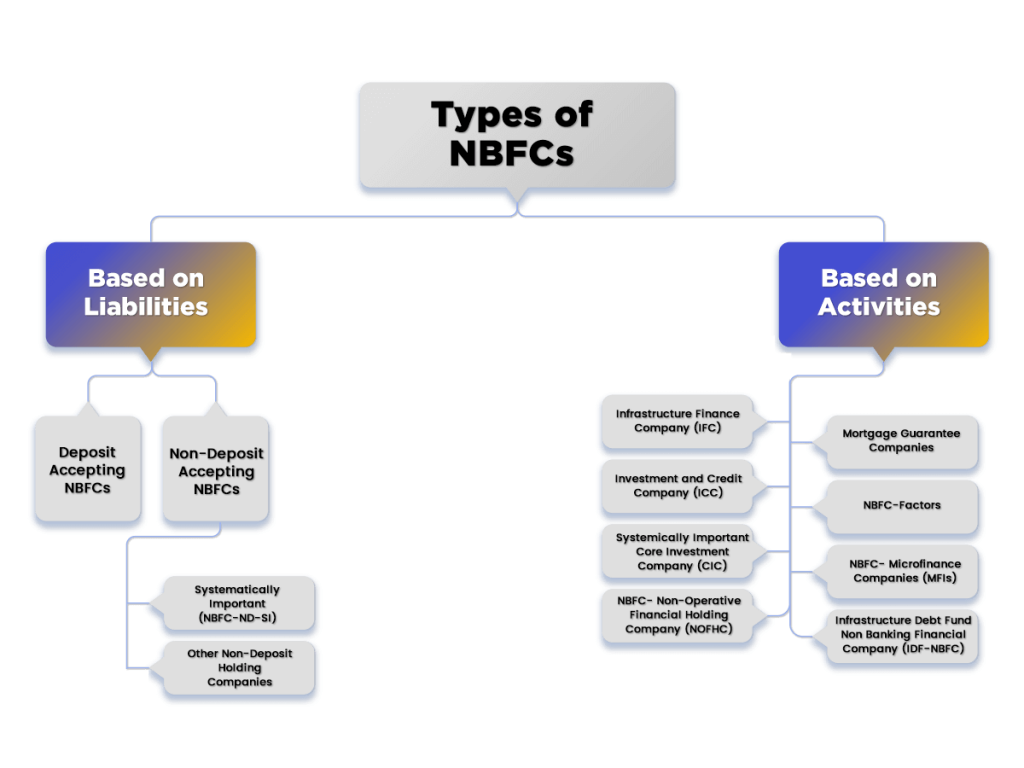

TYPE OF NBFCS CLASSIFIED ON THE BASIS OF THEIR ACTIVITIS

The Non-Banking Financial Companies can be divided into five categories

- Residual non-banking Companies i,e. RNBCs

- Non depository taking NBFCs i,e. NBFCs-ND

- Deposit taking NBFCs i.e NBFCs-D

- Systematically Important or NBFCs not holding/accepting public deposits and have asset size of INR 500 crore or more. i.e. NBFC-ND-SI

- Non- banking financial companies- Asset reconstruction companies. i.e NBFC-ARC

CHECKLIST FOR NBFC RBI COMPLAINCES

An NBFC which is duly registered with RBI in India, can accept the public deposits. There are a few regulations that The Non-Banking Financial Companies has to fulfil for the acceptance of public deposit.

Below is a summarized table of the compliances for NBFC according to month, quarter and Annually.

| Serial No. | Particulars | Timeframe |

| Monthly Compliance of NBFC | ||

| 1 | NBFC Monthly Return filling | By 7th of every month |

| Periodical Compliance of NBFC | ||

| 1 | Adoption of any notification in ensuing BOD Meeting of NBFC & filing certified copy with RBI | – |

| 2 | Resignation of Director (DIR-12 + Challan Receipt) of NBFC | Within Thirty days of Appointment under the NBFC |

| 3 | Appointment of Director of NBFC | Within Thirty days of Appointment under the NBFC |

| Annual Compliance of NBFC | ||

| 1 | Information about Companies having FDI/Foreign Funds | On or before Thirty June |

| 2 | Audited March Monthly return/NBS7 | On completion |

| 3 | Unaudited March Monthly return/NBS7 | On or before Thirty June |

| 4 | Declaration of Auditors to Act as Auditors of the Company | Annual basis |

| 5 | Audited March Monthly return/NBS-7 | On completion |

| 6 | Statutory Auditors Certificate on Income & Assets | On or before Thirty June |

| 7 | Resolution of Non-acceptance of Public Deposit | Before the commencement of the new FY |

| 8 | File audited annual balance sheet and P&L Account | One month from the date of sign off |

Returns to be submitted by Non-Banking Financial Companies

Compliance by Non Banking Financial Companies under RBI Regulations – Different returns and intimations

List of Returns to Be Submitted By The Non-Banking Financial Companies,

For deposit taking NBFC

- NBFC-1 Return: every quarter NBFC-1 is to be submitted. The motive of NBS-1 Return is to summarize financial details of the company. Eg : asset and liabilities , profit and loss etc.

- NBFC-2 Return: The prudential norms are to be submitted quarterly. The main motive of NBFC-2 return is to summarize compliance for The Non-Banking Financial Companies such as NOF, capital adequacy, provisioning, asset classification etc.

- NBFC-3 Return: It is a quarterly return as well. The motive to submit this report is to get information on statutory investment in liquid asset. Statutory investment include FD in, State or Central Government Securities, Scheduled Commercial Banks etc.

- NBFC-4 Return: It is filed annually. The motive of filing NBFC-4 return is to check the repayment status of NBFC. It has to be filed by the NBFC that holds public deposit but whose CoR has been rejected.

- NBFC-6 Return: This has to be filed monthly exposure to the capital market with total assets equal to or more than INR100 Crores.

- Half yearly ALM Return: it has to filed by NBFC whose asset size is above 100 crores, which holds or accepts public deposit of INR 20 crore. The motive of filing this is to find the difference between asset and liability.

- Audited balance sheet and Auditor’s report: This too has to be filed by NBFC accepting/holding public deposit.

- Branch information return: this is a quarterly return. The main motive is to get the reach and geographical spread of The Non-Banking Financial Companies.

By Non depository taking NBFC i.e NBFCs-ND-SI must submit the file below mention returns:

1. NBS-7 Return: It is to be filed quarterly, this includes capital funds, risk asset ratio , risk weighted asset etc.

2. It is mandatory for NBFCs-ND-SI to submit monthly return on important financial parameters.

3. Asset Liability Management Returns: This includes various returns that has to be filed at different intervals.

-

- Assets Liability Mismatch [ALM-YRLY] Statement – Annual basis.

- Statement of Structural liquidity in format ALM [NBS-ALM2] – Half Yearly;

- Statement of short term dynamic liquidity ALM [NBS-ALM1] – Monthly

- Statement of Interest Rate Sensitivity in format ALM – [NBS-ALM3] – Half Yearly.

4. Branch Information Return:All By Non depository taking NBFC i.e NBFCs-ND-SI are obligated to submit this return each quarter.

- Returns to be submitted by NBFC where the Asset below Rs. 500 Cr.

As per the New RBI regulations, NBFC with asset of less than 500 crore has to file annual return. Also, two new formats have been introduced to better capture the financial parameters of NBFC, those are :

- NBS 8 Return: this has to be filed by BFC having asset size between 100 crore and 500 crore.

- NBS 9 Return: this has to be filed by NBFC having asset size of less than 100 crore.

The due date of filing NBS-8 as well as NBS 9 is 30th may. These are filed with a motive of capturing financial details of NBFC including P&L, asset /Liabilities, branch information among other things

Returns to be filed by RNBCs and NBFC ARC

- NBFC- ARC Return: this shall be filed by NBFC arc in order to capture operational and financial details. This includes acquisition, NPA, recovery status among other things.

- NBFC -NBS 1A & NBS 3A: these returns are in regards with financial details like P & L Account, assets & Liabilities, Exposure to sensitive sectors etc.

Reserve Bank of India Intimations applicable for All NBFCs are below mention :

Here’s the list of compliances that all the NBFCs has to fulfil & required to be submitted.

- Filing of Annual Report to Reserve Bank of India: Annual return mus be submitted to the Reserve Bank of India within 15 days of AGM. Balance sheet (Audited) and P&L Account (Audited), along with Director’s report shall be submitted to Reserve Bank of India.

- SAC Certificate or Statutory Auditors Certificate : it refers to statutory Auditor Certificate , this shall be obtain by all NBFC and it must have a certificate of registration u/s 45IA.

- Annual Returns: all Each miscellaneous NBFC accepting deposits & holding must file annual returns in the format given.

- Change in director or principal officers: this needs f given within a month from date of change. Also, all NBFCs within 1 months from the commencement off its business provide a written statement that must contain the following information.

- Name and designation of its principal officers.

- Signature of signature principal officers authorised on behalf of company.

- Name and residential status of all the directors.

If any of the above changes, it shall be intimated to Reserve Bank of India with 1 month from the date of such event of changes.

RBI master directions Prudential rules & Regulation under Chapter IV

Apart from above Prudential rules & Regulation under Chapter IV norms, here’s some other compliances NBFC shall consider.

- Provisioning of Standard asset : Every applicable NBFCs shall make ensure provision for the standard assets at 0.25% of the outstanding.

- Leverage Ratio: The leverage ratio should not be more than 7 for all NBFCs. However, this doesn’t apply to NBFC MFI and NBFC IFC.

- It is not permitted to lend or take any credit against own shares of NBFC.

- Balance Sheet Disclosure: separate disclosure provisions regarding the bad debts or doubtful debts and the depreciation in investment shall be made.

- Classification of Assets: Assets shall be classified as :

-

- Standard

- Sub standard

- Loss Asset

- Doubtful asset.

- Accounting for investments: A Proper investment accounting policy must be planned and implemented frame BOD of Directors of NBFC

- Loans against the company’s shares are prohibited: No applicable NBFC can lend or take a credit against its NBFC own shares.

- Multiple NBFCs: All applicable NBFCs shall be jointly aggregated for the objective of checking the limit of INR 500 Crores asset size.

- Demand / call loans : there should be a separate policy regarding the demand/ call loans and carry the same out.

In summary

NBFC function are monitored & regulated by the Reserve Bank of India. So RBI list down all the provision & compliances to be met. In order to run smoothly and grow more, all NBFC must obey essential to adhere the rules provided by the RBI.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.