Residential Status U/s 6 of the Income Tax Act Act in short

Table of Contents

Residential Status U/s 6 of the Income Tax Act Act in short

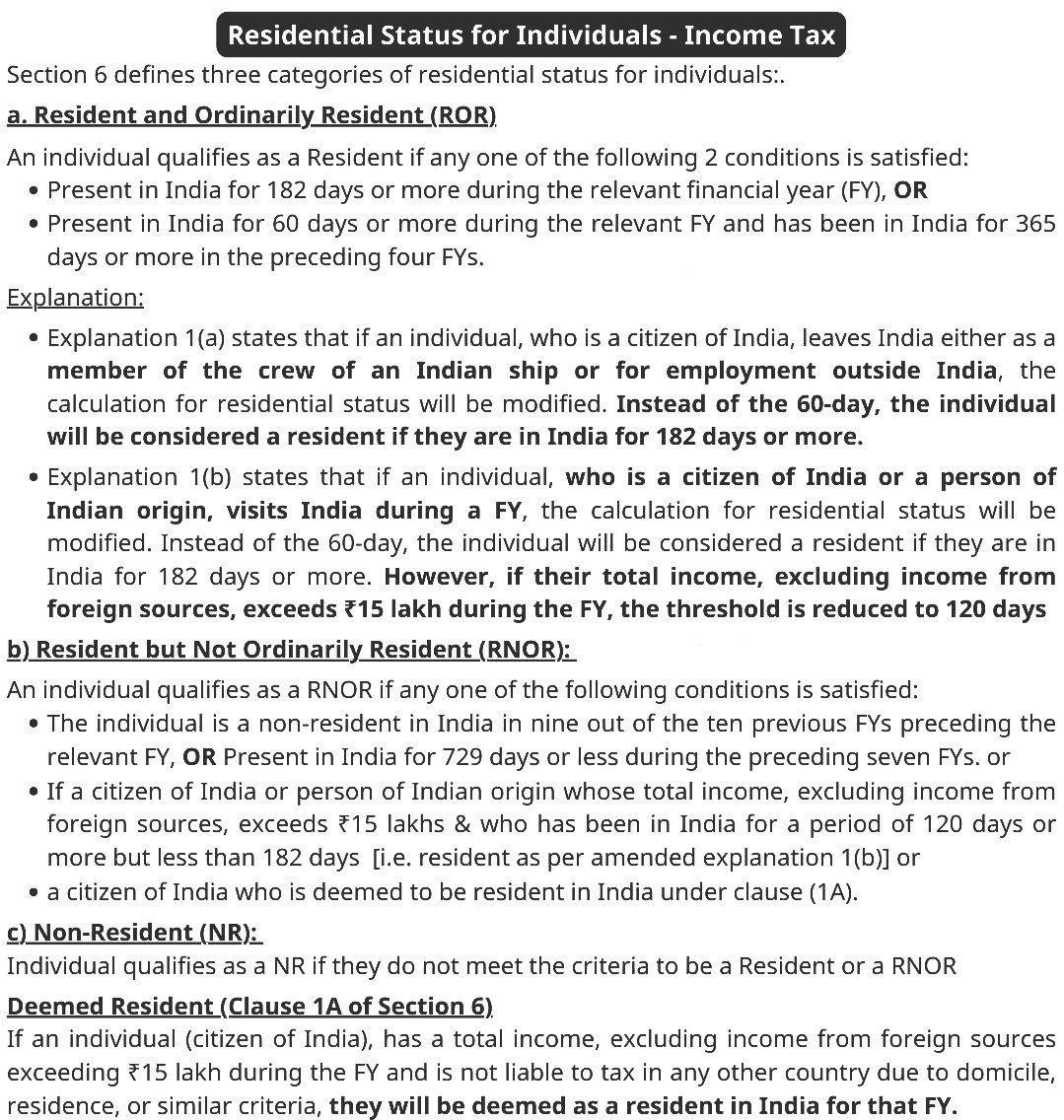

The taxability of an individual in India is determined by their residential status for a specific financial year. An Indian citizen may or may not be a resident of India based on specific criteria.

Classification of Taxable Persons:

An individual’s residential status is classified into three categories:

-

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (RNOR)

- Non-Resident (NR)

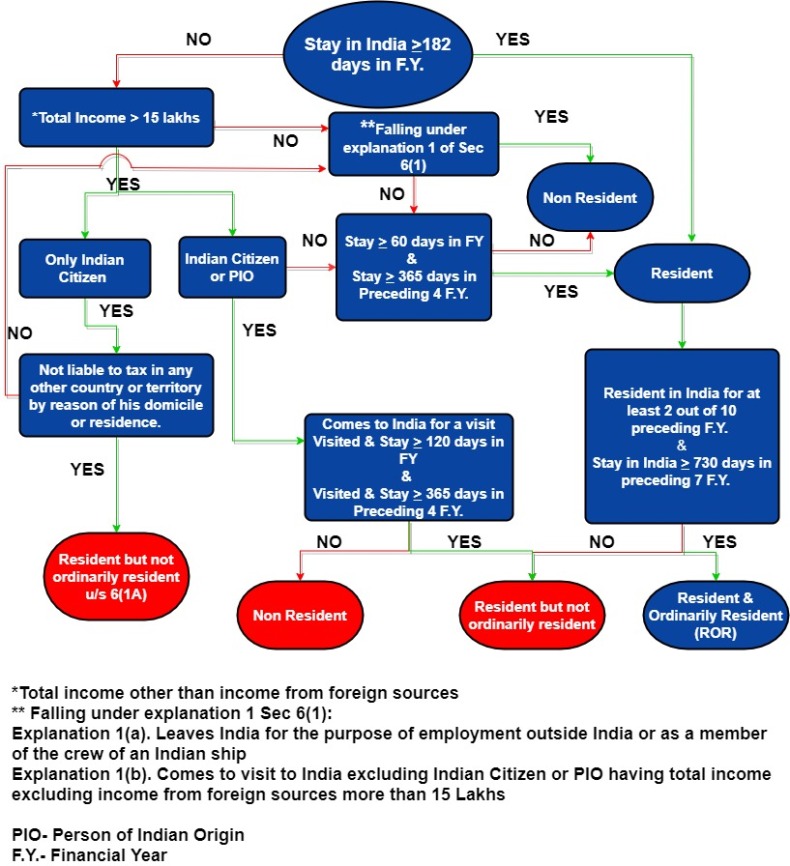

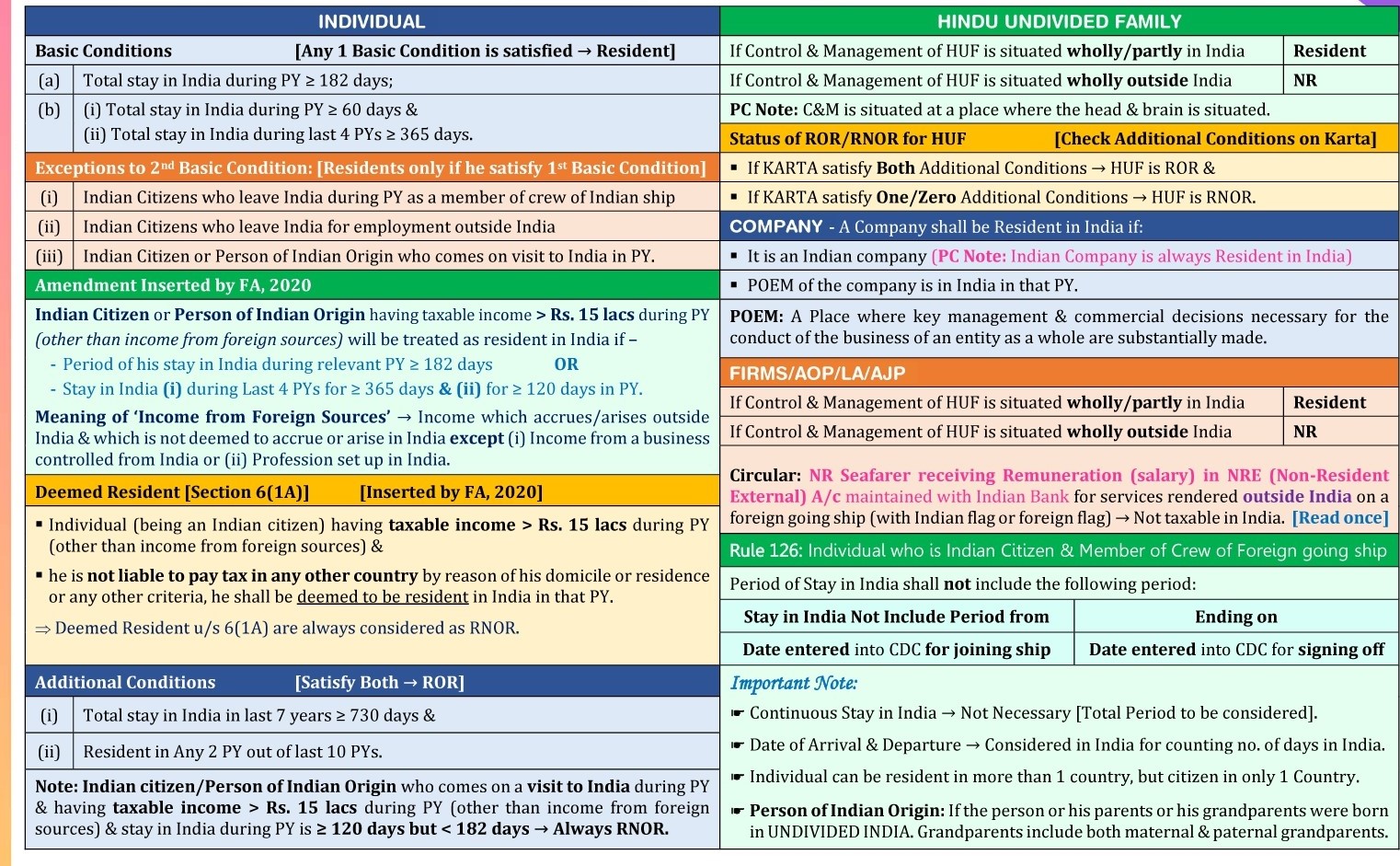

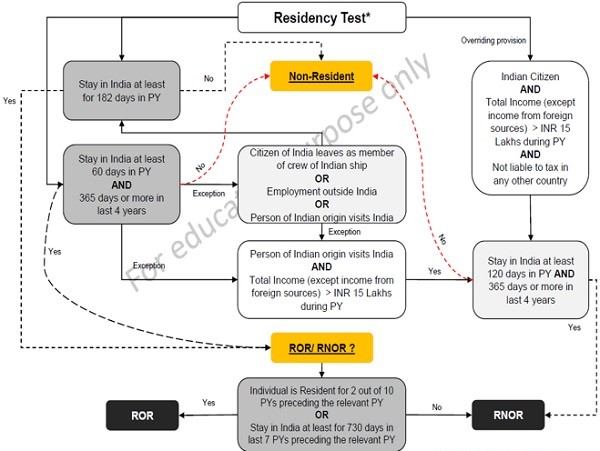

- Resident and Ordinarily Resident (ROR): An individual is considered a resident of India u/s 6(1) of the Income Tax Act if they satisfy any of the following:

- Stay in India for 182 days or more in a fiscal year, or

- Stay in India for 60 days or more in a fiscal year and 365 days or more in the four years immediately preceding that fiscal year.

To be classified as “ordinarily resident,” the individual must also meet these additional conditions under Section 6(6):

-

- Spent 730 days or more in India in the seven preceding years.

- Has been a resident for at least 2 out of 10 previous years before the current year.

- Resident but Not Ordinarily Resident : An individual is classified as RNOR if:

- They meet the basic residence conditions (as in ROR) but do not satisfy the additional conditions under Section 6(6) regarding 730 days of stay or residency in 2 of the past 10 years.

- Non-Resident: If an individual does not satisfy any of the conditions mentioned under the resident category, they are classified as a non-resident.

Amendments Made in Finance Act 2020:

I : Non-Residents now include individuals of Indian origin who:

-

- Earn income exceeding ₹15 lakhs from India,

- Have stayed in India for less than 120 days,

- Do not have their global income taxed in any other country.

II : RNOR category now includes individuals of Indian origin who:

-

- Stay in India for more than 120 days but less than 182 days,

- Do not have their global income taxed in any other country.

Residential Status of Other Entities:

- Residential Status of a Company: A company is considered a resident of India if:

- It is an Indian company, or

- The place of effective management (PoEM) during the previous year is in India. This refers to the place where key management and commercial decisions are made.

- Hindu Undivided Family (HUF):

-

- Resident HUF: Managed by members residing in India.

- RNOR HUF: If the Karta (manager) fulfills the following:

- Resident for at least 2 out of 10 previous years.

- Stay of 730 days or more in the preceding 7 years.

- Firms, LLPs, AOPs, BOIs, Local Authorities, Artificial Juridical Persons:

- Similar to HUF: Residential status depends on where the management is located.

- Additional Notes on Residential Status

-

- Crew Members: In the case of Indian citizens who are part of a ship’s crew, the period of stay does not include time spent on an eligible voyage, determined by the Continuous Discharge Certificate.

- Foreign Companies: A foreign company can be considered a resident if its effective management is proven to be conducted from India for the preceding year.

Key Points on Residential Status Under Section 6 of the Income Tax Act

- Stay in India:

- Includes stays in territorial waters of India (12 nautical miles from the coastline).

- Stay does not have to be continuous or active.

- Both date of arrival and departure are counted in determining days stayed in India.

- Citizenship and Residence:

- Residential status is independent of citizenship, place of birth, or domicile.

- An individual can be a resident in more than one country while having only one domicile.

Important Terminologies relation to Residential Status in income tax act :

- Income from Foreign Sources: Income earned outside India, excluding income sourced from a business or profession in India.

- Non-Resident Indian (NRI): An NRI is an Indian citizen or of Indian origin who is not a resident as per Section 6 of the Act.

- Person of Indian Origin (PIO): A person is considered of Indian origin if they, their parents, or grandparents were born in undivided India.

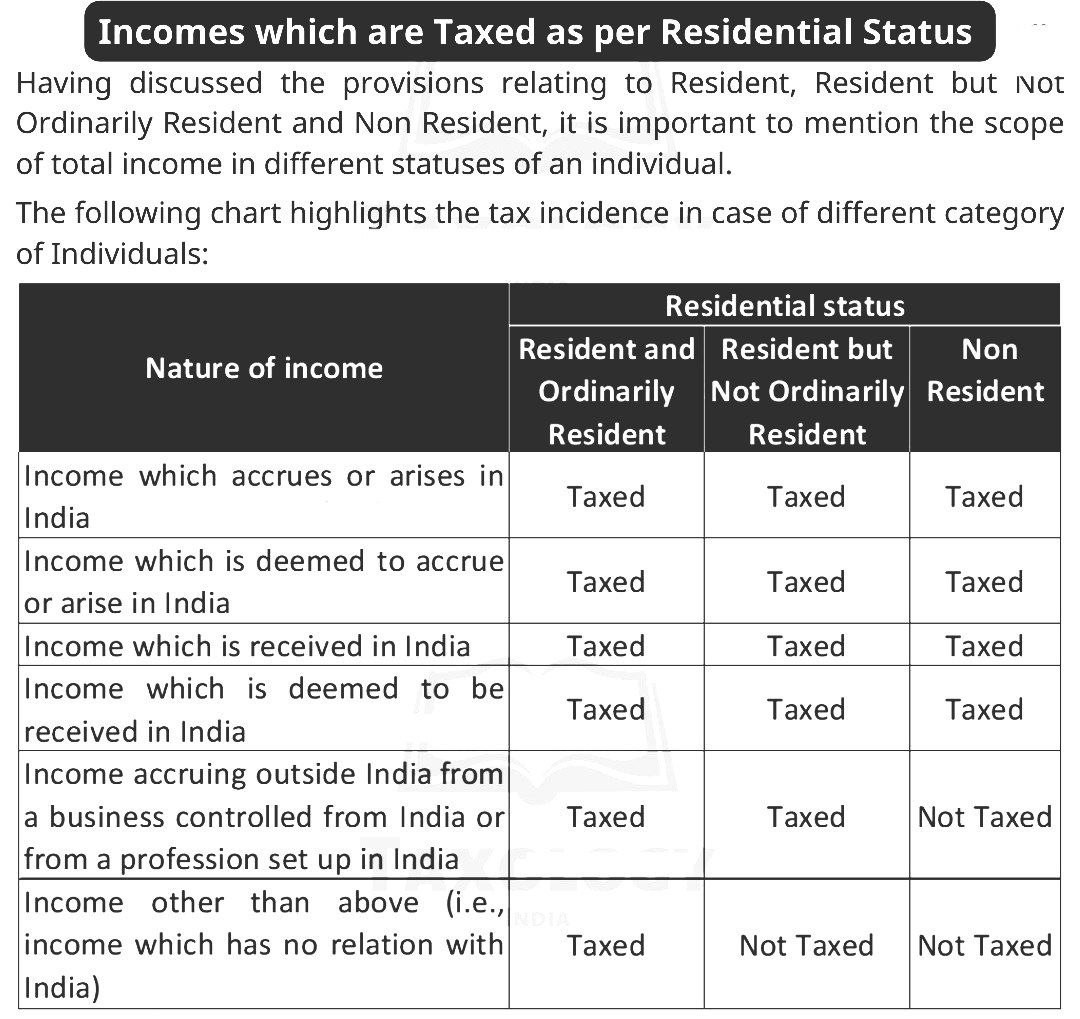

Taxability Based on Residential Status

-

- Resident and Ordinarily Resident: Taxable on global income, i.e., income earned both inside and outside India.

- Resident but Not Ordinarily Resident: Not required to pay tax on: Income earned and received outside India.

- Non-Resident : Taxed only on: Income received in India or sourced from India. And Income earned outside India that has no connection with India is not taxable.

FAQs on Residential Status Under Section 6 of the Income Tax Act

- When does a person become a resident in India?

- If the individual stays for 182 days or more in a year, or

- 60 days in a year and 365 days in the preceding 4 years.

- When does a person become a Resident and Ordinarily Resident (ROR)?

- Resident for 2 years out of the previous 10 years, and

- Stayed in India for 730 days or more in the preceding 7 years.

- Who is a deemed resident?

- An Indian citizen with income over ₹15 lakhs (excluding foreign sources) and not taxable in any other country due to residence or domicile is a deemed resident and will be treated as an RNOR.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.