Application of GST on Contribution By RWA Members

Table of Contents

Read about the Application of GST on Contribution By RWA Members

BRIEF INTRODUCTION

With the introduction of GST in 2017, Entry 77 was introduced via Notification No. 12/2017-CT dated June 28, 2017. As per the notification, exemption was granted in respect of contribution, being received by RWAs in way over Rs. 7,500. As per the clarifications issued by CBIC, it was provided that GST will be leviable on consideration made in excess of Rs. 7,500.

However, afterward an RWA filed an application before the Authority of Advance Ruling to hunt clarification in this matter. Hon’ble AAR held adverse and stated that exemption is offered as long as contribution is received up to Rs. 7,500. Therefore, If the contribution amount exceeds Rs. 7,500 then the whole contribution is susceptible to GST. If an excess amount is received then the whole contribution would be susceptible to GST. Therefore, a petition was filed by the petitioner before Hon’ble high court, thereby challenging the validity of Ruling of AAR and Circular being issued by CBIC.

| (1) | (2) | (3) | (4) | (5) |

| SL. NO. | CHAPTER, SECTION, HEADING, GROUP OR SERVICE CODE (TARIFF) | DESCRIPTION OF SERVICES | RATE (PER CENT.) | CONDITION |

| 1 | ……… | |||

| 77 | HEADING 9995 | SERVICE RENDERED BY AN UNINCORPORATED ENTITY OR NGO REGISTERED UNDER THE LAW FOR TIME BEING IN FORCE, IN RESPECT OF ITS OWN MEMBERS IN THE FORM OF CONTRIBUTION OR REIMBURSEMENT OF EXPENSES –

(A) AS A TRADE UNION; (B) IN RESPECT OF CARRYING OUT ANY ACTIVITY, BEING EXEMPT FROM THE GST; OR (C) UP TO AN AMOUNT OF RS. 7,500 PER MONTH IN RESPECT OF EACH MEMBER, FOR SUPPLY OF GOODS OR SERVICES FROM A THIRD PERSON AND THE SAME IS MADE FOR A COMMON USE OF ITS MEMBERS. |

NIL | NIL |

Entry No. 78 Services by an artist

| (1) | (2) | (3) | (4) | (5) |

| SL. NO. | CHAPTER, SECTION, HEADING, GROUP OR SERVICE CODE (TARIFF) | DESCRIPTION OF SERVICES | RATE | CONDITION |

| 1 | ……… | |||

| 78 | 9996 | SERVICES RENDERED BY AN ARTIST, IN THE FORM OF PERFORMANCE IN FOLK OR CLASSICAL ART LIKE –

(A) MUSIC, OR (B) DANCE, OR (C) THEATRE,

WHERE THE CONSIDERATION CHARGED DOES NOT EXCEED RS. 1,50,000: PROVIDED THE SAID SERVICE IS NOT PROVIDED BY ARTIST AS A BRAND AMBASSADOR. |

NIL | NIL |

GOVERNING CASE STUDY

It was held by the Hon’ble high court, that the words employed in Entry 77, ‘up to’ an amount of Rs.7,500/-, are to be interpreted, that any contribution, being in excess of said amount, shall be susceptible to GST. It means that the amount up to Rs. 7,500/- would be exempt from the application of GST. Therefore, The clarification by the GST Department at the same time as early as in 2017 has taken the right view.

BRIEF FACTS

- A petition was filed by RWA against an Advance Ruling, wherein it was held that GST would be leviable on the whole amount of contribution received by RWA from its members.

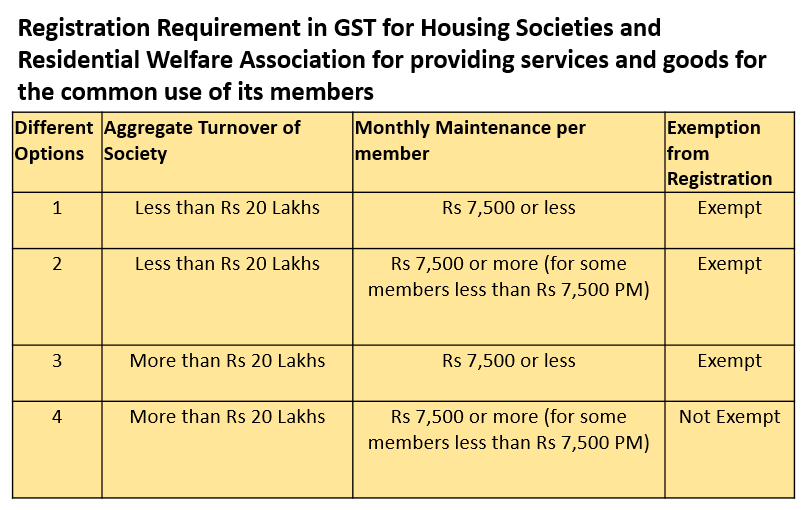

- After the introduction of GST, an exemption was provided in respect of contribution made by the members of RWA and the same was provided by the Notification 12/17- CT dated 28.06.2017. Thus, an exemption would be provided where such contribution does not exceed Rs. 5,000 per month per member. However, vide Notification No.2/18 dated 25.01.2018, the said limit of Rs. 5,000 was raised to Rs. 7,500.

- Therefore, exemption be granted in respect of contributions made to RWA and the same be available to Rs. 7,500/- per month per member.

- In many cases, RWA received contributions in more than Rs. 7,500. In such situation, question arose that:

- Whether just in case the amount of contribution exceeds Rs. 7,500, the RWA will not have the advantage of exemption, and hence, the entire contribution of Rs. 7,500 would be taxable under GST; or

- In Initial period, GST Department issued clarification just in case of Co-operative Housing Society wherein it had been specifically mentioned that GST would be applicable on consideration received in far more than Rs. 7,500.

- Therefore, considering the clarification, all RWAs were levying GST on contributions received accordingly.

- However, in 2009, one among the petitioners approached the Authority of advance ruling seeking clarification on this matter.

- Hon’ble AAR held adverse and stated that exemption is available given that contribution is received up to INR 7,500. If contribution amount exceeds INR 7,500 then entitlement of exemption would stand defeated and full contribution are going to be susceptible to GST.

- After the ruling of Hon’ble AAR, CBIC, it was clarified that exemption in respect of contribution made up to an amount of Rs. 7,500 would be exempt. However, in case of excess amount is received, the entire amount of contribution would be susceptible to GST.

ISSUES IN RESPECT OF GST ON CONTRIBUTION BY RESIDENTIAL WELFARE ASSOCIATION FROM ITS MEMBERS –

| SL. NO. | ISSUE | CLARIFICATION |

| 1. | …….. | |

| 5. | HOW SHOULD THE RWA CALCULATE GST PAYABLE WHERE THE MAINTENANCE CHARGES EXCEED ₹ 7500/- PER MONTH PER MEMBER? IS THE GST PAYABLE ONLY ON THE AMOUNT EXCEEDING ₹ 7500/- OR ON THE ENTIRE AMOUNT OF MAINTENANCE CHARGES? | GST EXEMPTION IN RESPECT OF MAINTENANCE CHARGES RECEIVED BY RWA FROM ITS MEMBERS WOULD BE AVAILABLE PROVIDED THE AMOUNT DOES NOT EXCEED RS. 7500/- PER MONTH PER MEMBER. WHERE THE SAID AMOUNT OF CHARGES EXCEEDS RS. 7500/- PER MONTH PER MEMBER, THE WHOLE AMOUNT OF CONSIDERATION WOULD TAXED UNDER GST. FOR EXAMPLE, IF THE MAINTENANCE CHARGES ARE ₹ 9000/- PER MONTH PER MEMBER, GST @ 18% SHALL BE PAYABLE ON THE ENTIRE AMOUNT OF ₹ 9000/- AND NOT ON (₹ 9000₹ 7500) = ₹ 1500/- |

- Aggrieved with the circular of CBIC and ruling of AAR, a petitioner filed a petition (W.P.No.27100 of 2019) before the Hon’ble Madras high court, challenging the Circular No.109/28/2019 dated 22.07.2019, in respect of difficulty of levying of GST on the amount of contribution received by RWA.

RELEVANT LEGAL EXTRACTS

- “Description of Service” under Entry No. 77 of Notification No. 12/2017- CT dated 28.06.2017 has been explained herein –

“Service by an unincorporated entity or NGO registered under the law, for time in force, to its own members by way of reimbursement of charges or amount of contribution-

(a) as a trade union;

(b) for the supply of completing any activity which is exempt from the levy of goods and service tax; or

(c) up to an amount of Rs. 7,500/- per month for each member, in respect of supply of products or services, being received from a 3rd person for the common use of its members.”

- The extract of the circular later issued by department is as follows –

| S. NO. | ISSUE | CLARIFICATION |

| 5. | HOW SHOULD THE RWA CALCULATE GST PAYABLE WHERE THE MAINTENANCE CHARGES EXCEED RS.7500/- PER MONTH PER MEMBER? IS THE GST PAYABLE ONLY ON THE AMOUNT EXCEEDING RS.7500/- OR ON THE ENTIRE AMOUNT OF MAINTENANCE CHARGES? | GST EXEMPTION IN RESPECT OF MAINTENANCE CHARGES RECEIVED BY RWA FROM ITS MEMBERS WOULD BE AVAILABLE PROVIDED THE AMOUNT DOES NOT EXCEED RS. 7500/- PER MONTH PER MEMBER. WHERE THE SAID AMOUNT OF CHARGES EXCEEDS RS. 7500/- PER MONTH PER MEMBER, THE WHOLE AMOUNT OF CONSIDERATION WOULD TAXED UNDER GST. FOR EXAMPLE, IF THE MAINTENANCE CHARGES ARE ₹ 9000/- PER MONTH PER MEMBER, GST @ 18% SHALL BE PAYABLE ON THE ENTIRE AMOUNT OF ₹ 9000/- AND NOT ON (₹ 9000₹ 7500) = ₹ 1500/- |

CONTENTION OF THE PETITIONER

The petitioner contended that:

1. Interpretation made by the Department is believed to be in contrary with the express language and intention of the exemption granted under the circular.

2. Also, according to Article 13(3) of the Constitution of India, the withdrawal of any statutory exemption, by issuance of a circular shall stand in contrary to the provisions of the constitution.

3. Further, based on the initial clarification provided by the Department itself, the petitioner RWAs were required to collect GST only on the amount of contribution in excess of Rs.7,500/-. However, in a contrary view, it’d be impossible for the RWAs to gather the shortfall as there would are several changes in ownership of the property, within the interim.

CONTENTION OF THE RESPONDENT

Ld. Counsel of the Respondent contended that:

1. Stress was placed on Section 15 of CGST Act, as per which, GST is leviable on transaction value. within the given case, transaction value is contribution received and it should entirely be taken into consideration for levying taxes.

2. Also, exemption is supposed for middle classes and not for luxury apartments/their owners.

3. Also, within the exemption notification, no slabs are given. Instead, a range has been provided, thereby entitling the assessee for exemption.

4. Also, respondent place reliance on ruling of apex court within the matter of Commissioner of Customs Import, Mumbai V. Dilip Kumar & Company (361 ELT 577) wherein it absolutely was held that within the case of ambiguity in interpretation of a tax exemption provision or Notification, interpretation should be strict and also the burden of proving applicability would fall on the assessee. Therefore, during this case, the exemption provision must be construed strictly and therefore the petitioners are thus not entitled to seek beneficial treatment.

ANALYSIS BY HON’BLE HIGH COURT OF MADRAS

The Hon’ble Madras high court made the following analysis –

1. Within the given cases, there’s no ambiguity within the language of the exemption provision. Therefore, judgment of the Supreme Court in Dilip Kumar (supra) wouldn’t be applicable to this case.

2. Intention of exemption notification is evident that it wants to remove contribution from the purview of taxation up to an amount of Rs.7,500/-.

3. If a comparison is applied of this exemption with language of other exemptions, then it clearly appears the difference in language adopted by the revenue within the matter of grant of exemptions.

4. In a very case where legislature intended that the exemption shall apply only to cases where the number charged doesn’t exceed a specified pecuniary limit, it states the maximum amount, where it’s stated that the exemption would be available only where the gross amount of consideration doesn’t exceed Rs.5,000/- in a particular financial year.

5. Similarly in entry No. 78 of Notification No.12/2017 dated 28.06.2017, exemption is offered to following:

Services by an artist, in the form of performance in folk or classical art as –

(a) music, or

(b) dance, or

(c) theatre,

Where the consideration charged for such performance does not exceed Rs. 1,50,000. However, it is to be noted that the said exemption shall not be available in respect of service provided as a brand ambassador.

6. “Artist” are categories supported their earnings. One who charges but INR 1.50 Lacs are exempted. If consideration exceeds INR 1.50 lakhs even by a rupee, then artist would lose the advantage of exemption.

7. These entries are given in same exemption notification thus the selection of words employed could be a conscious one intended to possess different applications.

8. As per Apex Court just in case of Dilip Kumar (supra), the Supreme Court reiterates the settled proposition that an Exemption Notification must be interpreted strictly. Thus, as per Entry 77, being, ‘up to’ an amount of Rs.7,500/-, can be interpreted that where the contribution exceeds Rs. 7,500, the amount in excess would be susceptible to tax.

9. The term ‘up to’ connotes an upper limit and also the same is interchangeable with the term ‘till’. Thus, the amount up to Rs.7,500/- would be exempt from the application of GST.

10. As regards the argument concerning slab rate, a slab may be a measure of determining liabilities. The intendment of the exemption Entry in question is just to exempt contributions till a particular specified limit.

11. Therefore, The clarification by the GST Department when early as in 2017 has taken the right view.

FINAL DECISION BY HON’BLE MADRAS HIGH COURT

Hon’ble supreme court held that Clarification by the GST Department in 2017 was correct. The judgement lapsed AAR and further passed the Circular by the CBDT is prone to be put aside. Therefore, no GST is applicable on contribution received up to INR 7,500 and just in case of contribution received in way over INR 7,500, GST would levy only on additional amount.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.