Advance Tax payment –Due Dates, Applicability, Procedure

Table of Contents

All About the Advance Tax Payment—Due Dates, Applicability, Procedure, and Installment Details:

We are providing a comprehensive overview of advance tax, covering its definition, who needs to pay, exemptions, due dates, treatment of capital gains and casual income, consequences of default, choosing the correct assessment year, mode of payment, calculation method, and the interest on late or non-payment. This breakdown is helpful for taxpayers to understand their obligations and avoid penalties.

What is Advance Tax?

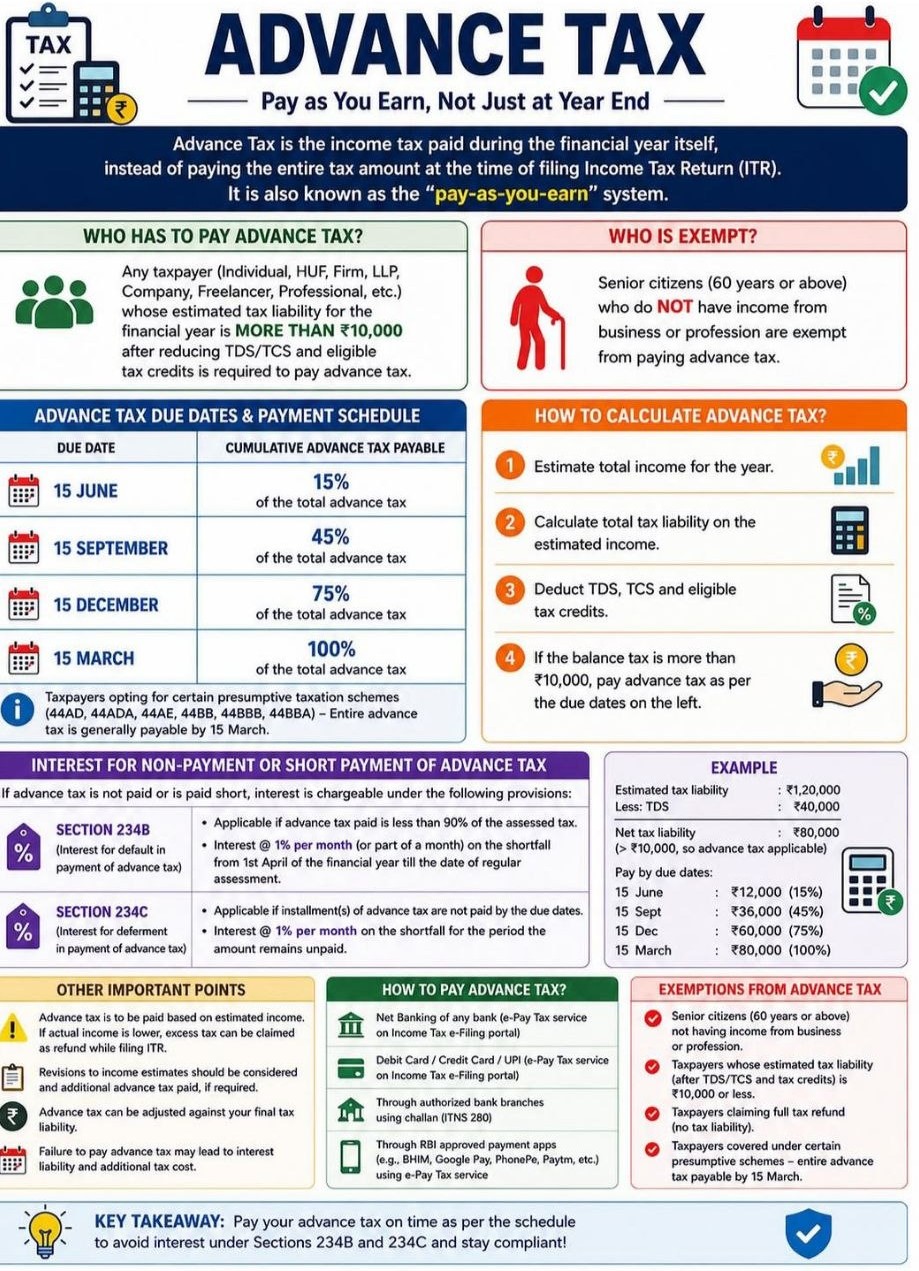

Advance tax is a mechanism through which taxpayers pay their taxes in installments over the course of the financial year, rather than in a lump sum at the end of the year.

– Payment made in the same year as the earned income.

– ‘Pay as you earn’ concept.

who should pay advance tax, covering various categories of taxpayers:

Salaried individuals, freelancers, and businesses: Anyone whose total tax liability is Rs 10,000 or more in a financial year must pay advance tax. This applies to all taxpayers, including salaried individuals, freelancers, and businesses.

In case any Senior citizens: Individuals aged 60 years or above who do not run a business are exempt from paying advance tax. Therefore, only senior citizens with business income are required to pay advance tax.

If the case of Presumptive income for businesses (Section 44AD): Taxpayers who have opted for the presumptive taxation scheme under section 44AD must pay their entire advance tax liability in one installment on or before March 15. They also have the option to pay all their tax dues by March 31.

Presumptive income for professionals (Section 44ADA): Independent professionals like doctors, lawyers, architects, etc., who come under the presumptive scheme as per section 44ADA, are required to pay their entire advance tax liability in one installment on or before March 15. Alternatively, they can pay the entire amount by March 31.

Here’s a breakdown of the key aspects of advance tax:

Who Pays Advance Tax?

– If tax liability exceeds Rs 10,000 after TDS deduction.

– Liability paid in the same financial year.

Who is Exempt?

Exemption: There are certain exemptions and conditions under which individuals or entities may not be required to pay advance tax. For instance, senior citizens (individuals aged 60 years or above) who do not have any income from business or profession are exempt from paying advance tax.

– Resident senior citizens without business income.

– Those under presumptive taxation scheme (section 44AD or section 44ADA).

Advance Tax Due Dates:

Deadline: Advance tax payments are typically made in installments during the financial year. The deadlines for these installments are specified by the Income Tax Department. For individuals, the due dates for advance tax payments are usually June 15, September 15, December 15, and March 15 of the financial year

– June 15: 15% of advance tax

– Sept 15: 45% (- taxes paid)

– Dec 15: 75% (- taxes paid)

– Mar 15: 100% (- taxes paid)

Capital Gains and Casual Income:

– Tax applicable on total income, including capital gains.

– Tax on such income paid in remaining installments if received after due dates.

Assessee-in-Default:

If a taxpayer fails to pay advance tax or pays an amount lesser than the required installment, they may be considered an “assessee-in-default.” In such cases, the taxpayer may be liable to pay interest under section 234B and section 234C of the Income Tax Act. Interest is levied for default in payment of advance tax as per the specified rates.

– Default if advance tax not paid on time.

– Failure to file intimation in Form 28A before due date.

Choosing the Right Assessment Year:

Mode of Payment: Advance tax can be paid online through the Income Tax Department’s website or at designated bank branches. Taxpayers are required to use Challan 280 for making advance tax payments.

– Pay attention to details in challan.

– Select correct head of payment, tax amount, and method.

– Choose the correct Assessment Year (AY)—2023–24 for the fiscal year 2022–2023.

Calculating Advance Tax:

– Estimate current year income.

– Deduct TDS/TCS for the current year.

– Determine Advance Tax liability.

Interest on Late Payment/Non-Payment:

Consequences of Non-payment: Failure to pay advance tax or paying less than the required amount can lead to interest charges and penalties. Additionally, it may also attract scrutiny from the Income Tax Department, which could result in further consequences such as penalties or legal action.

– Sec 234B: 1% interest if 90% of tax not paid by fiscal year-end.

– Sec 234C: Gradual interest on each installment if not paid on time.

It’s essential for taxpayers to adhere to the advance tax payment deadlines and fulfill their tax obligations to avoid any penalties or legal repercussions

About IFCCL

IFCCL is recognized as the best tax consultant for income tax filing in India, offering comprehensive and result-oriented taxation services to individuals, professionals, and corporations. We specialize in Advance tax calculation, ensuring timely compliance and accurate estimation to avoid interest and penalties. Our expert team provides strategic Capital gains tax advisory to help clients optimize tax liability on property, shares, and other investments. We also focus on Tax savings for salaried individuals, guiding clients on deductions, exemptions, and smart structuring to maximize benefits under applicable tax laws. With dedicated Corporate taxation support, IFCCL assists businesses in compliance, planning, assessments, and representation before tax authorities. If you are looking for practical solutions on How to save income tax legally in India, IFCCL delivers personalized strategies backed by deep regulatory knowledge and professional excellence. Contact us at 9555 555 480 or Singh@carajput.com/singh@caindelhindia.com

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.