FAQ’s on Goods and Services Tax

Q.: What is GST and GSTR Filings?

GST, or Goods and Services Tax, is an indirect tax that has replaced multiple taxes in India, including the VAT System, since its implementation on July 1st, 2017. On March 29th, 2017, the GST Act was passed by Parliament. GST is regarded as a ‘comprehensive, multi-staged, and destination-based’ taxation system.

Q.: What is GST, and how does it function?

GST is a single indirect tax for the entire country, bringing India closer together as a single market.

The Goods and Services Tax (GST) is a single tax on the supply of goods and services from the manufacturer to the consumer. Credits for input taxes paid at each stage will be available in the subsequent stage of value addition, making GST essentially a value addition tax at each stage.

As a result, only the GST imposed by the last dealer in the supply chain will be passed on to the final consumer.

Q.: Which central and state taxes are being absorbed into the GST?

The following taxes are subsumed at the central level.

- Central Excise Duty,

- Additional Excise Duty,

- Service Tax,

- Countervailing Duty is a type of additional customs duty.

- Special Additional Duty of Customs.

The following taxes are being absorbed at the state level.

- State V.A.T. and Sales Tax are combined.

- Central Sales Tax, Entertainment Tax (other than taxes levied by local governments) (levied by the Centre and collected by the States).

- Octroi and Entry tax,

- Purchase Tax,

- Luxury tax, and

- Taxes on lottery, betting and gambling.

Q.: What are the important events in the timeline that led to the implementation of GST?

After a 13-year journey since it was originally mentioned in the Kelkar Task Force report on indirect taxes, GST is finally being implemented in the country. The following is a quick timeline of the significant milestones in the proposal for the establishment of GST in India:

- A comprehensive Goods and Services Tax (GST) based on the VAT premise was proposed by the Kelkar Task Force on indirect taxes in 2003.

- In the Budget Speech for the fiscal year 2006-07, a plan to impose a national Goods and Services Tax (GST) by April 1, 2010 was originally proposed.

- Because the proposal included not only reform/restructuring of indirect taxes levied by the Centre but also by the States, the Empowered Committee of State Finance Ministers was tasked with developing a Design and Road Map for GST implementation (EC).

- In November 2009, the EC presented its First Discussion Paper on Goods and Services Tax in India, based on contributions from the Indian government and states.

- In September 2009, a Joint Working Group comprised of officers from the Central and State Governments was formed to continue the GST-related activities.

- In March 2011, the Constitution (115th Amendment) Bill was introduced in the Lok Sabha in order to amend the Constitution to allow for the introduction of GST. The Bill was referred to the Parliament’s Standing Committee on Finance for examination and report, as per the prescribed procedure.

- Meanwhile, a ‘Committee on GST Design’, comprised of officials from the Government of India, State Governments, and the Empowered Committee, was formed in response to a decision made at a meeting between the Union Finance Minister and the Empowered Committee of State Finance Ministers on November 8, 2012.

- This Committee conducted a thorough examination of GST design, as well as the Constitution (115th) Amendment Bill, and submitted its report in January 2013. In their meeting in Bhubaneswar in January 2013, the EC suggested several revisions to the Constitution Amendment Bill based on this Report.

- At the Bhubaneswar meeting, the Empowered Committee also decided to form three committees of officers to discuss and report on various aspects of GST, as follows.

- Committee on Revenue Neutral Rates and Place of Supply Rules

- Dual control, thresholds, and exemptions committee

- IGST and GST on Imports Committee

- In August 2013, the Parliamentary Standing Committee gave its report to the Lok Sabha. In consultation with the Legislative Department, the Ministry examined the recommendations of the Empowered Committee and the Parliamentary Standing Committee. The majority of the Empowered Committee’s and Parliamentary Standing Committee’s recommendations were accepted, and the draught Amendment Bill was appropriately revised.

- In September 2013, the Empowered Committee received the final draught Constitutional Amendment Bill incorporating the aforementioned changes.

- Following its November 2013 meeting in Shillong, the EC issued new recommendations on the Bill. The proposed Constitution (115th Amendment) Bill included some of the Empowered Committee’s suggestions. In March of 2014, the amended draught was given to the Empowered Committee for review.

- The 115th Constitutional (Amendment) Bill, 2011, introduced in the Lok Sabha in March 2011 for the introduction of GST, lapsed with the dissolution of the 15th Lok Sabha.

- After the new government’s approval, the draught Constitution Amendment Bill was sent to the Empowered Committee in June 2014.

- On 17.12.2014, the Cabinet approved the proposal for the introduction of a Bill in Parliament to amend the Constitution of India to facilitate the introduction of the Goods and Services Tax (GST) in the country, based on a broad consensus reached with the Empowered Committee on the Bill’s contours. The Bill was tabled in the Lok Sabha on December 19, 2014, and it was passed on May 6, 2015. It was then referred to the Rajya Sabha Select Committee, which issued its findings on July 22, 2015.

Q.: How would a goods-and-services transaction be taxed concurrently under the Central GST (CGST) and the State GST (SGST)?

Except for exempted products and services, goods that are outside the scope of GST, and transactions that are below the stipulated threshold limitations, the Central GST and the State GST will be levied simultaneously on every transaction of supply of goods and services. Furthermore, unlike State VAT, which is paid on the value of the items plus Central Excise, both would be levied on the same price or value.

Q.: Will cross-crediting between goods and services be permitted under the GST regime?

The use of CGST credit for both products and services would be permitted. In the event of SGST, the opportunity of credit cross-utilization will also be accessible. However, under the IGST model, cross-utilization of CGST and SGST would be prohibited except in the event of inter-State supply of goods and services, as detailed in the next question.

Q.: In terms of the IGST approach, how will inter-state transactions of goods and services be taxed under GST?

The Centre would impose and collect the Integrated Goods and Services Tax (IGST) on all inter-State supplies of goods and services under Article 269A (1) of the Constitution in the case of inter-State transactions. The IGST would be equal to the sum of the CGST and the SGST. The IGST method was created to ensure that input tax credits flowed smoothly from one state to the next. After allocating credit for IGST, CGST, and SGST on his purchases, the inter-State seller would pay IGST on the sale of his goods to the Central Government (in that order). The credit for SGST used in IGST payment would be transferred to the Centre by the exporting state. While discharging his output tax duty (both CGST and SGST) in his home State, the importing merchant would claim IGST credit. The IGST credit used in SGST payment would be transferred to the importing State by the Centre. Due to the fact that GST is a destination-based tax, all SGST on the finished product would usually go to the consuming State.

Q.: How will IT be used to carry out GST?

The Central and State Governments have jointly registered the Goods and Services Tax Network (GSTN) as a not-for-profit, non-Government Company to provide shared IT infrastructure and services to the Central and State Governments, tax payers, as well as other stakeholders in preparation for the implementation of GST in the country. GSTN’s main goals are to create a standard and unified interface for taxpayers, as well as common infrastructure and services for the federal, state, and local governments.

GSTN is developing a cutting-edge comprehensive IT infrastructure, which will include a common GST portal that will provide frontend services of registration, returns, and payments to all taxpayers, as well as backend IT modules for specific States that will include processing of returns, registrations, audits, assessments, appeals, and so on. All states, accounting authorities, the Reserve Bank of India, and banks are also preparing their IT infrastructure for GST administration. There would be no filing of returns by manual. All taxes can be paid online as well. There would be no need for manual intervention because all mismatched returns would be generated automatically. The majority of returns would be self-evaluated.

Q.: How will imports be taxed under the GST regime?

The current import duties of Additional Duty of Excise (CVD) and Special Additional Duty (SAD) will be absorbed into the GST. According to the explanation to clause (1) of Article 269A of the Constitution, IGST will be levied on all imports into India’s territory. Unlike under the current regime, the States that consume imported goods will now benefit from the IGST paid on imported commodities.

Q.: What are the main provisions of the Constitution (122nd Amendment) Bill, 2014?

The following are the Bill’s key features.

- Power simultaneously to tax goods and services laws by Parliament and the State legislatures.

- Includes various Central indirect taxes and levies such as Central Excise Duty, Additional Excise Duties, Service Tax, Additional Customs Duty, also known as Countervailing Duty, and Special Additional Duty of Customs.

- State V.A.T./Sales Tax, Entertainment Tax (other than local body taxes), Central Sales Tax (levied by the Centre and collected by the States), Octroi and Entry Tax, Purchase Tax, Luxury Tax, and Lottery, Betting, and Gambling Taxes are all included.

- Defending the Constitution’s definition of “declared commodities of extraordinary importance.”

- Implementation of an Integrated Goods and Services Tax on inter-state goods and services transactions.

- GST will be levied on all goods and services, with the exception of alcoholic beverages for human consumption. Petroleum and petroleum products will be subject to GST levy at a later date to be announced based on the Goods and Services Tax Council’s recommendation.

- Five-year compensation to states for revenue lost as a result of the implementation of the Goods and Services Tax.

- Establishment of the Goods and Services Tax Council to investigate issues pertaining to the goods and services tax and make recommendations to the Union and the States on parameters such as rates, taxes, cesses, and surcharges to be subsumed, exemption list and threshold limits, Model GST laws, and so on. The Council will be managed by the Union Finance Minister and will include representatives from all state governments.

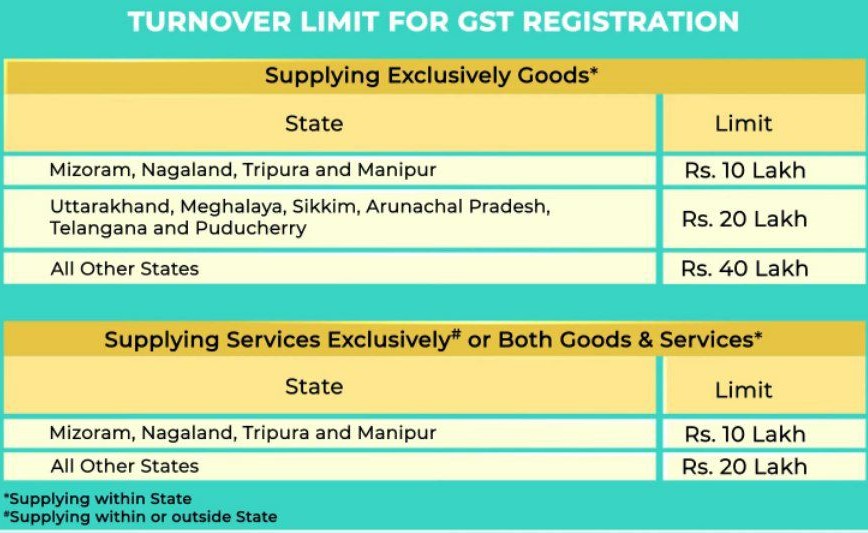

Q.: What are the main characteristics of the proposed GST registration procedures?

The following are the key features of the proposed GST registration procedures.

- Existing distributors: Existing VAT/Central Excise/Service Tax payers will not be required to reapply for GST registration.

- New distributors: GST registration will be accomplished through the submission of a single online application.

- The registration number will be based on the PAN and will serve both the Centre and the State.

- A single application to both tax authorities.

- Each dealer will be assigned a unique GSTIN number.

- Approval is expected within three days.

- Only in risk-based cases will post-registration verification be performed.

Q.: What are the main characteristics of the proposed GST return filing procedures?

The following are the main features of the proposed GST return filing procedures:

- A common return would serve the purposes of both the Centre and the State Governments.

- The GST business processes provide for eight forms for filing returns. The majority of average taxpayers would file their returns using only four forms. There are four types of returns: supply returns, purchase returns, monthly returns, and annual returns.

- Small taxpayers: Small taxpayers who have chosen the composition scheme must file returns on a quarterly basis.

- Returns must be filed entirely online. All taxes can be paid online as well.

Q.: What are the main characteristics of the proposed GST payment procedures?

The following are the main features of the proposed GST payment procedures.

- There is no paper generated during the electronic payment process.

- GSTN is a single point of contact for challan generation.

- Payment convenience – payments can be made via online banking, credit card/debit card, NEFT/RTGS, and cheque/cash at the bank.

- Common challan form with auto-population features

- Use of single challan and single payment instrument

- Common set of authorized banks

- Common Accounting Codes

Q.: In general, how many GSTR-Filings are there?

There are currently 19 different types of GST Returns based on the type of business, origin (residential/non-residential), turnover, monthly, annual, and so on. The basic GST Returns that all normal/regular taxpayers must file on a regular basis are.

GSTR-1: This is the monthly Sales Return Filing that contains information about all of the taxpayer’s outward supplies.

GSTR-2A: This is an auto-populated read-only draught of all purchases made by taxpayers during the tax period. This is auto-populated from the GSTR-1 sales returns filed by all suppliers. As a Recipient, you are unable to make changes.

GSTR-3B: This is the filing in which the taxpayer discharges all of his tax liabilities, either by paying cash or by adjusting the ITC. This is a monthly consolidated summary of Sales, Purchases, and ITC.

GSTR-9: The annual return that must be filed at the end of each year as a consolidated summary of GSTR-1, GSTR-3B, GSTR-2A, and ITC claims or demands.

GSTR-9C: This is the section in which taxpayers must have their accounts audited by a CA and submit the audit report, along with the reconciliation statement, to the GST Portal.

Q.: What exactly is reconciliation?

- Under GST, reconciliation is simply the matching of various reports to identify and correct any mismatches or errors.

- Reconciliation ensures that the records from both the buyer and seller end match, ensuring that the transactions are authentic and correct to the best of their knowledge.

- There will be no false or hidden transactions in the Return Filings as a result of this. GSTR1 & GSTR-3B, GSTR-2A & Purchase Books, Annual Reconciliation, GSTR-1 & e-Way Bill data are the most commonly reconciled.

Q.: What is the mechanism for reverse charge?

- Under the GST Reverse Charge Mechanism, taxes must be paid directly to the government by the recipient of goods.

- Normally, the recipient pays their tax liabilities to their supplier, who then pays the tax to the government by filing their GSTR-1 and GSTR-3B forms.

- In some cases, such as when the supplier is a non-registered person, the Reverse Charge applies, and the recipient must pay the GST directly to the government.

Q.: What exactly is the Input Tax Credit? How Do I Get the Most Credit?

- The tax that the taxpayer paid at the time of purchase of goods or services for creating goods in a given tax period is known as the Input Tax Credit, or ITC.

- For example, suppose Mr. Kabir pays Rs. 50,000 in tax on the purchase of leather for his Shoe Business.

- Kabir has a tax liability of Rs. 1 lakh when he sells the finished product, the Shoe, during the same tax period. Then he can claim the Rs. 50,000 in ITC that he paid earlier and adjust it with their tax liability.

- Kabir will then only have to pay Rs. 50,000. A taxpayer can claim the most ITC by ensuring that their reconciliation is error-free, clean, and thorough. Using IFCCL’s Auto-reconciliation feature is a no-brainer for the taxpayer. Click here (demo link) to learn how to claim 100% ITC with IFCCL.

Q.: What are the GST Tax Rates? How many tax rates are there now?

- Under the GST System, goods are divided and classified into categories, based on which taxes are levied. These categories determine the tax rates for the goods.

- Different types of goods are taxed at different rates. For example, luxury goods are taxed at a higher rate (28%) than essential goods, which are taxed at a lower rate (as low as 5 percent).

- Typical percentages are 0%, 5%, 12%, 18%, and 28%. There are additional tax rates for fuel, alcohol, gems and precious stones, and so on.

Q.: What is the GST Composition Scheme?

- It is a government-sponsored scheme that relieves small taxpayers of the burden of filing GST on a regular basis and collects GST from small businesses without actually bothering them.

- The Composition Scheme simplified compliance for small businesses while also assisting the government in preserving income inflow.

- This relieves small enterprises of the pressure of hefty tax payments.

- GSTR-1, GSTR-3B, and GSTR-9 forms are not required to be filed by taxpayers who are part of the Composition Scheme.

- Instead, they must file GSTR-4, a quarterly tax return, and GSTR-9A, an annual tax return under this scheme.

- It contains all of the information on the quarterly filings.

Popular Articles:

- SOP for verification of Taxpayer who granted deemed registration

- GST Registration facility available for IRPs: GSTN Guidance

- Complete knowledge about GST Registration

- Input tax credit includes block credit Under GST

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.