Filing Missed ITR Returns Beyond Belated Deadline

Table of Contents

Filing a Belated Income Tax Return: Key Details

If you’ve missed the deadline to file your Income Tax Return (ITR), you can still file it as a belated return under Section 139(4). While filing the belated return, you must select Section 139(4) of the Income Tax Act.

What is a Belated Return?

A belated return is filed after the original due date (e.g., 31st July for individuals) but before 31st December of the relevant assessment year. While there are penalties, filing a belated return is better than non-compliance.

Penalties under Section 234F and interest u/s 234A may apply, depending on your tax liability and the delay in filing. Taxpayers must ensure the return is filed before 31st December of the relevant assessment year. Belated returns provide a second chance for taxpayers to comply with their obligations and avoid legal consequences for failing to file on time.

Eligibility Criteria for Filing a Belated Return

There are no specific eligibility restrictions for filing a belated return; it applies to anyone who was required to file an Income Tax Return (ITR) but failed to meet the original deadline.

Who Must File an ITR?: Filing an ITR is mandatory in the following scenarios:

- Income Threshold

- Old Tax Regime: If your total income exceeds ₹2,50,000 (basic exemption limit).

- New Tax Regime: If your total income exceeds ₹3,00,000.

(Note: Higher exemption limits apply for senior citizens and super senior citizens.)

- Specified Transactions

- You deposited more than ₹1 crore in aggregate in a current account during the financial year, including accounts with banks or cooperative banks.

- You incurred foreign travel expenses exceeding ₹2 lakh in the relevant financial year.

- Your total electricity consumption bills exceeded ₹1 lakh in the financial year.

- Other Cases

- If you have capital gains or other taxable income, even below the basic exemption limit, and certain conditions apply.

- To claim a tax refund, even if your income is below the taxable threshold.

Penalties and Drawbacks of Filing a Belated Return

- Interest Under Sections 234A, 234B, 234C: Interest is charged for late payment of taxes.

- Late Fee Under Section 234F:

- Income up to ₹5 lakhs: ₹1,000.

- Income above ₹5 lakhs: ₹5,000.

- No late fee if income is below the taxable limit.

- Losses Cannot Be Carried Forward: Losses (except house property losses) cannot be carried forward for future adjustments.

- Deductions/Exemptions Disallowed: Certain deductions under Sections 10A, 10B, 80-IA, etc., are unavailable if filed after the deadline.

- Refund Delays: Filing late may delay any refunds due.

- No Revision Beyond Deadline: A belated return can be revised, but only up to 31st December of the relevant assessment year.

How to File a Belated Return?

You can file a belated return either online or offline.

Online Method:

- Login: Access your account on the Income Tax e-filing portal.

- File Return:

- Go to “e-File” > “Income Tax Returns” > “File Income Tax Return.”

- Select the appropriate Assessment Year (AY).

- Choose Section 139(4):

- In the filing section, select 139(4) (Belated Return).

- Complete Filing:

- Enter income details, claim deductions, compute tax, and submit the return.

- e-Verify:

- Ensure to e-verify your return to complete the process.

Offline Method:

- Download Utility: Use the offline ITR preparation software.

- Upload JSON: After preparing the return, upload the

jsonfile on the portal. - e-Verify: Finalize the process by e-verifying.

Missed Filing ITR for Previous FY ? Here’s What You Can Do

If you failed to file your Income Tax Return (ITR) within the due date for previous financial years, there are still ways to address the situation. Below are the options available:

Apply for Condonation under Section 119(2)(b)

Tax Dept provides relief for taxpayers who missed filing their ITR through a condonation request.

- Purpose: For late filing or verification of ITR due to genuine reasons.

- This relief is discretionary and depends on the merits of the case. Heavy penalties may still apply if the condonation is not granted.

- Process for condonation requests:

- Submit a condonation request via the Income Tax e-filing portal.

- The request must include valid reasons for the delay.

- The tax authority assesses the request and decides whether to accept it.

- Approval for condonation requests:

- If accepted, you are allowed to file or verify the return without penalties or additional interest.

File an Updated Return under Section 139(8A)

Updated Return (ITR-U) was introduced in Budget 2022 to allow taxpayers to Rectify errors in previously filed returns & File ITR for missed deadlines within a two-year window. Taxpayers can be filed up to 24 months from the end of the relevant assessment year.

Eligibility:

-

- Taxpayers who missed filing or made mistakes in earlier returns.

- Cannot be used if the return involves a claim for refund or results in reducing tax liability.

Filing Missed Returns Beyond Belated Deadline

If you miss the belated return deadline (31st December):

- File an ITR-U (Updated Return) under Section 139(8A) with an additional tax liability:

- 25% or 50% of the tax due, depending on when the ITR-U is filed.

- The due date for filing ITR-U is 24 months from the end of the relevant financial year.

Comparison: Condonation vs. ITR-U

| Aspect | Condonation (Sec 119(2)(b)) | Updated Return (Sec 139(8A)) |

|---|---|---|

| Purpose | Relief for genuine delays in filing/verification. | Allows rectification or missed filing. |

| Approval Required | Yes, discretionary approval from tax authorities. | No, taxpayer files directly via portal. |

| Deadline | No fixed deadline (subject to approval). | 24 months from the end of the AY. |

| Additional Tax | No, if condonation is approved. | Yes, 25-50% on due tax. |

| Claim Refund | Yes, if approved. | No refund claims allowed. |

Special Circumstances for Delay

You may request a Condonation of Delay from the Income Tax Commissioner in case of:

- Genuine hardship.

- Refund due from excess tax payments.

- Cases of severe circumstances where filing was impossible.

Consequences of Late Income Tax Return (ITR) Filing

- Filing your ITR after the due date can have several financial and procedural consequences, including penalties, interest, and loss of benefits. Here’s a detailed breakdown:

- Delayed Refunds; Interest Penalty (Section 234A); Late Filing Fees (Section 234F); Loss of Carry Forward Benefits; Restriction on Choosing the Old Tax Regime (For AY 2024-25)

- Timely ITR filing ensures you: Avoid penalties and interest; Retain the ability to claim refunds, deductions, and exemptions; Minimize the risk of notices and scrutiny from the tax department; Retain flexibility in choosing your preferred tax regime.

What to Do In case the Assessee Receives a Late Payment Notice from the Tax Dept.?

Receiving a late payment notice can be stressful, but handling it carefully and promptly can minimize penalties and avoid further complications. Here’s a step-by-step guide to addressing the issue:

- Review the Notice Carefully: Ensure the information in the notice, such as your name, PAN, and assessment year, is accurate. Understand the Issue: Determine whether the notice is related to unpaid taxes, penalties, or late payment of dues. Deadline: Note any response or payment deadlines mentioned.

- Verify Your Records: Cross-check the notice with your tax records, payment receipts, and filed returns. Taxpayer Ensure that the mentioned taxes or penalties are unpaid or late. In case taxpyer has already paid, locate the Challan Identification Number (CIN) or payment receipt as proof.

- Calculate Penalties and Interest Taxpayer must review the penalty and interest charges under Sections 234A, 234B, or 234C, if applicable. Use online calculators on the Income Tax Department’s portal for an accurate estimate. then you needed to Confirm that the amounts in the notice align with your calculations.

- Pay the Outstanding Amount : If the notice is accurate, pay the due amount promptly through the Income Tax e-Payment Portal to avoid further interest or penalties. Save the receipt of the payment for future reference.

- Respond to the Notice : If you find discrepancies, log in to the Income Tax e-Filing portal and respond under the ‘e-Proceedings’ or ‘e-Nivaran’ section. Attach supporting documents, such as payment proofs, to explain your case.

FAQs related to Belated Return

Q1 : Can I claim a refund with a belated return?

Ans: Yes, but ensure your bank account is pre-validated.

Q2 : What happens if I fail to file within 31st December?

Ans: File ITR-U or face penalties, notices, or prosecution in extreme cases.

Q3 : Can losses be carried forward with a belated return?

Ans: Only losses from house property can be carried forward.

Q4 : What if my income is below the taxable limit?

Ans : No late fees under Section 234F, but filing is still advised for documentation.

Q5 : Can a belated return be revised?

Ans : Yes, but only until 31st December of the assessment year.

Q6: What if a Return is Not Filed Within the Due Date?

If you miss the due date (31st July for most individual taxpayers), you can file a belated return by 31st December of the assessment year. A late fee will apply under Section 234F:

- ₹5,000 for total income exceeding ₹5 lakh.

- ₹1,000 for total income up to ₹5 lakh.

- No penalty if income is below the taxable threshold.

Q7: Is there any penalty for late filing of ITR?

Ans : Yes, filing ITR after the due date incurs a penalty under Section 234F:

-

- INR 5,000 for income above INR 5 lakh.

- INR 1,000 for income up to INR 5 lakh.

- No penalty for individuals with income below the basic exemption limit.

Q8: Can a belated return be revised?

Ans :Yes, a belated return can be revised. However, The deadline for revising or filing a belated return is 31st December of the relevant AY. Taxpayers ensure all corrections or updates are made before this date.

Q4: Can I claim a tax refund through a belated return?

Ans: Yes, you can claim a refund by filing a belated return under Section 139(4). Taxpayer snsure: bank account is pre-validated on the e-filing portal, & The belated return u/s 139(4) return is filed within the allowed timeline.

Q5: Can a belated return be filed after 31st December?

Ans: No, a belated return cannot be filed after 31st December of the assessment year. However, the taxpayer may file an updated return (ITR-U) u/s 139(8A) for specific situations. Filing an ITR-U does not allow you to claim an tax refund.

- For example, for AY 2026-27 (FY 2025-26), the deadline for a belated or revised return is 31st December 2026. Post this, you can file ITR-U by the applicable deadlines (e.g., up to 31st March 2026), but with additional tax and penalties

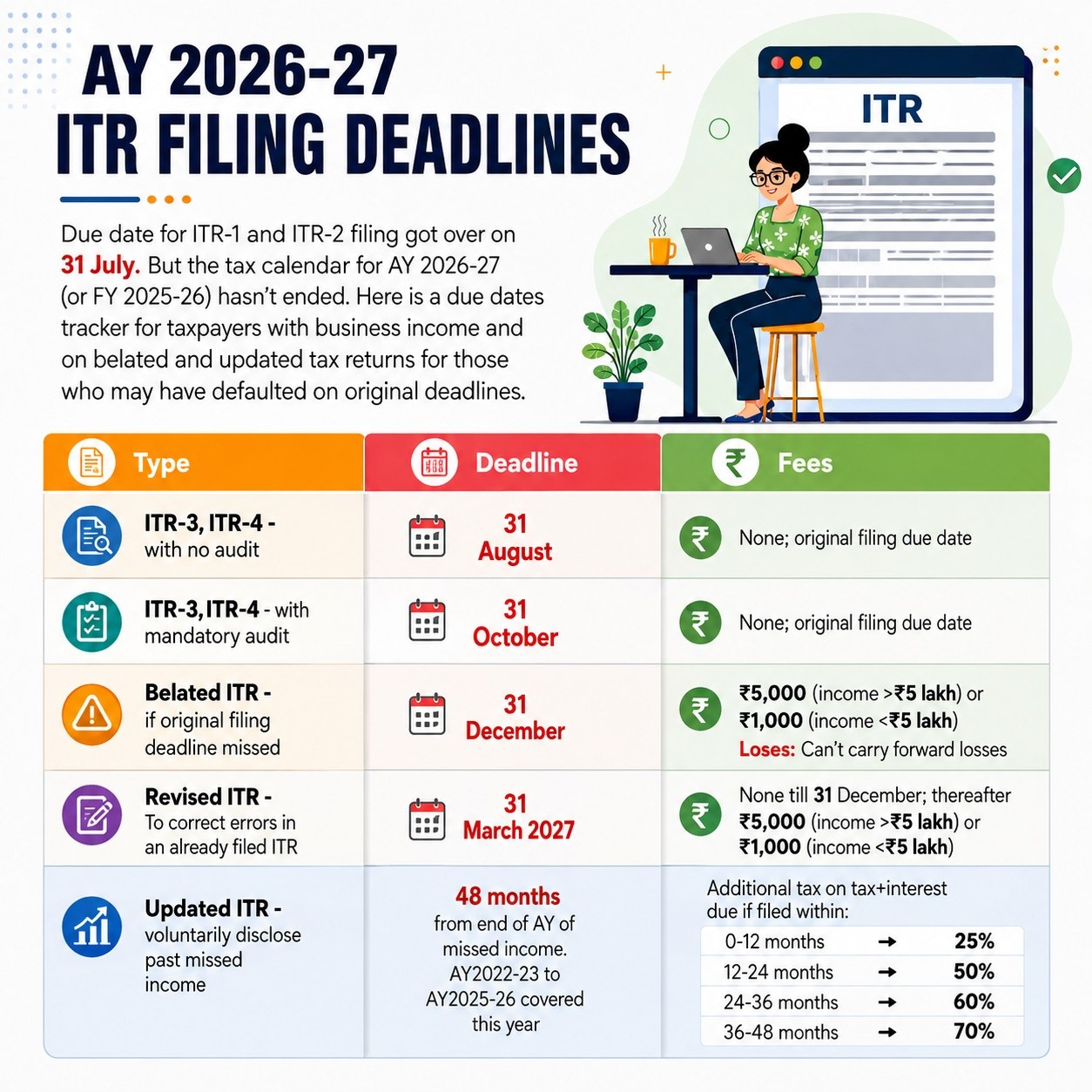

ITR filing deadlines and consequences for AY 2026-27

Key dates AY 2026-27 ITR Filing Deadlines

| Return Type | Deadline | Notes/Fee |

| ITR-3 / ITR-4 (No Audit) | 31 August | No fee; original filing due date |

| ITR-3 / | 31 October | No fee; original filing due date |

| Belated ITR | 31 December | INR 5,000 (income > INR 5 lakh) or INR 1,000 (income ≤ INR 5 lakh); loss carry-forward not allowed |

| Revised ITR (to correct errors | 31 March 2027 | No fee till 31 December; thereafter same late fee structure as above |

| Updated ITR (ITR-U) | Within 48 months from the end of the relevant AY | Additional tax payable on tax + interest |

Additional tax for Updated ITR (ITR-U)

| Time of Filing | Additional Tax |

| 0-12 months | 25% |

| 12-24 months | 50% |

| 24-36 months | 60% |

| 36-48 months | 70% |

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.