Mismatch in information of A.Y. 2021-22 between AIS & ITR

Table of Contents

Objectives of an Annual Information Statement (AIS)

Objectives of an Annual Information Statement (AIS) typically revolve around enhancing transparency, compliance, and effectiveness in tax administration. Here are some common objectives like Improving Taxpayer Compliance, Detecting Tax Evasion, Facilitating Risk Assessment, Promoting Transparency, Enhancing Data Analytics, Supporting Policy Formulation,

The objectives of AIS are aligned with the broader goals of promoting tax compliance, reducing tax evasion, and enhancing the efficiency and fairness of tax administration.

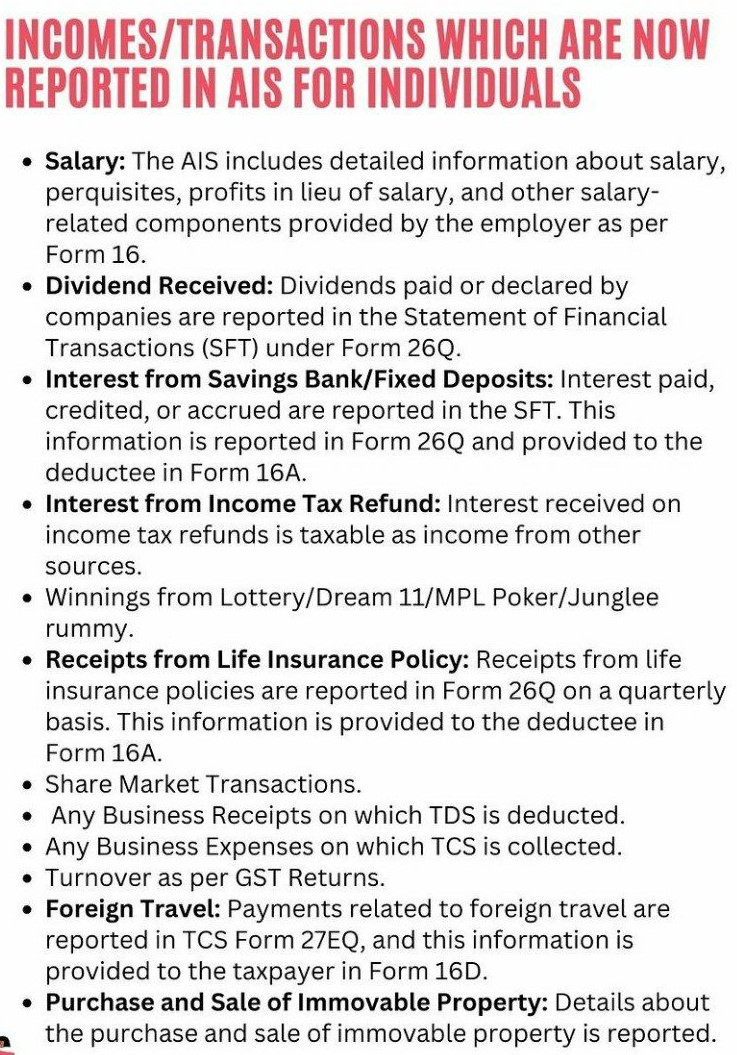

Annual Information Statement (AIS) reportable Transaction

Annual Information Statement (AIS) typically includes a wide range of financial transactions that are reported to tax authorities by various third-party entities. The transactions reported in AIS may vary depending on the jurisdiction and specific regulations, but generally, they cover significant financial activities that can help tax authorities assess taxpayers’ income and tax liabilities accurately. Here are some common types of transactions that may be reported in AIS like Investment Transactions; Bank Transactions; Credit Card Transactions; Loan Transactions: Property Transactions; Insurance Transactions; Salary and Income Details; Foreign Exchange Transactions,

Specific types of transactions reported in AIS and the threshold for reporting may vary depending on the jurisdiction’s tax laws and regulations. Additionally, not all transactions reported in AIS may be taxable, but they serve as valuable information for tax authorities to assess taxpayers’ overall financial activities and ensure compliance with Income tax Act.

Mismatch in information pertaining to A.Y. 2021-22 between AIS & ITR or Non filing ITR

- Tax Dept is in the process of sending communication(s) to the taxpayers for income and Transaction mismatch in information pertaining to A.Y. 2021-22 (F.Y. 2020-21) between AIS and ITR or Non filing ITR . Income Tax Department is urging taxpayers to view their AIS through the e-filing portal and file updated ITRs (ITR-U).

- It’s important for taxpayers to promptly address any discrepancies and file their updated ITRs to avoid potential consequences. Tax Dept is encouraging taxpayers to access their AIS via the e-filing portal and subsequently file updated Income Tax Returns (ITR-U) if necessary.

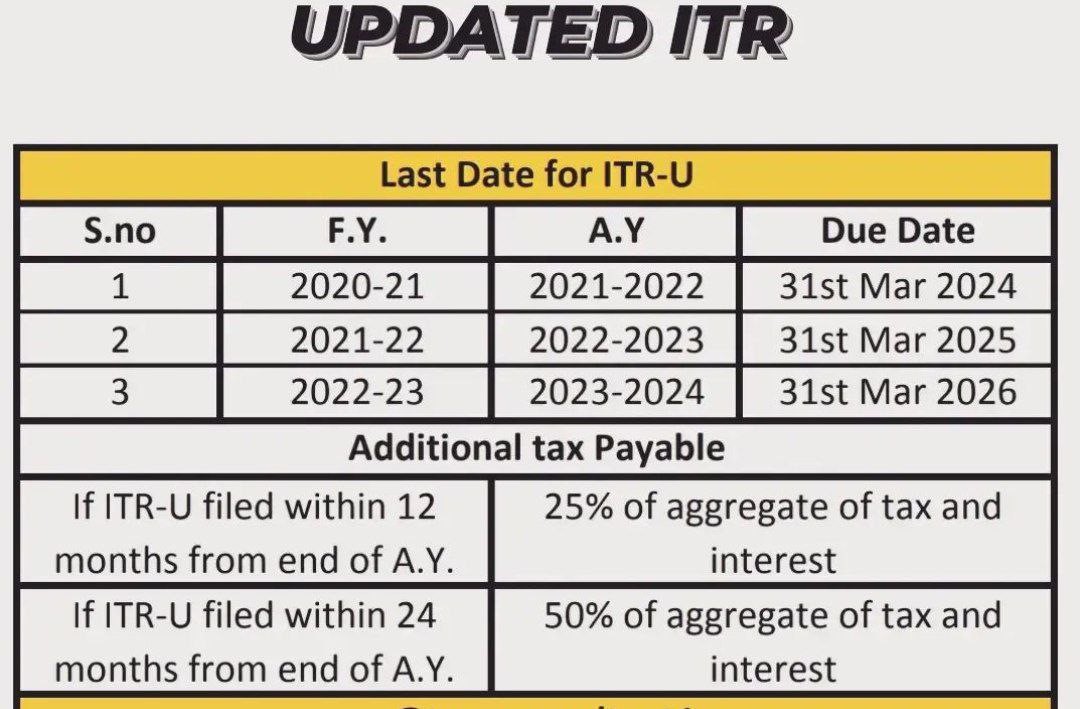

Last Date if ITR

Mismatch in information between AIS & ITR

- It appears that the Tax Dept is in the process of identifying discrepancies between the information available in the Annual Information Statement & Income tax return filings for AY 2021-22 (FY 2020-21). Taxpayers who have mismatches or have not filed their Income tax return are being urged to take action. This process is essential for ensuring the accuracy and completeness of taxpayers’ financial information as reported to the tax authorities.

- Taxpayers need to log in to the e-filing portal provided by the Income Tax Department. Once logged in, they can navigate to the section where they can view their Annual Information Statement (AIS). The Annual Information Statement contains details of various financial transactions reported to the Income Tax Department by third parties, such as banks, financial institutions, employers, etc

- Taxpayers should carefully review the information presented in their AIS. They need to ensure that all the reported financial transactions are accurate and consistent with their own records.

- If any discrepancies or missing information are identified between the Annual Information Statement and the taxpayer’s own records or previously filed Income tax returns, Income tax taxpayers should file updated Income Tax Returns using the ITR-U form. The ITR-U form is specifically designed for filing revised returns.

- After updating the Income tax return with the correct information, taxpayers need to submit it through the e-filing portal. It’s crucial to comply with the deadlines set by the Income Tax Dept for filing revised returns.

- Income tax taxpayers can ensure that their tax filings accurately reflect their financial transactions and comply with the requirements of the Income Tax Department. This helps to avoid potential penalties or further scrutiny from tax authorities due to discrepancies in the information provided.

Income Tax Returns (ITRs) have not been filed

- In cases where Income Tax Returns (ITRs) have not been filed, the Income Tax Department may still possess information regarding specified high-value financial transactions. These transactions are typically reported to the department by various third-party entities such as banks, financial institutions, registrar of properties, etc., under the Annual Information Statement (AIS) framework.

Specified high-value financial transactions could include activities such as:

- Large deposits or withdrawals in bank accounts.

- Purchase or sale of immovable property above a certain threshold.

- Investment in financial instruments like stocks, mutual funds, bonds, etc., above specified limits.

- High-value transactions in credit cards.

- Any other financial transactions as specified by the Income Tax Department.

The department uses this information to cross-verify with the taxpayer’s declared income and financial activities. If discrepancies are found or if the taxpayer has failed to file their ITRs, the department may initiate further inquiries or audits to ensure compliance with income tax Act 1961.

Tax dept has been focusing on high-value transactions for several years & sending out notices to those whose annual returns do not tally with their spending. However, the Income tax Dept has refused to provide any data on the success that it has achieved in obtaining additional revenue. In the FY 2022-23 (FY23), some 780 million ITR returns were filed, an increase of 6.8 per cent over the 730 million returns filed in FY22

This communication from the Income Tax Department serves as a reminder for taxpayers to fulfill their obligations and ensure accuracy in their tax filings. Failure to address discrepancies or non-filing of Income tax return may lead to further inquiries or penalties from the tax authorities. Therefore, it’s crucial for taxpayers to ensure that their financial transactions are accurately reported in their ITRs and that they file their returns in a timely manner to avoid any potential scrutiny or penalties from the Income Tax Department.

Responding to notices for Annual Information Statement mismatch

We can respond to the message in the following manner:

1. Provide Feedback in Annual Information Statement Provide Explanation

2.file Updated Income Tax Return u/s 139(8A) of the Income Tax Act, 1961, if eligible Feedback in Annual Information Statement can be provided by clicking on the “Provide feedback, if required” hyperlink provided against the “(B) Accepted by Taxpayer”.

3. Once the feedback is provided in Annual Information Statement Value Accepted by Taxpayer & difference value will get updated automatically.

4. Explanation can be provided by clicking on the “Provide Explanation, if required” hyperlink provided against the “(E) Explanation for difference”. Upon providing the explanation the difference value will get updated automatically.

5. In case the response is submitted with some values against “(F) Difference value for which updated Income Tax Return u/s 139(8A) need to be submit to avoid multiple compliances, if eligible”, then you are expected to furnish an updated return of income u/s 139(8A) for the difference value.

The Central Board of Direct Taxes releases new functionality in Annual Information Statement to display the status of feedback given by Taxpayer

List of Information covered under Annual Information Statement

Taxpayer Can submit transactions feedback in the AIS- Attention Taxpayers

You now have the ability to review your transactions and submit feedback in the Annual Information Statement (AIS). Here’s how the feedback process works:

- Provide feedback on the transactions listed in your AIS.

- Your feedback is sent to the source of the information for verification.

- The source reviews the feedback and provides details.

- If the source confirms that there was an error in the AIS, the necessary corrections will be made.

- You can track the status of your feedback and see whether it has been partially accepted, fully accepted, or rejected.

This initiative is designed to simplify compliance and enhance services for taxpayers.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.