Provision of Sec 43B(h) for payments made to MSMEs

Table of Contents

All about deduction U/s 43B(h) for payments made to MSMEs

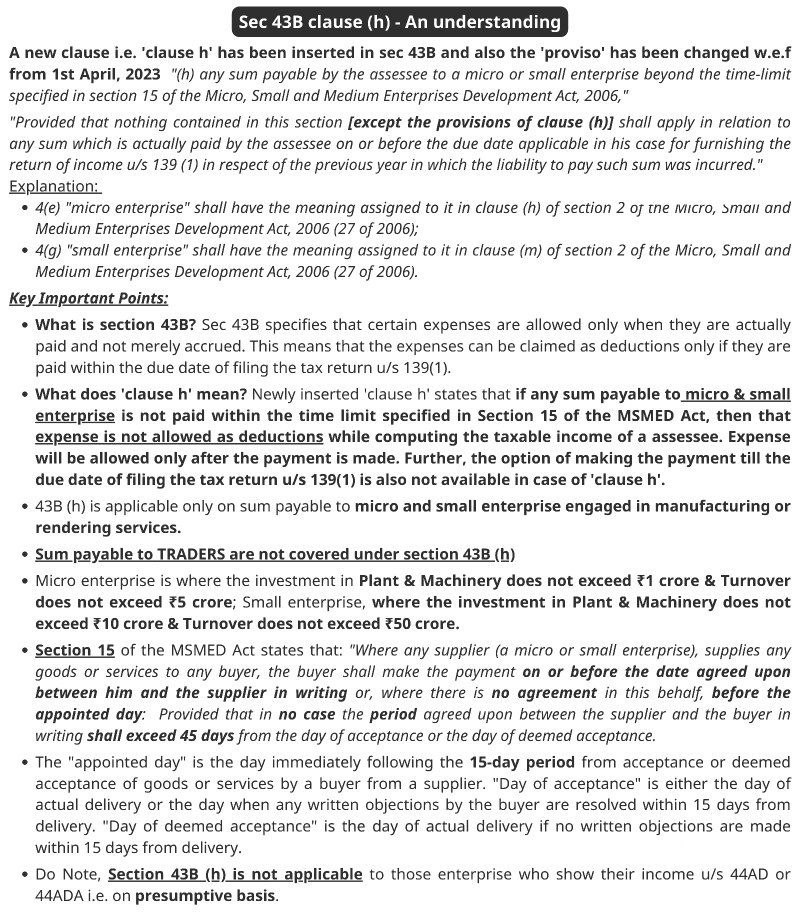

- Finance Act 2023 inserted Section 43B(h) was inserted by the Finance Act of 2023. It stipulates that any money owed to MSME Enterprises may be deducted in the same year if it is paid within the deadline stipulated by the Micro, Small and Medium Enterprises Development Act, 2006.

- This amendment aims to address the issue of working capital scarcity in this industry and promote prompt payments to micro and small businesses. The assessment year 2024–2025 and any following years will be covered by this change, which will go into effect on April 1, 2024. Govt started a Portal to launch Complaint for Delayed Payment – MSME Samadhaan launched

- In most cases, expenses are deducted under section 43B if they are paid within the deadline for filing an income return, as is set forth in section 139. Section 43B(h) disallowances, on the other hand, are exempt from this rule and are approved as expenses in the year of payment.

What is Small Enterprises?

Business Entity or Enterprise which is fulfilled all the below mentioned conditions.

(a) Sale or Turnover should not more than INR 50,00,000/-

(b) Investment is Plant & Machinery Should not more than INR 10,00,000/-

What is Micro Enterprises?

Business Entity or Enterprise which fulfilled all the following mentioned condition.

(a) Sale or Turnover should not more than INR 500,00,000/-

(b) Investment is Plant and Machinery Should not more than INR 100,00,000/-

Steps to be taken Ministry of Micro, Small & Medium Enterprises:

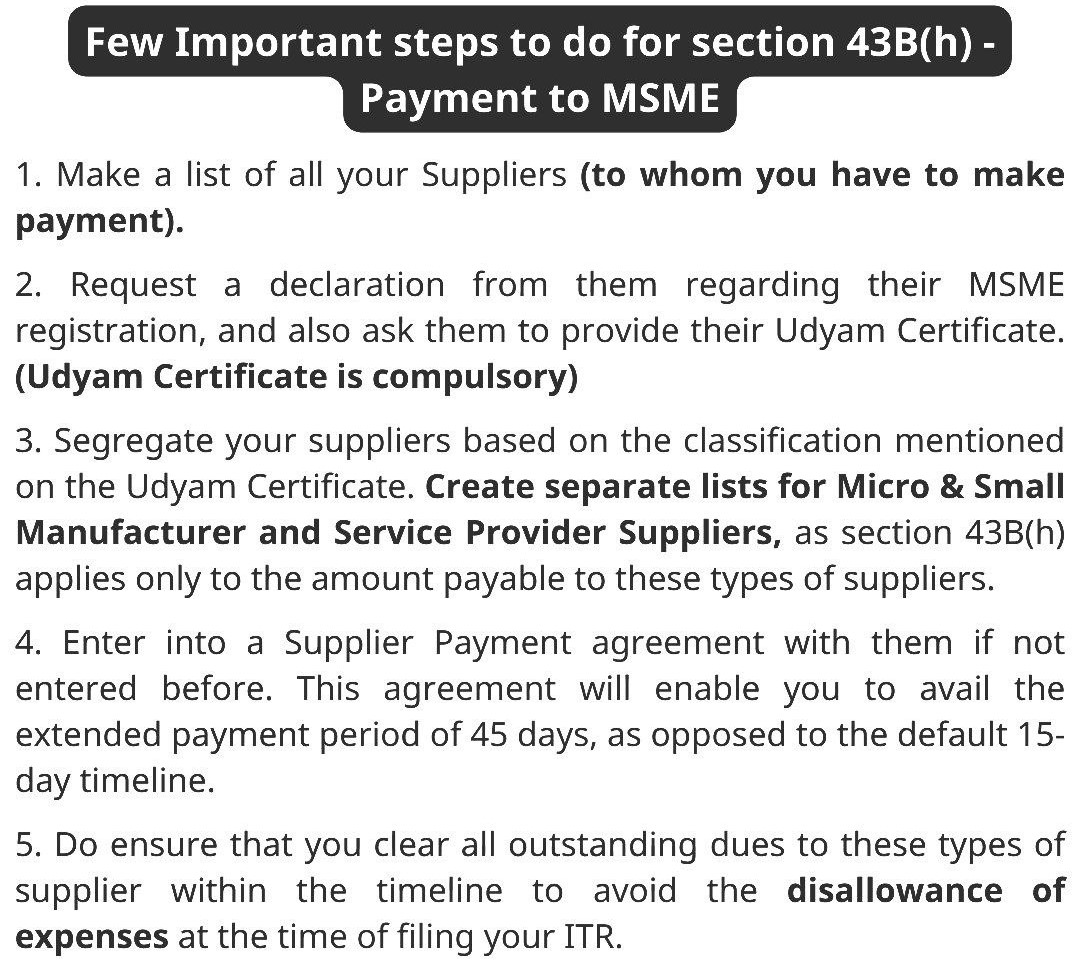

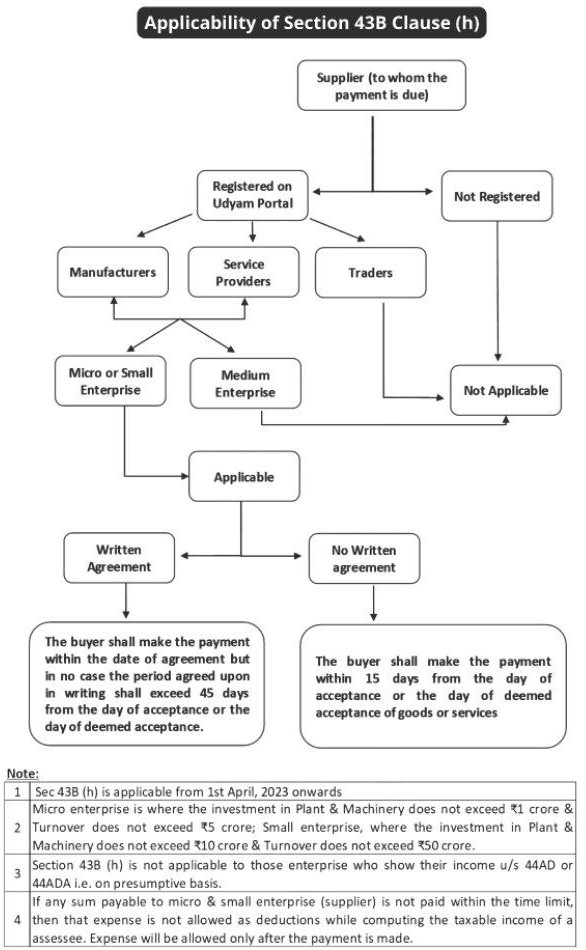

- Identify the Micro and Small vendor by obtaining Ministry of Micro, Small and Medium Enterprises certificate for classification (Micro / Small only).

- As per the provision of Micro, Small and Medium Enterprises Development Act, 2006 Section 15 is required that Compulsory payments to Ministry of Micro, Small and Medium Enterprises within the time as per specified written agreement, which cannot be more than forty Five days. In case no such written agreement is there, Micro, Small and Medium Enterprises Development Act, 2006 Section 15 make the provision that the all the MSME vendors payment shall be made within fifteen days.

- Expenses will be disallowed for the relevant year and allowed in the year in which the payment is made if creditors are still unpaid as of March 31 for a period longer than 45 days or 15 days from the date of the service invoice and the date of acceptance of goods (GRN), as applicable.

- Enter into an agreement with Ministry of Micro, Small and Medium Enterprises vendors / document the terms of payment, failing which the due will be automatically reckoned as 15 days. In case PO is raised, payment terms specified in the PO shall be considered for this purpose subject to an outer limit of 45 days.

- Explore the possibilities of bills discounting to settle Micro / Small vendor dues within the due date permitted.

The newly inserted clause in Sec 43B reads as follows:

“Sec 43B: Notwithstanding anything contained in any other provision of this Act, a deduction otherwise allowable under this Act in respect of-

(h): any sum payable by assessee to a MICRO or SMALL enterprise beyond the time limit specified in 15 of the MSME Development Act, 2006,”

The MSMED Act, 2006 (Dealing with Delayed Payment) – Related Provision

Details of Analysis of the Clause -MSME Payment U/s 43B(h) of the Income Tax Act, 1961 :

- Business Enterprise required to pay to Micro, Small and Medium Enterprises within fifteen or forty-five days as per section 15 of the Micro, Small and Medium Enterprises Development Act, 2006

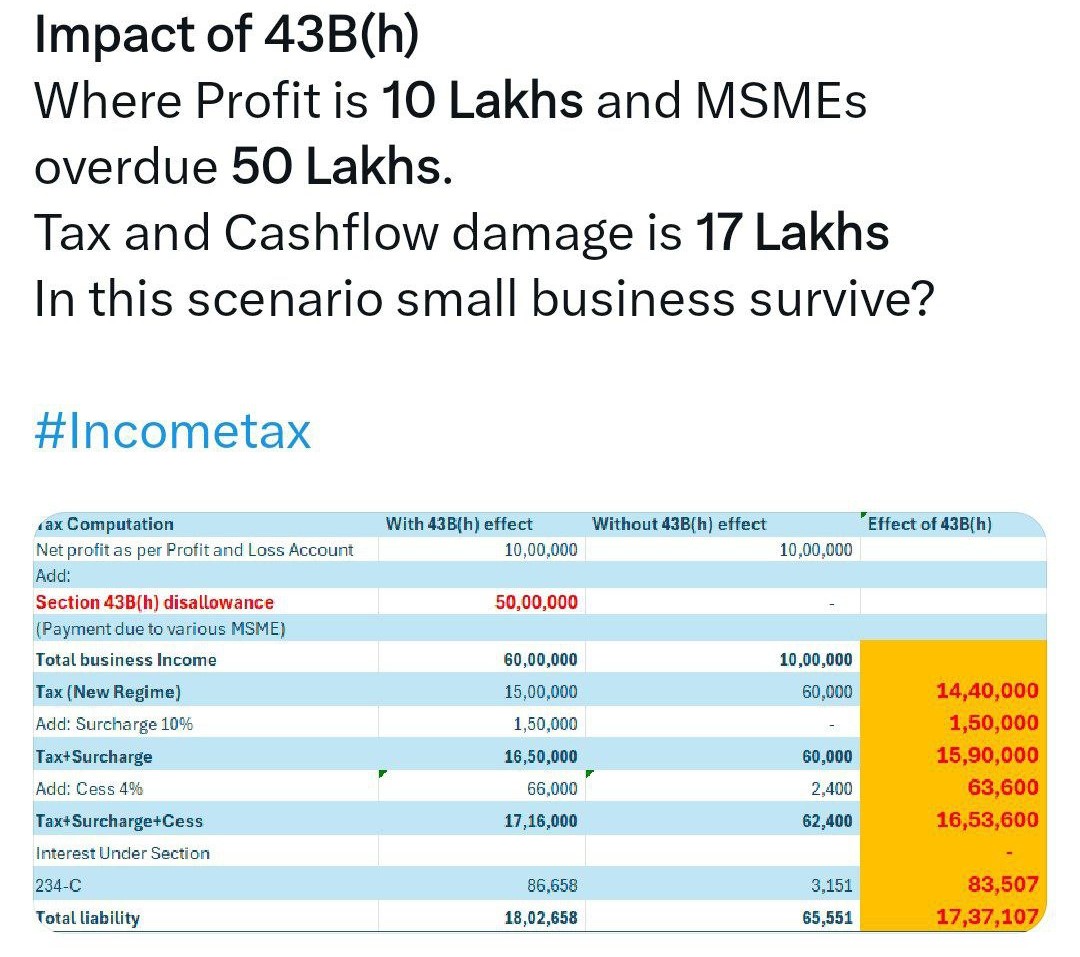

- If payment is not made within the above time period, that outstanding payable amount will be added to the taxable income of the business enterprise.

- In case there is no written proper agreements, payments shall be made within fifteen days.

- In case there is a written proper agreement, all the payment shall be made as per time period mentioned in written agreement. The above said agreements shall be Maximum forty five days.

- Section 15 of the MSMED Act specifies a 45-day term starting from the date of the customer’s acceptance or presumed acceptance of the products or services, or from the period of time agreed upon in writing between the buyer and the supplier, whichever comes first. The deadline is 15 days from the date of delivery of the products or services if there is no written agreement.

Drastic Consequences – on delayed Payments To Micro, Small and Medium Enterprises Vendors.

Interest u/s 16 of the Micro, Small and Medium Enterprises Development Act, 2006:-

- Interest allowable as deduction in computation of Income Tax : As per Micro, Small and Medium Enterprises Development Act, 2006 Section 16, above interest expenses are in nature of Penal Interest paid by business enterprise. So, interest expenses incurred for delayed payment to Micro, Small and Medium Enterprises is not allowed under Section 37 of Income Tax Act,1961.

- Note: It is to be noted that only MSME entity are covered under this clause. Therefore, this clause shall not be applicable on Medium Enterprises.

Consequences for Tax Auditors in case the Non Compliance of section 43B(h)

- With effect from Financial Year 2023-2024, In case status of the Micro and Small vendor has not been ascertained, This non compliance fact will have to be pointed out by Company or business Tax Auditor in the His income tax form 3CD which may lead to add back of expenditure or disallowance expenditure during his income tax assessments & it result exposure to penal provisions of income tax act will be attracted.

Consequences of not making the payment within prescribed time frame

- In case outstanding payments is not made within prescribed time, then that outstanding payable amount shall be added to taxable income of Taxpayer & That Taxpayer has to bear Income tax liability on respective outstanding amount. The Assessee gets deduction in previous year where payments is made.

- In case the business enterprise not make payment to Micro, Small and Medium Enterprises in above prescribed period, then it has to make payment of compound interest at monthly rests to supplier at 3 times Bank Interest as same is notified by RBI.

- To put it briefly, the adjustment to Section 43B(h) represents a major advancement in the Indian corporate ecosystem’s promotion of financial stability, compliance, and cooperation. The stage is set for a more sustainable and equitable future in the complex web of tax and company regulations as we anticipate these changes taking effect on April 1, 2024.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.