Section 16(4) eligibility & Conditions for claiming ITC.

Table of Contents

Complete Explanation of Section 16(4) of Central Goods and Services Act, 2017 :

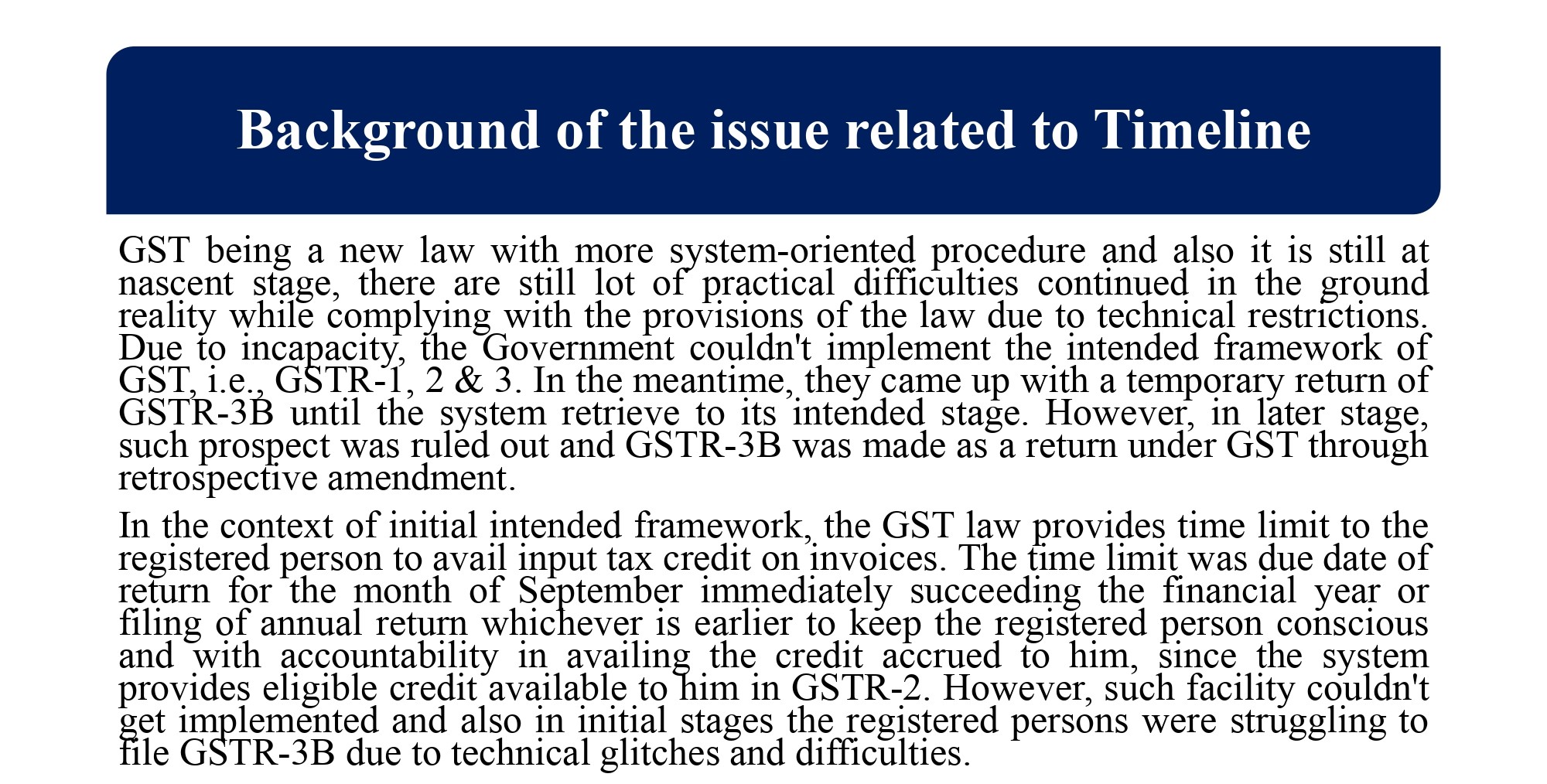

- Section 16(4) of the Central Goods and Services Act, 2017, pertains to basic conditions & eligibility of taking ITC. ITC allows businesses to claim a set-off on the goods and services taxes, which is paid on inputs used during the normal course of business’ & profession against the Goods and Services payable on their output services or goods provided to customers.

Discussion to Section 16(4) of GST Laws

Under section 16(4) of the Central Goods and Services Act, 2017 clearly says that a GST Registered person can only claim ITC only if Goods or services received are used in the course or furtherance of their business. Personal use of goods or services disqualifies them from claiming Input Tax Credit.

Means to say that Section 16(4) of Central Goods and Services Act, 2017 is only allowed for used of ITC in case Goods / Services are not used for personal use, In case it is used for personal purpose than its are not eligible to claim the Input Tax Credit.

What is deadline of Claiming / Availing Input Tax Credit (ITC)

Deadline / Time limit to claim Input Tax Credit on invoices or debit notes of a FY is Revised to earlier of below of due dates.

- 1st on is , 30th November of the Next Year or

- 2nd Year, Date of filing annual returns under the GST .

So we can say that a GST registered person cannot claim Input Tax Credit (ITC) after the below Dates.

- 30th November of the Next Year or

- Date of filing annual GST returns – Whichever is earlier.

What is Vested Right & Entitlement?

Constitution of India Article 300A, Right to Property: “No person shall be deprived of his property save by authority of law.”

- The important words used in this article are:

- Person

- Property

- Deprived

- Authority of Law

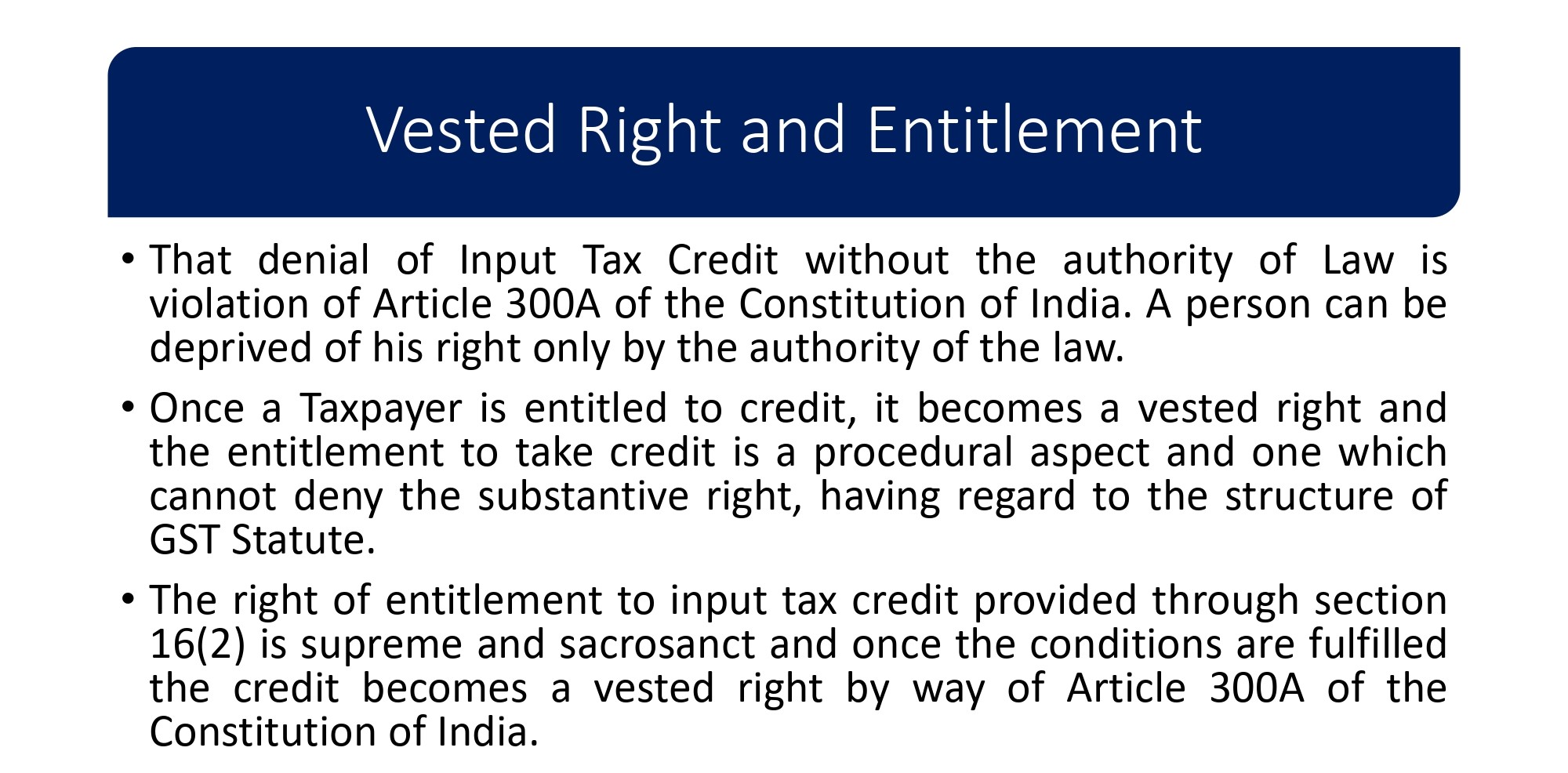

- That denial of Input Tax Credit without the authority of Law is violation of Article 300A of the Constitution of India. A person can be deprived of his right only by the authority of the law.

- Once a GST Taxpayer is entitled to credit, it becomes a vested right & entitlement to take ITC credit is a procedural aspect & one which cannot deny the substantive right, having regard to the structure of GST law.

- The right of entitlement to input tax credit provided through section 16(2) is supreme and sacrosanct and once the conditions are fulfilled the credit becomes a vested right by way of Article 300A of the Constitution of India.

Kavin HP Gas Gramin Vitrak vs The Commissioner of Commercial Tax (2023)

- If form is not notified, petitioner cannot be expected to file the same to claim ITC – Assessee should not be prejudiced from availing credit that they are otherwise legitimately entitled

- Reversal of ITC for belated claim as per Sec. 16(4) of TNGST is not applicable, since the filing of GSTR-3B is not meant for claim of Input Tax

- Also, in the absence of any enabling mechanism, the taxpayers cannot be prejudiced by not granting ITC.

Union of India vs Brand Equity Treaties Ltd. (2020)

First argued at Delhi High Court in the matter of Brand Equity Treaties Ltd. vs UOI (2020) where it was held that the rules prescribe the period as merely directory and due to non- filing/delay in filing of Form GST TRAN-1 cannot be the ground for denial of transitional credit. Then GST Dept went to Supreme Court and SC in the Landmark Judgement allowed credit to everyone & GST Portal was Reopened.

Main Provisions of Section 16 (4) must be taken care whiles claiming ITC :

- Registered Person Eligibility can claim the input tax credit, ensuring that unregistered entities do not take advantage of the ITC system and cause revenue loss for the government.

- Proper Documentation related accounting and record keeping,

- Business Use must be utilized solely for business purposes,

- Enhanced Business Accountability for claim ITC for legitimate business purposes, promoting transparency and accountability in the taxation system.

- Importance of Documentation necessitating record-keeping of all purchases and expenses & Compliance Requirements must be taken care,

- Understanding and complying with Section 16 (4) is vital for businesses to avoid penalties and legal implications.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.